Carrying credit card debt while interest keeps compounding is genuinely exhausting. You pay every month, you do everything right, and somehow the balance barely moves. That’s not a personal failure — that’s how high-APR debt works. The numbers are stacked against you.

Balance transfer cards exist for exactly this situation. Move your debt to a card offering 0% intro APR, and suddenly every payment you make is actually reducing what you owe — not just covering the bank’s monthly cut.

But these cards come with real tradeoffs, fine print that trips people up, and approval requirements that not everyone meets. This guide covers what’s worth knowing in 2026, without the fluff.

Table of Contents

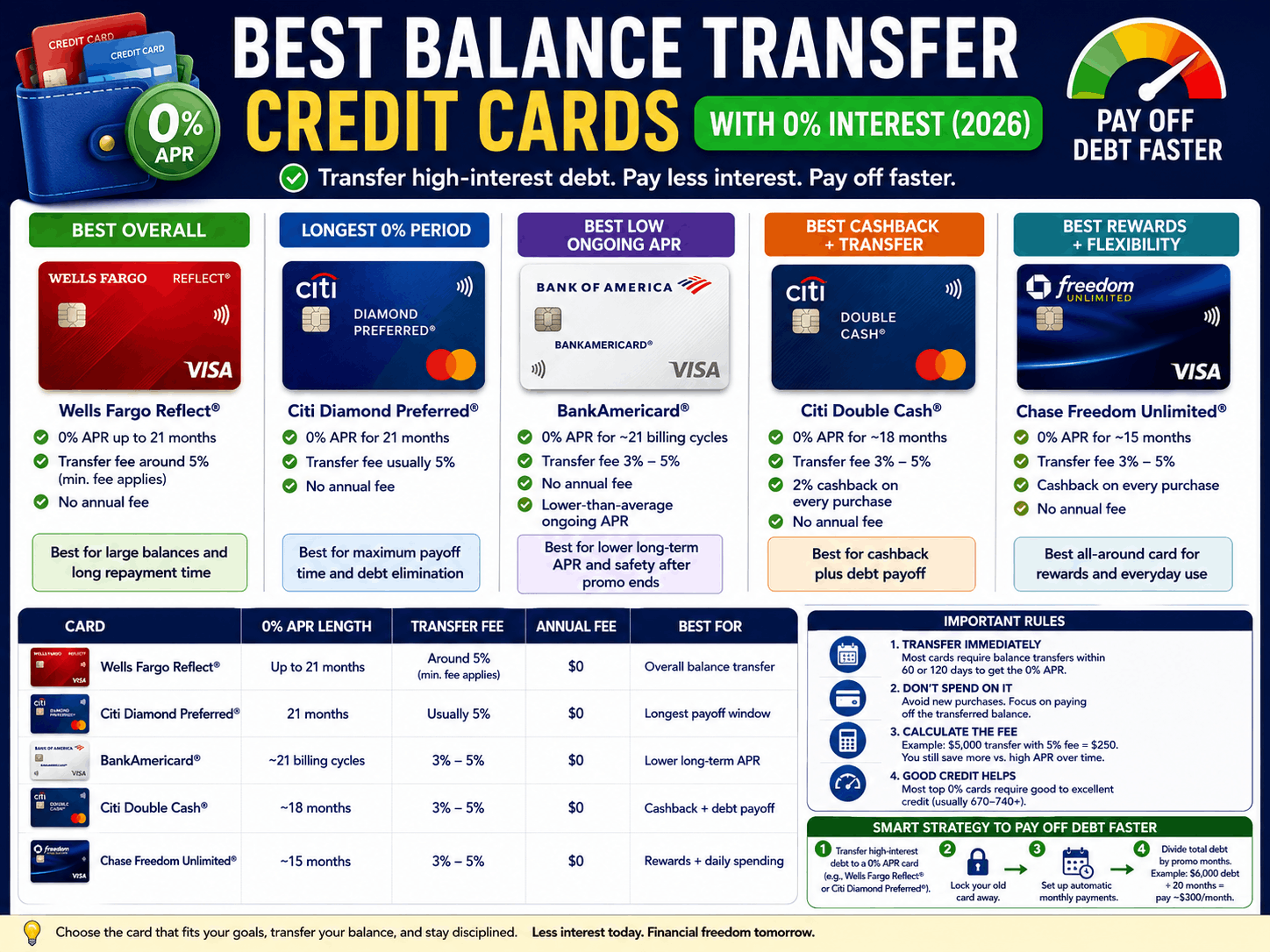

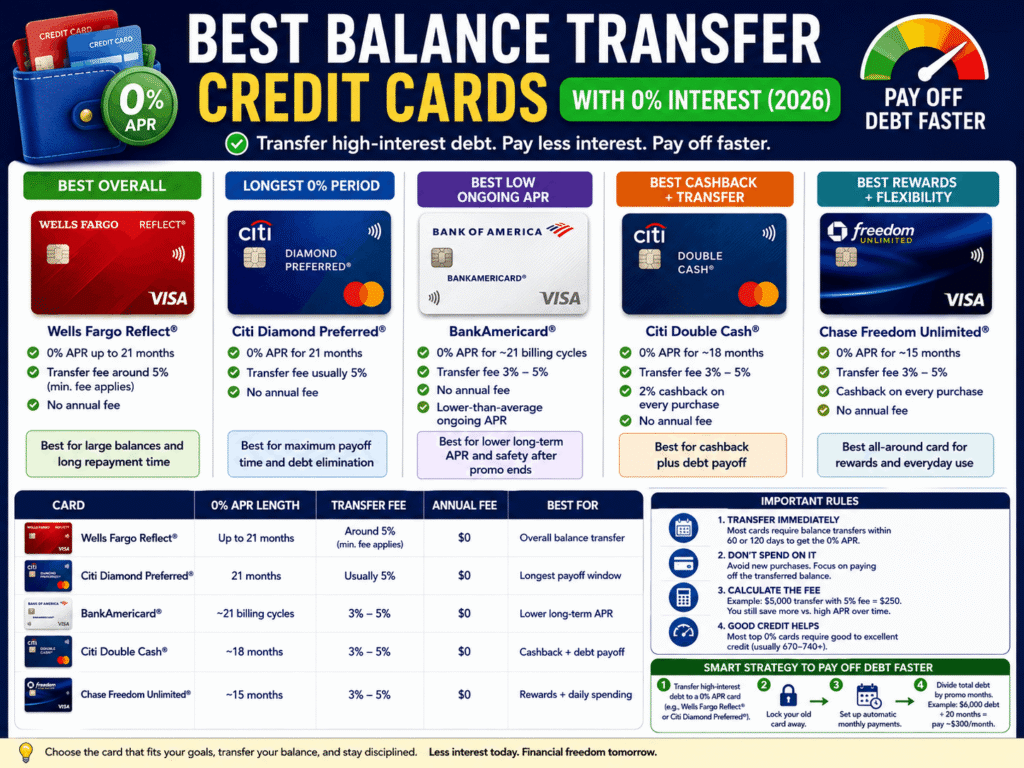

Quick Summary: Best 0% Balance Transfer Cards in 2026

Before getting into the details, here’s an at-a-glance comparison of the top options based on intro period length, transfer fee, and credit requirements. <div style=”overflow-x:auto;”>

| Card | 0% Intro Period | Balance Transfer Fee | Regular APR After | Credit Needed |

|---|---|---|---|---|

| Citi Simplicity® Card | Up to 21 months | 3% (min $5) | Variable | Good–Excellent |

| Wells Fargo Reflect® Card | Up to 21 months | 5% (min $5) | Variable | Good–Excellent |

| BankAmericard® Credit Card | 18 billing cycles | 3% intro, then 4% | Variable | Good–Excellent |

| Discover it® Balance Transfer | 18 months | 3% intro, then 5% | Variable | Good–Excellent |

| Chase Slate Edge℠ | 18 months | 3% intro | Variable | Good |

| Citi® Double Cash Card | 18 months | 3% (min $5) | Variable | Good–Excellent |

</div>

Note: APR rates and terms change. Always verify current offers directly with the card issuer before applying.

What Is a Balance Transfer, Exactly?

A balance transfer means moving debt from one credit card (or sometimes a loan) to a different credit card — usually one offering a promotional 0% APR period.

Here’s a simple example: Say you have $4,000 on a card charging 24% APR. At that rate, minimum payments keep you in debt for years, with hundreds of dollars going purely to interest. You apply for a balance transfer card with a 0% intro period of 18 months, move that $4,000 over, and now you have a fixed window to pay it down without any interest piling on top.

The key word is promotional. That 0% rate expires. When it does, whatever balance remains gets hit with the card’s regular APR — which is often high. That’s the part people don’t fully internalize until it’s too late.

The Best Balance Transfer Cards in 2026 — Reviewed

Citi Simplicity® Card

Best for: People who want the longest possible 0% window with no penalty APR

The Citi Simplicity consistently offers one of the longest intro periods available — up to 21 months on balance transfers made within the first four months of opening the account. There’s no annual fee, no late fee, and no penalty APR if you miss a payment (though you should still avoid missing payments for credit score reasons).

Advantages:

- Up to 21-month 0% intro APR on balance transfers

- No annual fee

- No penalty rate for late payments

Downsides:

- No rewards program whatsoever

- 3% transfer fee applies (some cards have eliminated this)

- The 0% only applies to transfers, not new purchases initially

Who should avoid it: If you want a card you’ll actually use for everyday spending and rewards after the promo period, this isn’t the best fit.

Wells Fargo Reflect® Card

Best for: People who want a long intro period on both purchases and balance transfers

The Reflect card offers up to 21 months of 0% APR on both balance transfers and new purchases when you meet certain conditions. That flexibility makes it useful if you also need to make a large purchase during the payoff period without paying interest.

Advantages:

- Extended intro period for purchases, not just transfers

- No annual fee

- Cell phone protection as a benefit

Downsides:

- 5% transfer fee is higher than competitors

- No rewards program

- Requires good to excellent credit for approval

Hidden risk: The 5% transfer fee can add up fast. On a $5,000 balance, that’s $250 upfront — not nothing. Run the math against what you’d pay in interest on your current card to confirm it still makes sense.

BankAmericard® Credit Card

Best for: People who want a straightforward card with a long intro period and lower fee upfront

The BankAmericard offers 18 billing cycles at 0% on balance transfers, with a 3% intro transfer fee for the first 60 days (it goes to 4% after that). This makes timing your application and transfer important.

Advantages:

- 18 billing cycles of 0% on transfers

- 3% transfer fee window for early transfers

- No annual fee

Downsides:

- Not as long as Citi Simplicity or Wells Fargo Reflect

- No cash back or rewards

- Need to act quickly to lock in the lower transfer fee

Discover it® Balance Transfer

Best for: People who want 0% on transfers and cash back rewards after the intro period

Discover is one of the few issuers where you get meaningful rewards even on a balance transfer card. The 18-month 0% period applies to transfers, plus you earn 5% cash back on rotating categories and 1% on everything else after that.

Advantages:

- 18 months 0% on transfers

- Cash back rewards program — rare for this card type

- Discover matches all cash back earned in year one

- No annual fee

Downsides:

- Transfer fee goes from 3% to 5% after the intro period — watch the timing

- Discover is accepted nearly everywhere in the US but has less international coverage

Who should consider it: If you’re going to keep using the card after paying off the debt, Discover’s rewards structure gives it long-term value most balance transfer cards don’t offer.

Citi® Double Cash Card

Best for: People who want a balance transfer card that stays useful long-term

The Double Cash earns 2% back on everything — 1% when you buy, 1% when you pay. The 18-month 0% intro on transfers makes it a decent debt payoff tool and a solid everyday card after the promo ends.

Advantages:

- Flat 2% cash back with no rotating categories

- 18-month 0% intro on balance transfers

- No annual fee

Downsides:

- 3% transfer fee applies

- 0% doesn’t apply to purchases — only transfers

- Some people find the dual-rate earning structure slightly confusing at first

Real-World Cost Example: Does a Balance Transfer Actually Save Money?

Let’s run a realistic scenario.

Situation: $6,000 in credit card debt at 22% APR. You’re making $200/month minimum payments. <div style=”overflow-x:auto;”>

| Scenario | Time to Pay Off | Total Interest Paid | Transfer Fee |

|---|---|---|---|

| Stay on current card (22% APR) | ~4+ years | ~$2,800+ | $0 |

| Transfer to 0% / 18-month card | 18 months (if paying ~$333/month) | $0 | ~$180 (3%) |

| Transfer to 0% / 21-month card | 21 months (if paying ~$285/month) | $0 | ~$180–$300 |

</div>

Even with the transfer fee, you’re saving significantly — but only if you commit to paying the balance down before the intro period ends. If you transfer and keep making minimum payments, you’ll likely still have a balance remaining when the 0% expires, and the regular APR kicks in immediately.

Hidden Fees and Traps to Watch For

This is where a lot of people get caught off guard. The 0% offer sounds clean, but there’s always fine print worth reading.

Balance transfer fee Almost every card charges 3% to 5% of the transferred amount. On $8,000, a 5% fee is $400 added to your balance immediately. Factor this into your math before applying.

The introductory APR expiration When the promo ends, any remaining balance gets the card’s standard APR — often 20% to 29% depending on your creditworthiness and current rates. This isn’t disclosed in a tricky way; it’s in the terms. But people underestimate how often they’ll have a remaining balance.

New purchase APR is different Most balance transfer cards don’t apply the 0% promo to new purchases. If you use the card for everyday spending while also trying to pay down a transferred balance, payments typically go to whichever portion has the lower APR first — meaning new purchases could quietly accrue interest in the background.

Late payments Missing a payment on some cards immediately cancels the promotional rate and triggers the penalty APR, which can exceed 29%. Always set up autopay for at least the minimum.

Transfer deadlines Most issuers require you to complete the transfer within 45 to 60 days of opening the account to qualify for the promotional rate. Missing this window means paying the regular APR from day one.

Common Mistakes People Make With Balance Transfers

Applying with too-low credit scores. These cards generally require good to excellent credit (roughly 670+ on the FICO scale). Applying with a score in the 580–640 range often results in denial — and the hard inquiry still hits your credit report. Check your score before applying.

Closing the old card immediately. Once the balance is transferred, the temptation is to close the old card and be done with it. This can actually lower your credit score by reducing available credit and shortening average account age. Leave it open if there’s no annual fee.

Using the old card again. After transferring the balance, some people start charging the old card back up — effectively creating two debt problems instead of one. If this is a pattern for you, consider addressing the spending habits alongside the debt transfer.

Not doing the math on the fee. A 3% fee on a small balance might not be worth it. If you’re transferring $800 at a 24% APR card and can realistically pay it off in four months anyway, the $24 fee and a new credit inquiry may not be worth the hassle.

Forgetting about the 0% end date. Set a calendar reminder. Seriously. Banks don’t send you an enthusiastic notice when your promo period is about to end.

Who Should Probably Skip Balance Transfer Cards

Not everyone benefits from this approach.

- People with fair or poor credit — Approval odds are low, and applying can ding your score without any benefit.

- Anyone who can’t commit to paying down the balance — If the math shows you won’t eliminate most of the balance within the promo period, you’re mostly paying a transfer fee to delay the same problem.

- People with very small balances — If you owe $300 or $400, the transfer fee and credit inquiry don’t make much sense. Focus on paying it off directly.

- Anyone already near their credit limit — Adding a new card while carrying high utilization on existing accounts can compound score damage short-term.

How to Choose the Right Card for Your Situation

Step 1: Know your balance amount and current APR. If you’re paying 15% on $1,500, the urgency is lower than someone paying 27% on $7,000. Higher balance + higher APR = greater case for a transfer.

Step 2: Calculate how long you realistically need. Divide your balance by the number of months in the promo period. That’s the minimum monthly payment required to clear the debt before the rate changes. If that number is unrealistic for your budget, you need a longer promo period — or a different strategy.

Step 3: Compare the transfer fee vs. interest savings. Even a 3% fee is usually worth it if you’re paying 20%+ APR. But run the numbers for your specific situation.

Step 4: Check your credit score first. Use a free tool like Experian or Credit Karma to estimate your score before applying. This helps you target cards you’re actually likely to be approved for.

Step 5: Read the actual terms. The promo period, transfer deadline, what triggers the penalty APR, and how payments are allocated to different balances — all of this is in the card’s terms. It takes ten minutes to read and can save you real money.

Frequently Asked Questions

Does a balance transfer hurt my credit score? Applying for a new card creates a hard inquiry, which may temporarily lower your score by a few points. However, if the transfer reduces your utilization rate on your existing card, that benefit often outweighs the inquiry within a few months.

Can I transfer balances from multiple cards? Yes, most cards allow transfers from multiple accounts — as long as the total doesn’t exceed your approved credit limit on the new card.

What happens if I don’t pay off the balance before the 0% period ends? The remaining balance starts accruing interest at the card’s regular variable APR, which is disclosed in the terms when you apply. It’s typically in the 19%–29% range depending on your credit profile.

Can I transfer a balance to a card from the same bank? Generally no. Most issuers don’t allow transfers between their own cards. For example, you can’t transfer a Chase balance to another Chase card.

Is there a limit on how much I can transfer? The maximum is usually equal to your approved credit limit on the new card, minus any applicable transfer fee. So if you’re approved for a $5,000 limit and the fee is 3%, your effective transfer ceiling is around $4,850.

Will I get approved if I have a 670 credit score? It depends on the card and the issuer’s full picture of your credit profile. A 670 is at the low end of “good” credit territory. You may be approved but with a lower credit limit, or you may be declined. It varies.

Final Thoughts

A 0% balance transfer card is one of the more practical tools available for managing credit card debt — if you use it with a clear plan. The mechanics are simple: move the debt, pay it down aggressively during the promo window, and stop adding to it.

Where people go wrong is treating the transfer as the solution rather than the starting point. The card buys you time. What you do with that time determines whether you come out ahead.

If your debt is high, your current APR is painful, and you have the credit score to qualify, it’s worth comparing offers. If the math works out and you can commit to the payments, a balance transfer can meaningfully reduce what you pay overall.

Just make sure you understand the fee, the expiration date, and what happens if there’s a remaining balance when the promo ends. Those three things cover most of the common problems people run into.

Always review current terms directly with card issuers, as rates and promotional offers change regularly.