If you’ve been carrying credit card debt for a while, you’ve probably seen those offers — “0% APR for 15, 18, or even 21 months on balance transfers.” They sound almost too good. And if you’ve ever wondered whether they’re legitimate, how they actually work under the hood, or what the catch is, you’re not alone.

This guide breaks it all down honestly. No sales pitch, no oversimplification. Just a clear explanation of how 0% APR balance transfers work, what they cost, and whether they make sense for your situation.

Table of Contents

Quick Answer: How a 0% Balance Transfer Works

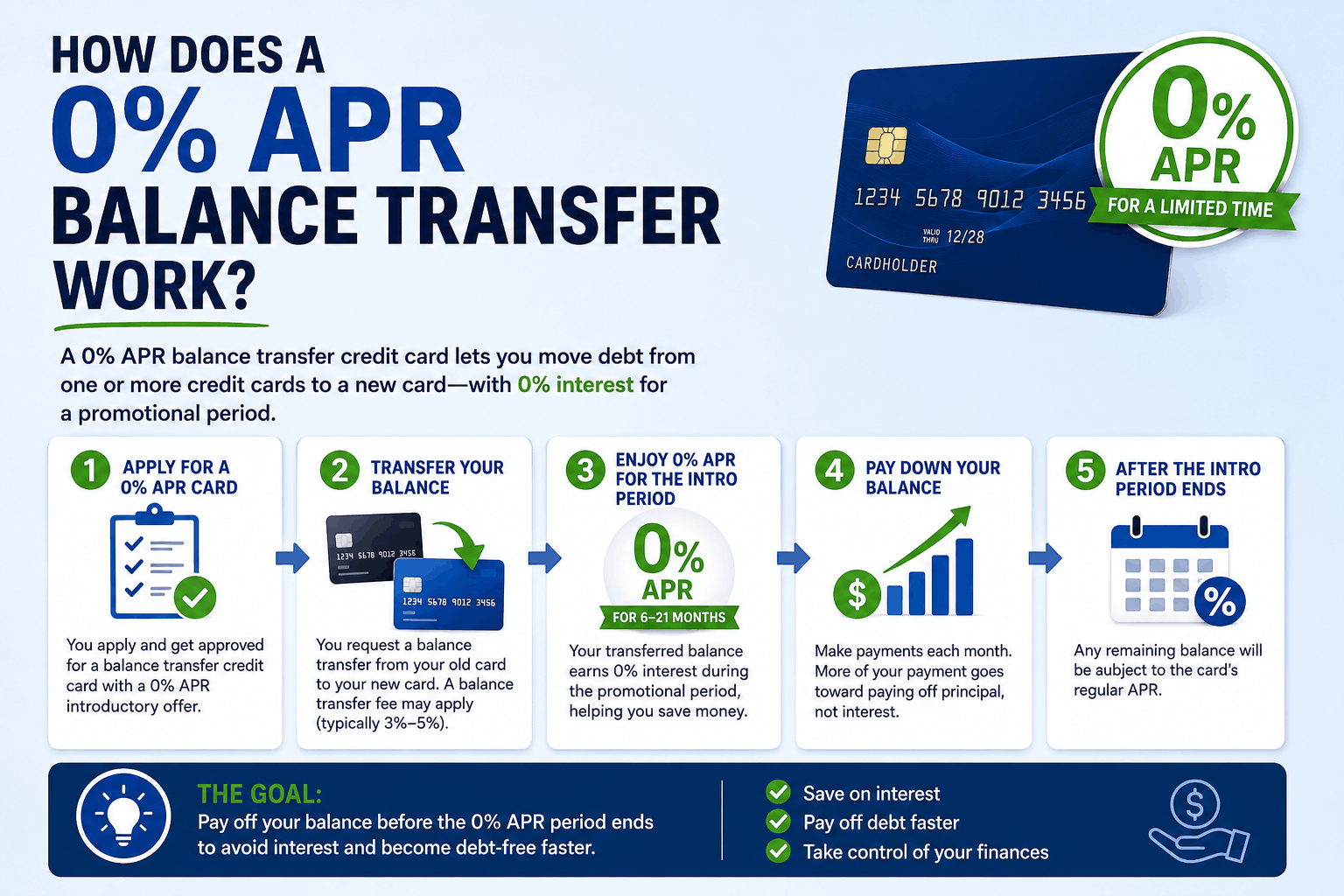

You move existing credit card debt onto a new card that charges 0% interest for a limited promotional period — usually 12 to 21 months. During that window, every payment you make goes entirely toward reducing your balance instead of feeding interest charges.

You still owe the debt. You still have to make monthly payments. But none of your money is lost to interest while the promotion is active.

Key Terms at a Glance

| Term | What It Means |

|---|---|

| Promotional APR | 0% interest for a set period (e.g., 18 months) |

| Balance Transfer Fee | One-time fee to move the debt (usually 3%–5%) |

| Regular APR | The rate that kicks in after the promo ends |

| Transfer Deadline | Window to initiate the transfer (often 60–120 days) |

| Credit Limit | Max amount you can transfer to the new card |

What Is a 0% APR Balance Transfer, Exactly?

APR stands for Annual Percentage Rate — it’s the cost of borrowing money expressed as a yearly percentage. On a standard credit card, if you carry a balance month to month, that APR gets divided across 12 months and applied to whatever you owe. At 24% APR, you’re paying about 2% per month in interest. That adds up fast.

A 0% promotional APR on balance transfers means the issuer is temporarily waiving that interest charge on debt you move over from another card.

Here’s a simple example. Say you owe $4,000 on a card charging 22% APR. You’re paying roughly $73 in interest every single month just to exist. Over 18 months, that’s over $1,300 in interest — and your balance barely shrinks if you’re only making minimum payments.

Transfer that $4,000 to a 0% APR card with an 18-month window, and suddenly $0 goes to interest. Every payment reduces the actual debt.

Step-by-Step: How the Process Actually Works

1. You Apply for a Balance Transfer Card

The card has to be from a different bank than where your current debt lives. You can’t transfer a Citi balance to another Citi card. The new issuer reviews your credit and approves you for a credit limit.

2. You Request the Transfer

After approval, you initiate the transfer — usually online or by phone. You provide your old account number and the amount you want to move. Some issuers let you do this during the application process.

3. The New Card Pays Off Your Old Card

The issuing bank sends payment directly to your old creditor. This takes anywhere from 7 to 21 days depending on the institution. Keep paying minimums on your old account until you confirm the transfer went through — missing a payment during this window can hurt your credit.

4. You Repay the New Card at 0% Interest

For the length of the promotional period, no interest accrues on the transferred balance. You make monthly payments, and all of it chips away at the principal.

5. The Regular APR Kicks In After the Promo Period

Whatever balance remains when the promotional period ends starts accruing interest at the card’s standard rate — which can be anywhere from 18% to 29% depending on your credit profile. If you haven’t paid it off by then, the savings start reversing.

What Does a Balance Transfer Actually Cost?

The 0% interest sounds free, but it isn’t entirely.

The Balance Transfer Fee

Almost every card charges a fee to process the transfer — typically 3% to 5% of the amount moved. On $5,000, that’s $150 to $250 charged upfront (added to your new balance).

This fee is worth paying in most cases, but run the math first.

Example:

| Debt Amount | 3% Transfer Fee | 5% Transfer Fee |

|---|---|---|

| $2,000 | $60 | $100 |

| $5,000 | $150 | $250 |

| $8,000 | $240 | $400 |

| $12,000 | $360 | $600 |

Compare that one-time fee against what you’d pay in interest keeping the debt on a 20%+ card for 12–18 months. In most cases, the transfer fee is significantly cheaper.

Cards With No Transfer Fee

A small number of cards waive the transfer fee, though they typically come with shorter promotional periods. If you have a smaller balance and can pay it off quickly, a no-fee card might be the better move.

Real-World Example: The Numbers Side by Side

Scenario: $6,500 in credit card debt at 21% APR. Minimum payment around $130/month.

Option A — Keep the debt on the original card:

- Monthly interest charge: ~$114

- After 18 months of minimums: Balance still over $5,500

- Total interest paid: ~$1,900+

Option B — Transfer to a 0% APR card (3% fee, 18-month promo):

- Transfer fee: $195 (added to balance, so new balance = $6,695)

- Monthly payment needed to clear in 18 months: ~$372

- Total interest paid: $0

- Total cost of the transfer: $195

The difference is stark. Even if you can’t pay $372/month and carry a small remaining balance into the regular APR period, you still come out significantly ahead.

Hidden Risks and Fine Print That Trips People Up

The Promo Clock Starts at Account Opening

Not when you complete the transfer. If it takes you 45 days to initiate the transfer and the card has an 18-month promo period, you effectively have about 16.5 months left. Some cards require the transfer be initiated within 60 or 120 days of account opening to qualify for the promotional rate at all.

New Purchases Are Usually Not Covered

The 0% rate typically applies only to the transferred balance. New purchases often accrue interest at the regular APR from day one. And depending on how the card applies your payments, your new purchases might not get paid down until the transferred balance is gone.

The CFPB requires that payments above the minimum be applied to the highest-APR balance first — but only the excess above the minimum. It’s cleaner to just not use the card for new purchases at all.

One Late Payment Can Void the Entire Promotion

This catches people off guard more than almost anything else. Many card agreements include a clause allowing the issuer to cancel the promotional rate if you miss a payment. You end up back at 25% APR on the full balance. Set up autopay for at least the minimum the day the card arrives.

Deferred Interest vs. True 0% APR

This distinction matters. Deferred interest means the interest is still quietly building in the background — if you don’t pay off the full balance by the end of the promo period, all of that accumulated interest gets added to your balance at once. This is common with store credit cards and some retail financing offers.

True 0% promotional APR means interest simply does not accrue during the promotional window. Always confirm which type you’re dealing with before transferring.

Common Mistakes to Avoid

Transferring a balance you can’t realistically pay off. Divide your total balance (including the fee) by the number of promo months. That’s your required monthly payment. If it doesn’t fit your budget, transfer only what does.

Closing the old card immediately. Closing an account can hurt your credit utilization ratio and shorten your average account age. Neither is great for your credit score. Keep the old card open but don’t use it.

Applying during a sensitive credit period. A balance transfer application involves a hard inquiry. If you’re planning to apply for a mortgage or car loan in the next few months, time it carefully.

Thinking the problem is solved once the transfer goes through. The debt still exists. It just has a temporary 0% rate. The people who don’t benefit from these offers are the ones who transfer the balance, feel relief, and then keep spending on both the old and new card.

Missing the transfer window. Some issuers only allow the promotional rate on transfers made within 60 or 120 days of account opening. Check the terms before procrastinating.

How Does a 0% Balance Transfer Affect Your Credit Score?

Several things happen when you open a balance transfer card:

- A hard inquiry is added to your credit report, usually dropping your score a few points temporarily

- Your average account age decreases slightly with a new account

- Your total available credit increases, which can lower your credit utilization ratio

That last point is actually helpful. If your original card had a $5,000 limit and you were using $4,000 of it, that’s 80% utilization — damaging to your score. Once you transfer the balance, that card shows $0 balance. Your overall utilization drops, which tends to push your score up over time.

According to Experian, credit utilization accounts for about 30% of your FICO score, making it one of the most impactful factors you can actually control in the short term.

Who Should Avoid a 0% Balance Transfer?

Not everyone benefits from this strategy.

People with credit scores below 670. Most cards offering meaningful 0% promotional periods require good to excellent credit. If your score is lower, you might not get approved — or you might get approved for a low credit limit that doesn’t cover your full balance.

Anyone who can’t commit to a monthly payoff plan. If the math requires $300/month and your budget genuinely can’t support that, a debt management plan through a nonprofit credit counseling agency might be a more sustainable path.

People who tend to accumulate new debt. If the pattern is “pay off debt, then build it back up,” a balance transfer doesn’t solve that problem. It just delays it with a temporary interest reprieve.

Those planning a major loan application soon. A new credit card inquiry and account can nudge your score down at exactly the wrong time.

How to Choose the Right 0% Balance Transfer Card

Ask These Four Questions First

1. How long is the promotional period? Longer is almost always better. 18–21 months gives you a realistic payoff window without needing to make massive monthly payments.

2. What’s the transfer fee? 3% is the standard. Some cards charge 5%. A few charge nothing but have shorter promo periods. Do the math based on your specific balance.

3. What’s the regular APR after the promo ends? If there’s any chance you’ll have a remaining balance, a card reverting to 18% is meaningfully better than one jumping to 28%.

4. Is there a transfer deadline? Confirm how long you have to initiate the transfer and get it done before that window closes.

Simple Decision Framework

| Your Situation | Best Move |

|---|---|

| Large balance, need maximum time | Look for 21-month cards, accept 5% fee |

| Smaller balance, can pay fast | Prioritize low or no transfer fee |

| Not sure you’ll pay it off | Pick lowest regular APR, not longest promo |

| Excellent credit | You’ll likely qualify for the best terms |

| Good but not excellent credit | Consider prequalification tools before applying |

Frequently Asked Questions

Does 0% APR mean I don’t have to make payments? No. You still owe monthly minimum payments. Skipping them can trigger late fees, damage your credit, and potentially void the promotional rate. The 0% means no interest, not no payment.

Can I transfer balances from multiple cards? Yes, as long as the total doesn’t exceed your approved credit limit on the new card. You can often transfer from several different accounts at once.

What happens to my old card after the transfer? Nothing automatically. The account stays open with a $0 balance. You decide whether to keep it open (usually better for your credit score) or close it.

Can I transfer a personal loan balance to a credit card? Some issuers allow this, but it depends on the card. Check the specific terms — not all balance transfer offers cover non-credit card debt.

How long does approval take? Many issuers give instant or same-day decisions online. After that, the physical card usually arrives in 7–10 business days, and you can initiate the transfer once the account is active.

Does the 0% apply to the transfer fee? No. The fee gets added to your balance, but it doesn’t earn the promotional rate — or rather, it’s just part of the balance you need to pay off.

Final Thoughts

A 0% APR balance transfer is one of the most straightforward debt-reduction tools available — and when used correctly, it genuinely works. The interest savings are real. The math is solid. The process isn’t complicated.

The only thing standing between a successful balance transfer and a frustrating one is whether you treat it like a structured payoff plan rather than a relief valve. Know your monthly number, set up autopay, leave the card alone for new spending, and watch the balance actually shrink.

That’s it. No tricks. No magic. Just temporarily paused interest and a finite window to get ahead of it.

This article is for informational purposes only and does not constitute financial or legal advice. Always verify current rates, fees, and promotional terms directly with the card issuer before applying.