Financing a big purchase is stressful enough without trying to decode credit card fine print at midnight. Maybe you’re replacing a broken appliance, paying for a home repair, or covering a medical bill that insurance only half-covered. Whatever it is, the idea of splitting a large expense into interest-free payments sounds like an obvious move — and in many cases, it genuinely is.

But these cards aren’t as straightforward as they look in the promotional email. There are traps, timelines, and rules that catch people off guard every single year. This guide breaks down exactly how 0% APR credit cards work for large purchases, which cards are worth considering, what the real risks look like, and how to use one without accidentally turning a smart financial decision into expensive debt.

Table of Contents

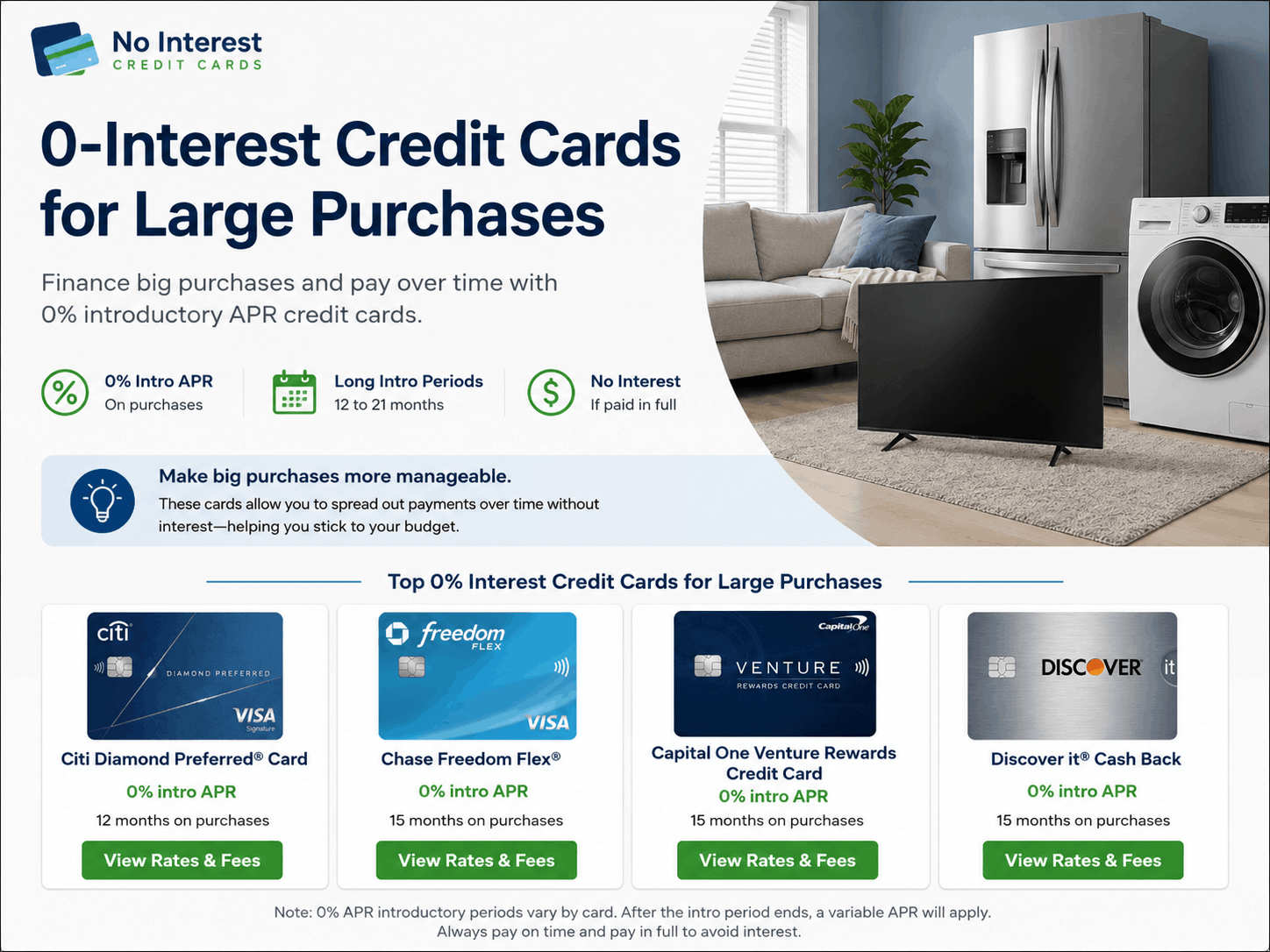

Quick Answer: How 0% APR Cards Work for Large Purchases

A 0% intro APR credit card gives you a set window — typically 12 to 21 months — where no interest is charged on purchases. You still make minimum monthly payments, but every dollar goes toward the actual balance instead of feeding interest charges.

If you pay off the full balance before the promotional period ends, you pay zero interest. If you don’t, the regular APR kicks in — usually somewhere between 19% and 29% depending on your credit profile.

Fast Comparison: Top 0% APR Cards for Large Purchases

Wells Fargo Reflect®

0% Intro Period: Up to 21 months

Regular APR: ~18%–29%

Annual Fee: $0

Best For: Longest 0% window

Citi Simplicity®

0% Intro Period: 21 months (purchases)

Regular APR: ~19%–29%

Annual Fee: $0

Best For: No late fees

Chase Freedom Unlimited®

0% Intro Period: 15 months

Regular APR: ~20%–29%

Annual Fee: $0

Best For: Cash back + 0% combo

Discover it® Cash Back

0% Intro Period: 15 months

Regular APR: ~18%–28%

Annual Fee: $0

Best For: Rewards + 0%

Blue Cash Everyday® (Amex)

0% Intro Period: 15 months

Regular APR: ~19%–29%

Annual Fee: $0

Best For: Everyday spending

APR ranges vary based on creditworthiness at time of approval. Always verify current terms before applying.

What Is a 0% Interest Credit Card for Large Purchases?

It’s a credit card that charges no interest on new purchases during a promotional period set by the issuer. The key phrase here is “promotional period” — after that window closes, the standard variable APR applies to any remaining balance.

This is different from a deferred interest plan, which some retailers offer through store cards. With deferred interest, if you don’t pay the full balance by the deadline, the interest that was building in the background gets charged retroactively — all at once. A true 0% APR card from a major issuer doesn’t work that way. Interest simply doesn’t accrue during the promo period.

Think of it like this: you’re essentially getting a short-term, interest-free loan from the bank, structured as revolving credit. Used with discipline, it’s one of the most practical tools in personal finance for managing a one-time large expense.

Best Cards for Large Purchases: A Closer Look

Wells Fargo Reflect® Card

Best for: People who need maximum repayment time

The Reflect card currently offers one of the longest 0% intro periods available — up to 21 months on purchases and qualifying balance transfers when you meet on-time minimum payment requirements. There’s no annual fee, which matters because carrying a card just to use a promo period and then shelving it shouldn’t cost you money.

The downside: there are no rewards. No cash back, no points, nothing. It’s purely a financing tool. If you’re carrying a significant balance and your priority is paying it down without interest eating into your progress, that’s fine. But if you’re the type who uses credit cards for everyday spending to earn rewards, this won’t serve that goal.

Watch out for: The “up to 21 months” language. The full extension isn’t automatic — it typically requires on-time payments throughout the initial promo window.

Citi Simplicity® Card

Best for: People who occasionally miss payment due dates

The Citi Simplicity has a 21-month 0% period and, importantly, no late fees and no penalty APR. That last part matters more than most people realize. With most credit cards, one missed payment can trigger a penalty APR in the range of 29–30%, which immediately wipes out the benefit of the 0% promo on future purchases or remaining balances depending on the card terms.

Simplicity eliminates that specific risk. It’s not a reason to be careless with payments — your credit score still takes a hit from late payments regardless of card fees — but it provides a meaningful safety net.

No rewards here either, similar to the Reflect card.

Chase Freedom Unlimited®

Best for: People who want 0% financing and ongoing rewards

This card combines a 15-month 0% intro period with unlimited 1.5% cash back on general purchases (plus higher rates in specific categories). After the promo period, it becomes a solid everyday rewards card.

The practical appeal: you’re not just burning a hard credit inquiry for a short-term financing tool. This card has long-term value. If you’re making a large purchase now and plan to keep using the card afterward, the math works in your favor.

The 15-month window is shorter than the Wells Fargo or Citi options, so your monthly payoff targets will be higher. On a $4,500 purchase, you’d need to pay roughly $300 per month to clear the balance in time.

Discover it® Cash Back

Best for: Disciplined spenders who want rewards with their 0% period

Discover’s rotating 5% cash back categories (activated quarterly, up to a spending cap) combined with a 15-month 0% intro period make this card genuinely useful beyond the promo window. The first-year cashback match promotion — where Discover doubles all the cash back you earn in year one — adds real value if you spend consistently.

One consideration: Discover has slightly less merchant acceptance than Visa or Mastercard internationally, though domestic acceptance is nearly universal.

Real-World Cost Examples

Let’s say you need to replace a central air conditioning unit. Average installed cost: around $5,500.

Scenario A — Using a 0% APR card (21-month window):

- Monthly payment needed: ~$262

- Total interest paid: $0

- Total cost: $5,500

Scenario B — Putting it on a regular credit card (24% APR, minimum payments):

- Minimum payment: ~$110/month initially

- Time to pay off: Over 6 years

- Total interest paid: Roughly $3,000+

- Total cost: ~$8,500+

Scenario C — Using a 0% card but not paying it off in time (balance of $1,200 remaining when promo ends at 27% APR):

- The $1,200 now accrues interest at 27%

- Monthly interest charge alone: ~$27

- The card “worked” but left a tail of debt that costs more than expected

Scenario C is where a lot of people land. They start strong, life happens, and the last few hundred or thousand dollars roll into the standard rate. It doesn’t ruin the strategy, but it’s worth planning for.

Hidden Fees and Traps to Know Before You Apply

The Deferred Interest Confusion

As mentioned earlier, some store-branded financing offers look like 0% APR but are actually deferred interest. The interest accumulates during the promo period — it just isn’t charged unless you still have a balance when the promotion ends. At that point, 18–24 months of interest hits your account at once. This is common with furniture stores, electronics retailers, and home improvement financing. Always confirm whether you’re looking at a true 0% APR or a deferred interest arrangement.

Balance Transfer vs. Purchase APR

Many 0% cards offer both a purchase APR promo and a balance transfer promo, but they’re separate. If you’re using the card for new purchases, the purchase promo applies. If you’re moving existing debt from another card, that’s a balance transfer — typically with a fee of 3–5% of the amount transferred. Applying a balance transfer promo to new purchases won’t work, and mixing both on one card can create confusing payment allocations.

What Happens If You Miss a Payment

With most issuers, a missed payment can terminate your promotional APR immediately and trigger the penalty rate. This is the single most common way the 0% strategy collapses. Set up autopay for at least the minimum payment. Then manually pay more on top each month.

The Standard APR After the Promo Ends

This is stated in the card’s terms but rarely emphasized in the marketing. APRs in the 24–29% range are common. If you have $2,000 left when the promotional period expires, you’re now in expensive territory. The math on carrying a balance at those rates moves against you quickly.

Common Mistakes People Make With 0% APR Cards

Not calculating the monthly payment needed upfront. Before you swipe, divide the purchase amount by the number of promo months. That’s your minimum target payment. If that number isn’t realistic given your budget, the card won’t solve your problem — it’ll delay it.

Treating the card as ongoing spending money. The 0% promo is for the large purchase. If you keep adding everyday expenses to the balance, the payoff math breaks down. Some people use a separate card for daily spending and keep the 0% card dedicated to the one purchase they’re financing.

Applying for multiple cards at once. Each application triggers a hard inquiry on your credit report, which temporarily reduces your score. If you’re planning a mortgage or car loan in the near future, stacking credit applications right before is poor timing.

Ignoring the credit utilization impact. If the large purchase brings your utilization on that card near or above 30% of the credit limit, your credit score can drop during the repayment period. This is temporary and recovers as you pay down the balance, but it’s worth knowing.

Closing the card immediately after payoff. Keeping the account open (even if you rarely use it) maintains your available credit and can help your credit age over time. Both are positive factors in most credit scoring models.

Who Should Avoid These Cards

If your credit score is below 670, you may not qualify for the cards with the longest or most favorable promotional periods. Some issuers will approve applicants in the fair credit range but offer a much shorter intro window or a lower credit limit — which may not cover the purchase you had in mind.

If your income or current debt load makes the required monthly payments genuinely unaffordable, a 0% card is the wrong tool. It delays the problem with a deadline attached. A personal loan with fixed monthly payments at a lower rate than your existing credit card debt might be a better structural fit.

If you have a history of carrying balances or frequently paying late, the strategy requires behavioral change to work. That’s not a judgment — it’s just honest. The structure of a 0% card rewards people who are ready to execute a specific payoff plan.

How to Choose the Right Card for Your Situation

Start with the payoff timeline question. How long do you actually need to pay off this purchase comfortably?

- If you need 18–21 months: Look at the Wells Fargo Reflect or Citi Simplicity.

- If you can manage it in 15 months and want rewards: Chase Freedom Unlimited or Discover it.

- If you want no annual fee and the fewest penalties for occasional mistakes: Citi Simplicity.

Then check your credit score before applying. Most of the better cards target good to excellent credit (typically 670+). Experian, Equifax, and TransUnion all offer free credit report access annually through AnnualCreditReport.com. Many banks and credit unions also show your score for free inside the app.

Finally, read the full terms before applying — specifically the regular APR, the penalty APR, and exactly how long the promotional period runs.

Frequently Asked Questions

Does a 0% APR card affect my credit score? Yes, in a few ways. The hard inquiry at application causes a small temporary dip. Carrying a high balance relative to your credit limit also affects your utilization ratio. Both effects are manageable and typically recover within a few months with responsible use.

Can I use a 0% APR card to finance a car or a down payment? Most dealers and sellers don’t accept credit card payments for vehicle purchases. However, some people use 0% APR cards to cover a down payment or associated fees. Check whether the specific transaction will process as a purchase (qualifying for the promo) or a cash advance (which often has no grace period and a higher rate).

What if I can’t pay off the full balance before the promo ends? The remaining balance doesn’t disappear — it begins accruing interest at the standard rate. Pay down as much as possible before the deadline, and consider whether a low-APR personal loan could cover whatever’s left at a better rate than the card’s standard APR.

Is there a minimum purchase amount required? No. The 0% promo applies to any purchase that posts to the card during the promotional window, regardless of amount. But obviously, the strategy is most impactful for larger purchases where interest savings are significant.

How does 0% APR differ from no-interest financing at a store? As explained earlier, many store financing offers use deferred interest — not true 0% APR. With deferred interest, unpaid balances at the end of the promo period are hit with all the interest that accumulated silently. Always ask specifically whether it’s a true 0% APR or a deferred interest offer.

Final Thoughts

A 0% interest credit card for large purchases is a genuinely useful financial tool when you go in with a clear plan. The key variables are the same every time: how much you’re financing, how many months you have, what your realistic monthly payment looks like, and what your credit score qualifies you for.

The promotional period isn’t a trick — it’s a real benefit that banks offer to attract customers. You can use it without getting burned. But it does require actually following through on the payoff. The cards don’t fail people; incomplete plans do.

If the numbers work for your situation, it’s worth pursuing. If they don’t quite add up, it’s better to know that now than to find out when the promo ends.