Home repairs have a way of arriving at the worst possible time. The water heater dies in January. The roof starts leaking before a rainy season. The HVAC system that “just needed a tune-up” turns out to need full replacement. Whatever the situation, you’re suddenly looking at a four-figure bill with no clean way to pay it.

A no interest credit card for home improvement is one of the more practical solutions available — but only if you understand exactly how it works. The promotional offer looks simple on the surface, but the fine print matters more than most people expect. This guide covers the real mechanics, the best card options, the traps to watch for, and how to figure out whether this strategy actually fits your situation.

Table of Contents

Quick Answer: What You Need to Know Upfront

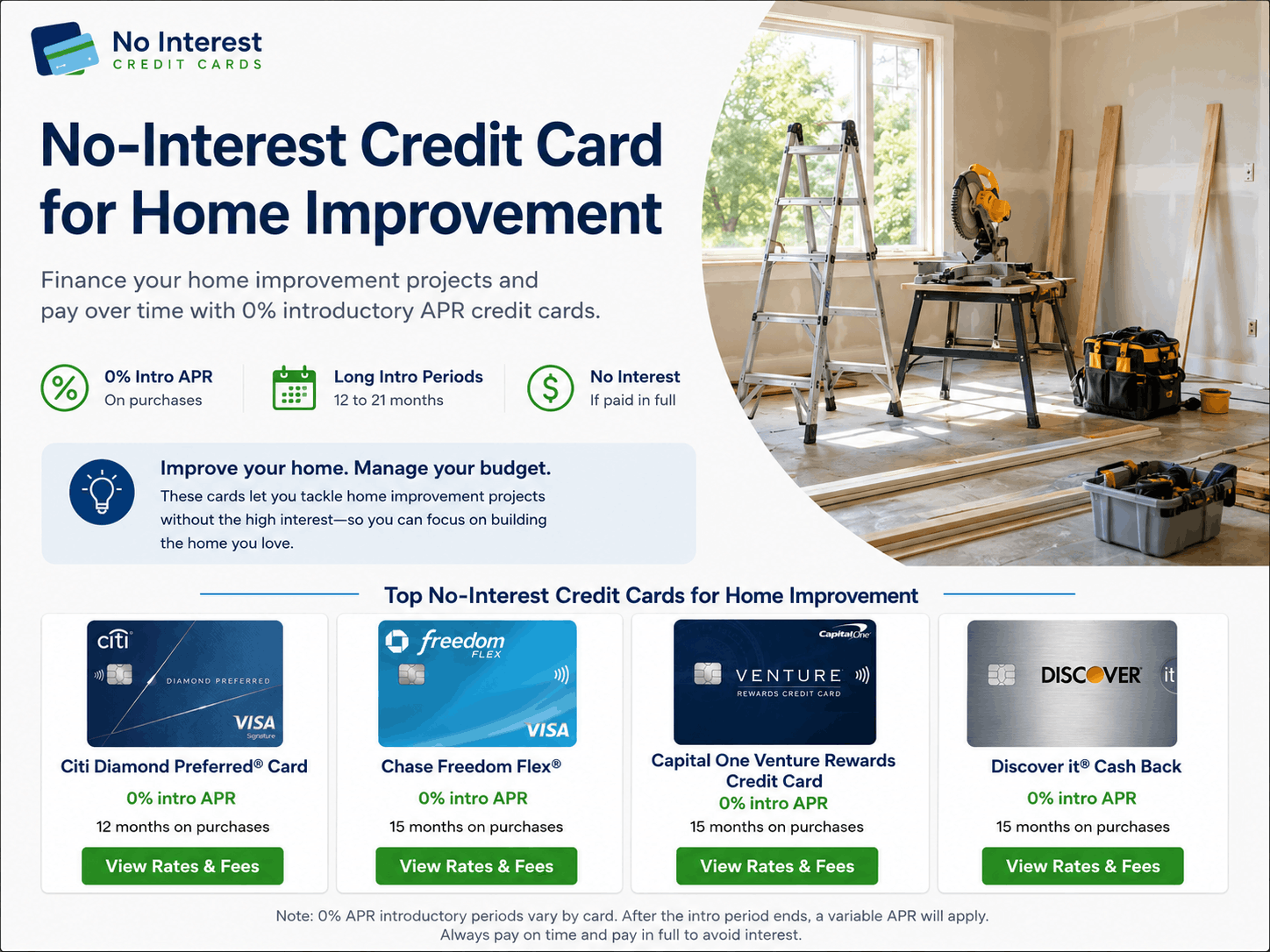

A no interest credit card gives you a promotional window — typically 12 to 21 months — where purchases don’t accrue interest. If you pay off the full balance before that window closes, you finance the renovation at zero cost. If you don’t, the standard APR applies to whatever remains.

Fast Comparison: Top No Interest Cards for Home Improvement

Wells Fargo Reflect®

0% Intro Period: Up to 21 months

Regular APR: ~18%–29%

Annual Fee: $0

Best For: Maximum repayment time

Citi Simplicity®

0% Intro Period: 21 months

Regular APR: ~19%–29%

Annual Fee: $0

Best For: No late fees or penalty APR

Chase Freedom Unlimited®

0% Intro Period: 15 months

Regular APR: ~20%–29%

Annual Fee: $0

Best For: Cash back on contractor spend

U.S. Bank Visa® Platinum

0% Intro Period: 21 months

Regular APR: ~18%–29%

Annual Fee: $0

Best For: Long promo, no rewards distraction

Discover it® Cash Back

0% Intro Period: 15 months

Regular APR: ~18%–28%

Annual Fee: $0

Best For: Rewards + 0% combo

APR ranges reflect variable rates based on creditworthiness. Verify current terms directly with each issuer before applying.

What Is a No Interest Credit Card for Home Improvement?

It’s a standard credit card from a major bank or issuer that offers a promotional period during which no interest is charged on new purchases. The “home improvement” framing is really just about how you’re using it — the card itself doesn’t know you’re buying lumber or hiring a plumber. It’s a general-purpose card with a financing benefit that happens to work well for renovation expenses.

The critical thing to understand: this is different from store financing through Home Depot, Lowe’s, or a contractor’s preferred lender. Those arrangements often use deferred interest — not true 0% APR. With deferred interest, if you carry any remaining balance when the promotional period ends, all the interest that accumulated quietly in the background gets charged to your account at once. Retroactively. That’s a genuinely awful surprise that catches people completely off guard.

A true 0% APR card from Citi, Chase, or Wells Fargo doesn’t work that way. During the promo period, interest simply doesn’t accrue. You’re not borrowing against a hidden ticking clock of accumulated charges.

Best No Interest Cards for Home Improvement: A Closer Look

Wells Fargo Reflect® Card

Best for: Projects with larger price tags that need more time to pay off

The Reflect card offers up to 21 months of 0% APR on purchases — one of the longest windows currently available. There’s no annual fee, which is exactly what you want when the card is essentially serving as a short-term financing vehicle.

The trade-off is straightforward: no rewards. This is a pure financing card. If your renovation runs $6,000 and you want 21 months to pay it down comfortably, the Reflect gives you that runway without charging for it. If you’re also hoping to earn cash back on contractor invoices or material purchases, this card won’t do that.

One detail worth knowing: the full 21-month extension on the promo period isn’t automatic. It typically requires on-time minimum payments throughout the initial window. Read the current offer terms carefully before applying.

Citi Simplicity® Card

Best for: People who want a long promo period with built-in forgiveness for occasional late payments

The Simplicity card stands out because it has no late fees and no penalty APR. That second part is more significant than it sounds. With most credit cards, one missed or late payment can immediately cancel your promotional rate and replace it with a penalty APR that often runs 29–30%. For a large renovation balance, that’s a serious financial hit.

The Simplicity card eliminates that specific risk. Your credit score can still take damage from a late payment — that’s reported to the bureaus regardless of card fees — but your promotional rate stays intact. For homeowners managing a tight budget during a renovation, that safety net has real value.

Like the Reflect, there are no rewards. The 21-month 0% window is the product.

Chase Freedom Unlimited®

Best for: Homeowners who want to earn cash back on renovation spending while financing at 0%

The Freedom Unlimited offers 15 months of 0% APR on purchases along with unlimited 1.5% cash back on general spending (and higher rates in specific categories). For a $5,000 kitchen renovation, that’s $75 back in your pocket just from using the card — before any bonus category spending.

The 15-month window is shorter than the Simplicity or Reflect, so your monthly payoff target will be higher. On a $5,000 balance, you’d need to pay roughly $334 per month to clear it in time. That’s manageable for many households but requires honest budgeting upfront.

The Chase Freedom Unlimited is also a card worth keeping after the renovation is done, which makes the hard credit inquiry more justifiable in the long run.

U.S. Bank Visa® Platinum Card

Best for: Long-window financing without the rewards distraction

The U.S. Bank Platinum card offers up to 21 months of 0% APR on purchases with no annual fee. It’s a quieter card than the Chase or Discover options — no rotating categories, no cash back system to track — just a long promotional period for people who want to focus entirely on paying down a renovation balance.

It’s worth noting that U.S. Bank is a major national issuer with solid customer service and account management tools, which matters when you’re monitoring a large balance over nearly two years.

Discover it® Cash Back

Best for: Disciplined spenders who want rewards and a 0% window together

Discover’s 15-month 0% intro period pairs with a rotating 5% cash back program on quarterly categories — which occasionally includes home improvement retailers or general merchandise. The first-year cashback match promotion doubles everything you earn in year one, which adds up if you’re making significant material purchases.

Discover acceptance is nearly universal domestically. If you’re paying contractors who prefer cards over checks, Discover typically works without issue.

Real-World Cost Examples

Let’s work through a realistic scenario. You need to replace all the windows in a mid-sized home. Total cost from a contractor: $7,200.

Option A — No interest credit card (21-month promo):

- Monthly payment needed to clear balance: ~$343

- Total interest paid: $0

- Total cost: $7,200

Option B — Personal home improvement loan (9% APR, 36 months):

- Monthly payment: ~$229

- Total interest paid: ~$844

- Total cost: ~$8,044

Option C — No interest card, but $1,800 balance remains when promo ends (27% APR):

- That $1,800 now accrues interest monthly

- Monthly interest charge: ~$40

- If only minimums are paid from here, the cost grows quickly

- Total damage depends on how long it takes to pay off the remainder

Option C is worth sitting with. A lot of people execute the plan well for the first 12 months and then hit an unexpected expense — car repair, medical bill, something — and the last few thousand dollars on the renovation card gets deprioritized. The promo ends, the interest starts, and suddenly the “free financing” has a tail.

Hidden Fees and Traps to Understand Before You Swipe

The Deferred Interest Problem With Store Cards

Home Depot’s Project Loan card and similar retail financing products frequently use deferred interest structures. The promotional marketing says “no interest for 24 months,” but the mechanism underneath is different from a bank-issued 0% APR card. If a single dollar of your original balance remains at the deadline, 24 months of accumulated interest — at rates that often exceed 25% — gets charged all at once.

The Consumer Financial Protection Bureau has documented complaints about this specific issue repeatedly. It’s a legal product, but it operates in a way that surprises a lot of borrowers.

The Standard APR After the Promo Ends

This rate is disclosed in the card’s terms, but it rarely gets the attention it deserves during the application process. Variable APRs in the 24%–29% range are common on the same cards that offer attractive intro periods. Whatever balance remains when the promo expires starts accruing at that rate immediately.

Cash Advance Fees on Contractor Payments

Some contractors or service providers don’t accept credit cards, or charge a processing fee to do so. If you’re withdrawing cash from your card to pay a contractor, that transaction typically processes as a cash advance — which has no grace period, a higher APR than purchases, and an upfront fee (usually 3–5% of the amount). The 0% promo does not apply to cash advances.

Balance Transfer Confusion

If you’re also considering moving existing debt to a 0% card, note that balance transfer promos and purchase promos are separate offers with separate rules. Mixing both on one card can create confusing payment allocation issues. Most issuers apply minimum payments to the lower-APR balance first — which means purchases at 0% get paid down while a higher-rate balance sits. Read the payment allocation terms carefully if you’re using one card for both purposes.

Common Mistakes Homeowners Make With These Cards

Underestimating the total project cost. Renovation budgets expand. What starts as a $4,000 bathroom remodel can become $6,500 with tile overruns, plumbing surprises, and permit fees. If the expanded cost pushes your balance beyond what you can realistically pay in the promo window, the math shifts.

Not calculating the monthly target before applying. Divide the expected renovation cost by the promo months. That’s your minimum monthly payment to break even. If that number doesn’t fit your monthly cash flow, the card won’t solve the problem — it’ll delay it with a deadline.

Using the card for ongoing household expenses after the renovation. This is how balances grow beyond the original plan. If the 0% card becomes your everyday card, the payoff calculation breaks down every month.

Applying for multiple cards around the same time. Each credit card application triggers a hard inquiry on your credit report, which causes a temporary score drop. Applying for three cards in a month to compare options isn’t a smart move — especially if you’re also considering a home equity line or refinance in the same timeframe.

Closing the card after payoff. An open card with a zero balance improves your credit utilization ratio and contributes to your average account age — both positive factors in FICO scoring. Unless there’s a compelling reason, keeping the account open costs nothing and quietly helps your credit profile.

Who Should Avoid Using a No Interest Card for Home Improvements

If your credit score is below 660–670, your approval odds for the best 0% promo cards are lower, and the offers you do qualify for may have shorter windows or lower credit limits that don’t cover the full project cost.

If your current debt-to-income ratio is already stretched — meaning you’re juggling multiple monthly obligations — adding a large card balance with a fixed payoff deadline creates pressure that may be hard to sustain.

If the renovation is urgent and large (think: $15,000+ structural repair), a no interest card may not cover the full cost depending on the credit limit you’re approved for. In that situation, a home equity loan or HELOC often provides larger loan amounts at lower interest rates, with fixed payments that don’t expire on a deadline.

If you’ve had difficulty paying cards on time in the past, the strategy requires a behavioral change to work. The card doesn’t manage the repayment — you do.

How to Choose the Right Card for Your Renovation

Start with the total project cost and a realistic monthly budget. How much can you commit to this card each month without straining other obligations?

- Divide the total cost by your comfortable monthly payment amount.

- The result tells you how many months you need.

- If you need 18+ months, look at the Wells Fargo Reflect, Citi Simplicity, or U.S. Bank Platinum.

- If 15 months works and you want rewards on the spend, Chase Freedom Unlimited or Discover it are solid choices.

Then check your credit score through Experian, Equifax, or your bank’s free score tool before applying. Knowing where you stand helps you target cards you’re likely to qualify for — which protects your credit from unnecessary hard inquiries.

Finally, confirm with your contractor how they accept payment. Credit card, check, bank transfer, or a combination. Some larger contractors charge a card processing fee (typically 2–3%), which slightly reduces the interest savings benefit.

Frequently Asked Questions

Can I use a no interest credit card to pay a contractor directly? Yes, as long as the contractor accepts credit card payments. Many do, especially larger firms. Verify beforehand, and ask whether there’s a processing fee — some pass that cost to the customer.

What happens if my renovation goes over budget and I can’t pay off the full balance? The remaining balance starts accruing interest at the standard APR when the promo ends. You haven’t lost everything — you just have a smaller high-interest balance to manage. Consider whether a low-rate personal loan could pay off the remainder more efficiently than carrying it on the card.

Does applying for a home improvement credit card hurt my credit score? The application triggers a hard inquiry, which typically causes a small, temporary drop — usually 5 points or less. This recovers within a few months of responsible use.

Is it better to use a no interest card or a HELOC for home improvements? It depends on the project size and your financial situation. A no interest card is faster to obtain, requires no home equity, and charges nothing if paid off in time. A HELOC provides larger loan amounts, typically at lower long-term rates, but uses your home as collateral and involves closing costs and a longer application process. For projects under $10,000, the no interest card is often simpler. Above that range, it’s worth comparing both options.

What credit score do I need to qualify? Most cards with the best 0% promotional periods target applicants with good to excellent credit — roughly 670 and above by FICO standards. Some issuers approve applicants in the fair credit range but may offer less favorable terms.

Final Thoughts

A no interest credit card for home improvement is a genuinely useful financing tool when the project size, your credit score, and your monthly budget are all aligned. The math is clean: borrow what you need, pay it off before the deadline, pay nothing in interest.

What makes or breaks the strategy isn’t the card — it’s the plan behind it. Know your monthly target payment before you apply. Keep the card dedicated to the renovation. Set up autopay so a missed due date doesn’t end the promo early. And if your budget shifts mid-project, address it directly rather than hoping to catch up later.

Used with discipline, this is one of the more straightforward financing options available to homeowners. Used without a plan, it’s a delayed bill with an expiration date and a high interest rate on the other side.