Medical debt is one of the most emotionally loaded financial problems people face. Unlike a car loan or a planned renovation, a medical bill often arrives without warning — after a hospital stay, an emergency procedure, or a diagnosis that changed everything. You didn’t choose the expense. You didn’t have time to save for it. And now you’re staring at a statement with a balance that feels impossible.

A 0 APR credit card for medical bills is one practical option worth understanding. When used correctly, it lets you pay down a large medical balance over time without interest eating into every payment. But the mechanics matter, and there are real risks that aren’t always obvious. This guide covers how these cards work, which options make sense for medical expenses specifically, and what to watch out for before you apply.

Table of Contents

Quick Answer: How 0 APR Cards Work for Medical Bills

A 0% intro APR credit card gives you a set promotional window — typically 12 to 21 months — where no interest accrues on purchases. If you charge your medical expenses to the card and pay off the full balance before the promo period ends, you pay zero in interest. If you still have a balance when the promotion expires, the standard variable APR kicks in on whatever remains.

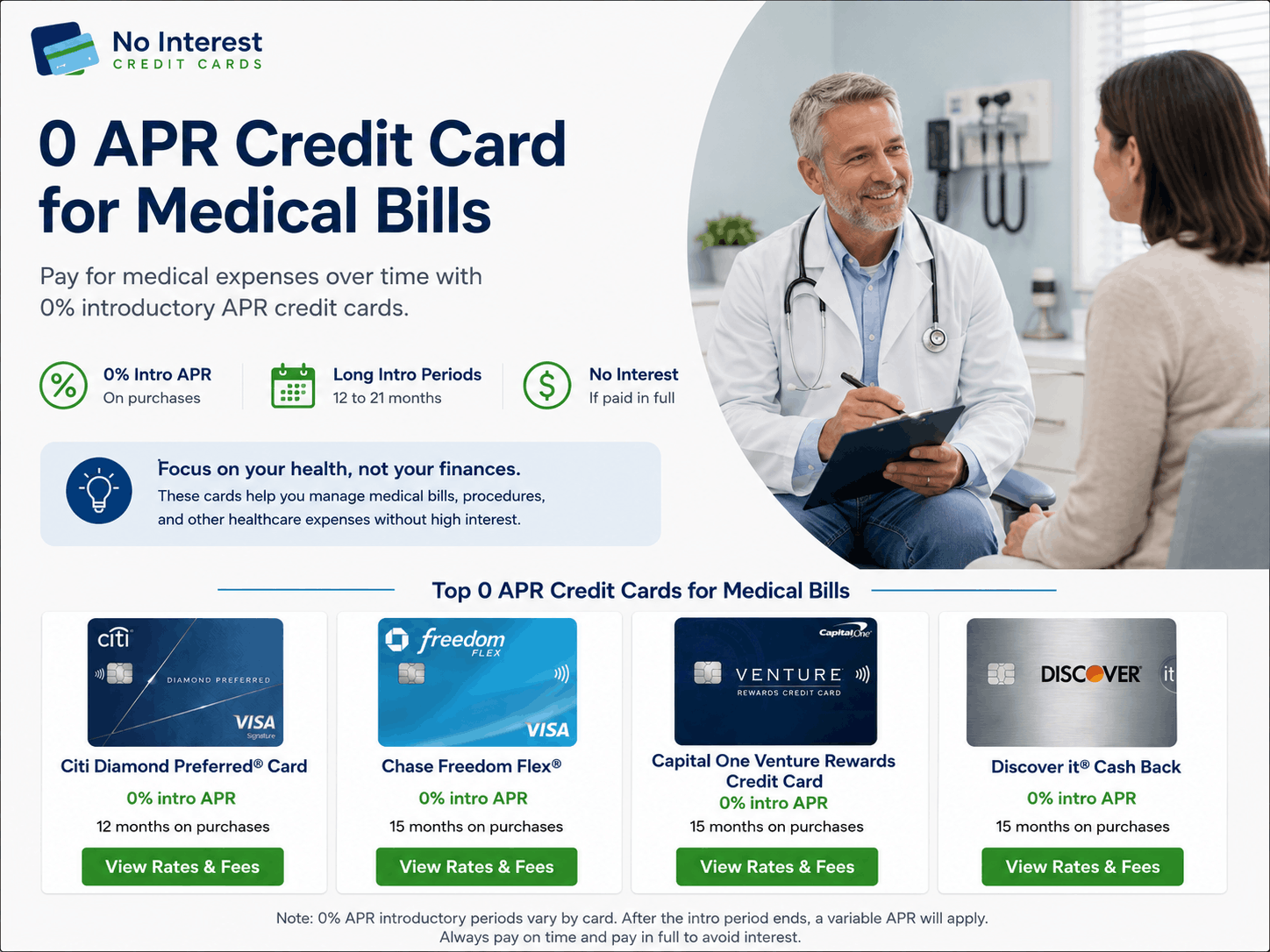

Fast Comparison: Best 0 APR Cards for Medical Expenses

Wells Fargo Reflect®

0% Intro Period: Up to 21 months

Regular APR: ~18%–29%

Annual Fee: $0

Best For: Maximum payoff window

Citi Simplicity®

0% Intro Period: 21 months

Regular APR: ~19%–29%

Annual Fee: $0

Best For: No late fees or penalty APR

U.S. Bank Visa® Platinum

0% Intro Period: 21 months

Regular APR: ~18%–29%

Annual Fee: $0

Best For: Long promo, clean terms

Chase Freedom Unlimited®

0% Intro Period: 15 months

Regular APR: ~20%–29%

Annual Fee: $0

Best For: Cash back on medical spend

Discover it® Cash Back

0% Intro Period: 15 months

Regular APR: ~18%–28%

Annual Fee: $0

Best For: Rewards + 0% promo

APR ranges are variable and depend on your credit profile at approval. Always confirm current terms with the issuer before applying.

What Is a 0 APR Credit Card for Medical Bills?

It’s a general-purpose credit card — not a medical-specific product — that comes with a promotional period during which purchases don’t accrue interest. You can use it anywhere that accepts credit cards, including hospitals, outpatient clinics, specialist offices, labs, and pharmacies. The card doesn’t care what you’re buying. You’re essentially getting a short-term interest-free loan, structured as revolving credit, that you can use to cover a medical expense and repay over the promo window.

This is meaningfully different from CareCredit or other medical financing products. CareCredit is a healthcare-specific card that often uses deferred interest rather than true 0% APR. With deferred interest, if any balance remains when the promotional period ends, the interest that accumulated silently during the entire promo period gets charged all at once. That’s a serious trap that catches a lot of patients off guard — especially on large balances where the retroactive interest charge can be hundreds or even thousands of dollars.

A bank-issued 0% APR card eliminates that risk. Interest simply doesn’t accrue during the promotional window. There’s no hidden balance building in the background.

Best 0 APR Cards for Medical Bills: A Closer Look

Wells Fargo Reflect® Card

Best for: Large medical balances that need maximum repayment time

The Reflect card currently offers up to 21 months of 0% APR on purchases with no annual fee. For a significant medical expense — surgery, a hospitalization, a complex treatment plan — that runway gives you nearly two years to pay down the balance without interest. On a $6,000 balance, you’d need roughly $286 per month to clear it in 21 months. That’s a manageable number for many households.

There are no rewards on this card. It’s built purely as a financing vehicle, which is fine if your goal is managing a specific large expense rather than ongoing credit card use.

One important detail: the full 21-month window may require on-time minimum payments throughout the initial promotional period to maintain the extension. Read the specific offer terms at application.

Citi Simplicity® Card

Best for: Patients managing tight budgets who want protection against one late payment

The Simplicity card offers 21 months of 0% APR and stands out because it has no late fees and no penalty APR. That combination matters more for medical debt than most other situations. When you’re dealing with a health issue, your finances can be disrupted in multiple ways simultaneously — reduced work hours, additional out-of-pocket costs, unexpected follow-up expenses. A month where you pay late or short shouldn’t terminate your promotional rate and drop you into 29–30% APR territory.

With the Citi Simplicity, your rate stays intact even after a late payment. Your credit score can still be affected by late payments reported to Experian, Equifax, or TransUnion — that part doesn’t change — but the card itself won’t penalize you financially on top of that.

No rewards, no frills. But for a medical financing scenario, the safety net has real practical value.

U.S. Bank Visa® Platinum Card

Best for: Straightforward long-window financing without complexity

The U.S. Bank Platinum offers up to 21 months of 0% APR on purchases with no annual fee. It’s a clean, no-distraction card — no rotating categories to track, no rewards system to manage. If your goal is simply to finance a medical expense and pay it off systematically over time, this card does exactly that.

U.S. Bank is a major national institution with solid account management tools, which matters when you’re monitoring a balance for nearly two years.

Chase Freedom Unlimited®

Best for: Patients who want to earn rewards on medical and pharmacy spending

The Freedom Unlimited offers 15 months of 0% APR along with unlimited 1.5% cash back on general purchases. On a $5,000 medical bill, that’s $75 back — not life-changing, but real money at a time when every dollar matters.

The 15-month window is shorter, so monthly payments need to be higher. On $5,000, you’d need about $333 per month to clear the balance before the promo expires. That requires honest upfront budgeting.

The card has long-term value beyond the promotional period, which makes the hard credit inquiry more defensible if you’re concerned about the temporary score impact.

Discover it® Cash Back

Best for: Disciplined payers who want rewards and the first-year cashback match

Discover’s 15-month 0% period paired with the first-year cashback match — where Discover doubles all cash back earned in year one — can add meaningful value on large medical spending. If your total out-of-pocket medical costs hit $4,000–$5,000 in year one across multiple providers and pharmacies, the cashback match on that spending adds up.

Domestic acceptance is nearly universal, which matters for hospital billing systems, specialist offices, and pharmacy point-of-sale terminals.

Real-World Cost Examples

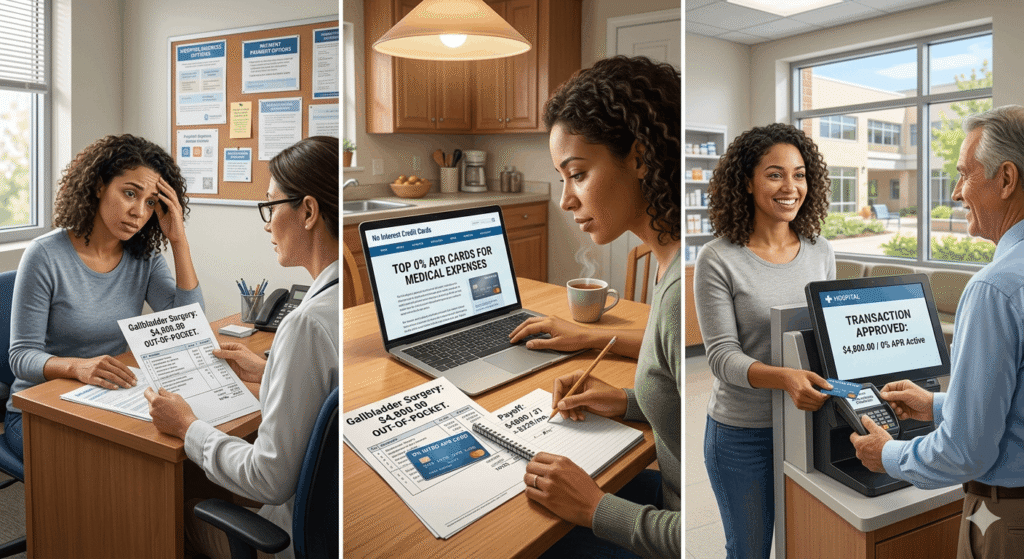

A patient receives a bill for gallbladder surgery after insurance. Total out-of-pocket: $4,800.

Option A — 0 APR credit card (21-month promo):

- Monthly payment target: ~$229

- Total interest paid: $0

- Total cost: $4,800

Option B — Carry balance on existing card (22% APR, minimum payments):

- Minimum payment starts around $96/month

- Payoff timeline: 5+ years

- Total interest paid: ~$2,600+

- Total cost: ~$7,400+

Option C — Medical financing card with deferred interest (same 21-month window):

- Pay $200/month, but $400 remains at deadline

- 21 months of accumulated interest at 26% charges retroactively: potentially $400–$600 in one shot

- Total cost: More than expected, more than the 0 APR card

Option D — 0 APR card, but $1,200 remains when promo ends (26% APR):

- Monthly interest charge: ~$26

- Total cost depends on how quickly the remainder is paid off

- Still better than Option B, but more expensive than the original plan

The difference between Option A and Option B is over $2,600. For an unplanned medical expense, that gap is genuinely significant.

Hidden Fees and Traps That Apply to Medical Bills Specifically

The Deferred Interest Problem With Medical Financing Cards

CareCredit, Synchrony-issued medical financing, and similar products are widely offered at healthcare provider offices. The promotional terms look similar to a 0% APR card, but the mechanism underneath is often deferred interest. If even one dollar of your original balance remains at the deadline, all accumulated interest — at rates that frequently exceed 26% — gets charged immediately.

The Consumer Financial Protection Bureau has received numerous complaints about this specific practice. These products are legal and some patients use them successfully, but the margin for error is thin. A bank-issued 0% APR card is structurally safer.

Hospital Bill Negotiation Before You Charge Anything

This is worth mentioning because it affects the base number you’re financing. Hospitals — particularly nonprofit ones — often have financial assistance programs, income-based sliding scale discounts, or the ability to negotiate the billed amount before it goes to collections. According to the CFPB, patients have the right to request an itemized bill and dispute charges that appear incorrect.

If you can reduce a $6,000 bill to $4,200 through negotiation or financial assistance, you’re financing $4,200 — not $6,000. That changes the monthly payment math significantly.

Charging vs. Paying Later: Some Hospitals Bill Differently

If a hospital sends you to collections before you can get a credit card involved, the card is less useful. Medical bills typically go to collections after 90–180 days of nonpayment. If you have a large bill and plan to use a 0% card, act quickly — contact both the hospital billing department and the card issuer to understand how the transaction will process.

Cash Advance Distinction

Paying a hospital directly by credit card processes as a purchase, which qualifies for the 0% promo. Withdrawing cash from your card to pay a provider who doesn’t accept cards processes as a cash advance — which carries a separate, higher APR and an upfront fee (typically 3–5%). The 0% promo does not cover cash advances under any circumstances.

The Standard APR After the Promo Ends

This is disclosed in the card agreement but easy to overlook during the application process. Variable rates of 24%–29% are common on the same cards that advertise attractive intro periods. Whatever balance remains when the promotion expires immediately begins accruing at that rate.

Common Mistakes Patients Make With 0 APR Cards for Medical Debt

Not confirming the provider accepts credit cards. Most hospitals and large practices do. Some smaller specialty providers or individual practitioners don’t, or charge a processing fee. Verify before you apply.

Not calculating the monthly payment target before applying. The math is simple: divide the bill by the number of promo months. If that number doesn’t fit your monthly budget, the card won’t solve the problem. It’ll delay it until the promo ends.

Using the card for everyday purchases on top of the medical balance. Every dollar added to the balance raises the monthly payment needed to clear it in time. If the card is for financing a medical bill, keep it for that purpose only.

Ignoring the bill negotiation step. Applying for a credit card before attempting to reduce the bill is a sequencing mistake. Negotiate first, then finance whatever remains.

Applying right before a mortgage or major loan application. Each credit card application generates a hard inquiry. If you’re planning to apply for a home loan or refinance in the next few months, timing your credit card application carefully — or waiting — may be worth discussing with a lender.

Not setting up autopay. With most cards, a single missed payment can cancel the promotional rate and trigger a penalty APR. Setting up autopay for at least the minimum payment eliminates that risk.

Who Should Avoid Using a 0 APR Card for Medical Bills

If your credit score is below 660–670, approval odds for the best 0% promo cards are lower, and the offers you qualify for may come with shorter promotional windows or lower credit limits that don’t cover the full bill.

If your monthly budget is already tight and the required monthly payment to clear the balance in time isn’t realistic, the card creates a deadline you may not be able to meet. A medical payment plan negotiated directly with the hospital — often available at 0% interest or low fees — may be a better structural fit. Many hospitals are legally required to offer financial assistance under IRS nonprofit rules and will provide interest-free payment plans for patients who qualify.

If the medical bill is large enough that it genuinely requires a personal loan or home equity product, a credit card may not provide enough credit limit to cover the full amount. Personal loans for medical expenses from lenders like LightStream or SoFi can offer fixed rates well below standard credit card APRs for qualified borrowers.

How to Choose the Right Card for Your Medical Expense

Start by knowing the exact amount you need to finance. Then work backward:

- Divide the total by the number of months you can comfortably pay.

- That result tells you how long a promotional window you need.

- If you need 18+ months: Wells Fargo Reflect, Citi Simplicity, or U.S. Bank Platinum.

- If 15 months works and you want cash back: Chase Freedom Unlimited or Discover it.

- If payment consistency is a concern: Citi Simplicity, because there’s no penalty APR.

Check your credit score through Experian, Equifax, TransUnion, or your bank’s free tool before applying. It takes two minutes and helps you target cards you’re likely to qualify for — which protects your credit from unnecessary hard inquiries on applications that won’t be approved.

If you haven’t already, contact the hospital or provider billing department before charging anything. Ask specifically about financial assistance programs, itemized bill review, and whether a direct payment plan is available. Some patients find they can reduce the bill significantly or eliminate the financing need entirely.

Frequently Asked Questions

Can I use a 0 APR credit card to pay any medical provider? Most hospitals, urgent care centers, specialist offices, labs, and pharmacies accept credit cards. Some smaller practices or providers may not, or may add a processing fee. Always confirm before you rely on the card for payment.

Is CareCredit the same as a 0 APR credit card? No. CareCredit and similar medical financing products often use deferred interest, which works very differently from a true 0% APR card. With deferred interest, unpaid balances at the deadline trigger all accumulated interest retroactively. A bank-issued 0% APR card from Citi, Chase, or Wells Fargo doesn’t have that mechanism.

What if the medical bill goes to collections before I can use a card? Once a bill is with a collections agency, paying by credit card may or may not be possible depending on the agency. Act quickly — most providers send bills to collections after 90–180 days. If you have a large upcoming medical expense, plan the card application as early as possible.

Does financing medical bills with a credit card affect my credit score? The application itself causes a small temporary dip from the hard inquiry. Carrying a large balance relative to your credit limit can affect your utilization ratio. Both effects are manageable and recover with responsible use and payoff progress.

Are there medical-specific credit cards worth considering? CareCredit and Alphaeon Credit are commonly offered at healthcare provider offices. They can work — but only if you pay the full balance before the promo deadline. They’re structurally riskier than bank-issued 0% cards due to deferred interest. For most patients who qualify for a bank card, the bank card is the safer option.

Final Thoughts

A 0 APR credit card for medical bills is a legitimate, practical tool for managing an expense that arrived without invitation. The interest savings over a 15–21 month period can be substantial — often more than $1,000 on a mid-sized medical balance compared to carrying that debt on a standard card.

What the card can’t do is make the bill smaller or manage the repayment for you. Before applying, negotiate the bill if possible, know exactly what monthly payment you can sustain, and pick a card whose promo window matches your realistic payoff timeline.

The plan itself isn’t complicated. The discipline to follow through is the part that matters.