Meta Description: Wondering how a no interest credit card really works? Learn the truth about 0% APR credit cards — the rules, the risks, hidden costs, and the best 0 percent interest credit cards of 2026.

A few years back, I had about $4,800 sitting on a Capital One card charging me 24.99% APR. Every month I’d pay $120 minimum, watch maybe $20 of it go toward the actual balance, and just… feel stuck. It was like running on a treadmill. Fast.

A friend who works in banking casually mentioned a balance transfer to a 0% APR card. My first reaction? Skepticism. “Nothing’s free,” I said. And honestly? I wasn’t entirely wrong. But I also wasn’t entirely right. Because when you use a no interest credit card the smart way, it genuinely can save you hundreds — sometimes thousands — in interest charges.

The catch is that most people don’t fully understand how these cards work. They jump in, make a mistake or two, and end up worse off than before. So let’s break this down properly — no fluff, no misleading promises. Just the real mechanics, the rules you have to follow, and whether one of these cards makes sense for you.

Table of Contents

What Exactly Is a “No Interest” Credit Card?

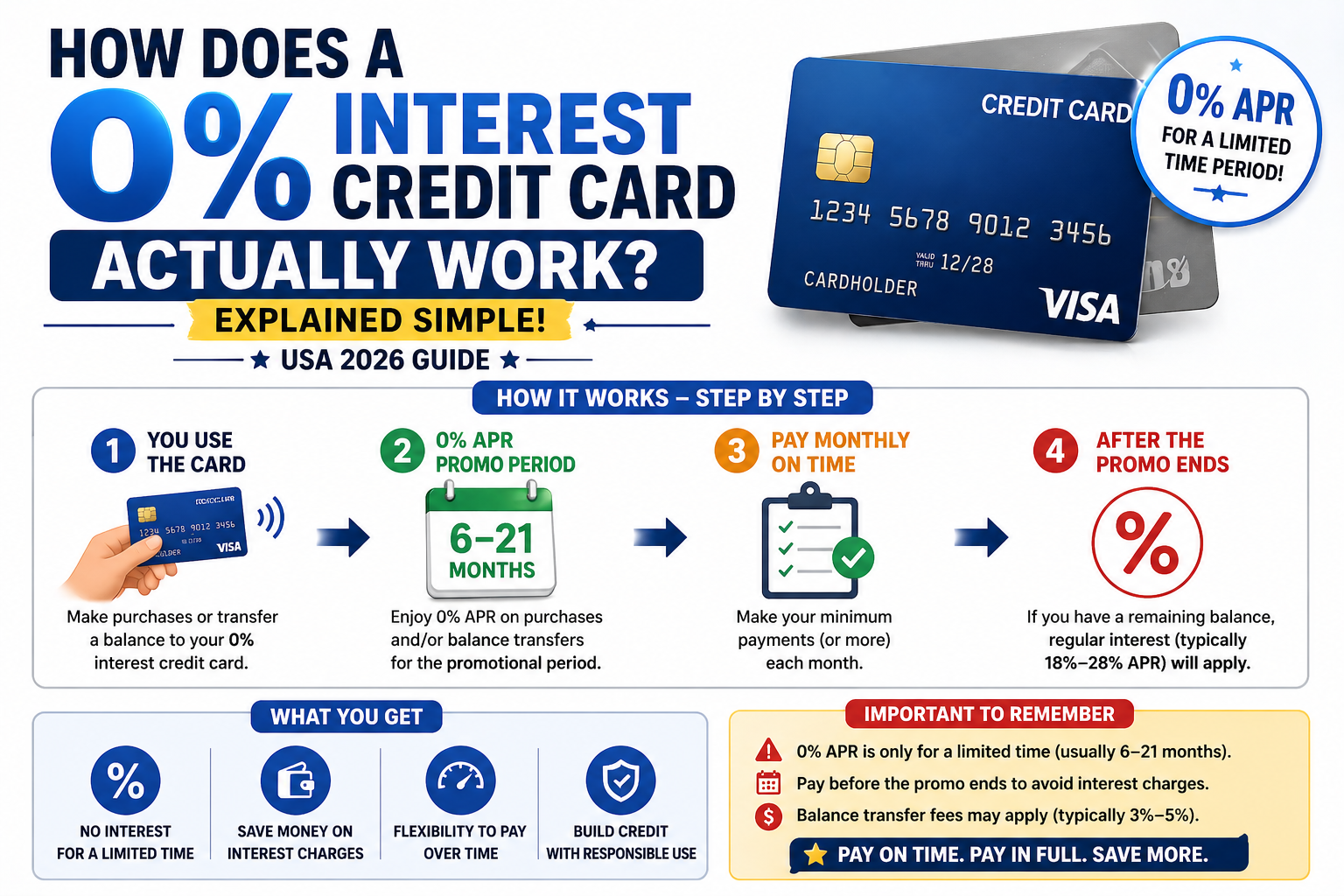

Let’s clear up the terminology first. When people say “no interest credit card” or “zero interest credit card,” they’re almost always talking about a 0% introductory APR offer. This is not a permanent feature of the card. It’s a promotional period — usually ranging from 12 to 21 months — during which the card issuer charges you zero interest on purchases, balance transfers, or both.

After that promotional window closes? The card’s regular APR kicks in, and that rate is typically somewhere between 16% and 29% depending on your credit score and the card. Not exactly pocket change.

So when you see “0% APR for 21 months,” what you’re really reading is: “We’ll give you nearly two years to pay off your balance without charging you interest — but after that, all bets are off.”

There are two main flavors of 0% APR offers:

1. 0% on Purchases — You charge things to the card, and those new purchases don’t accrue interest during the promotional period. Great for big planned expenses like a home renovation, new appliances, a vacation, or medical bills.

2. 0% on Balance Transfers — You move existing high-interest debt from another card onto this new card, and that transferred balance sits interest-free during the promo period. This is the version that saved me about $600 in interest on my own debt journey.

Some cards offer both. Some only offer one. Reading the fine print matters here.

How Does It Really Work? (The Actual Mechanics)

Here’s where a lot of people get confused. The concept sounds simple but the execution has a few nuances worth knowing.

For New Purchases

Say you get approved for a no interest credit card with a 0% intro APR on purchases for 18 months. You immediately use it to buy $3,000 worth of new kitchen appliances. During those 18 months, you can carry that $3,000 balance without a single dollar of interest being added — as long as you make at least the minimum payment each month.

Think of it like an interest-free loan from the bank. They’re betting that either (a) you won’t pay it all off in time and they’ll collect interest after the promo period, or (b) you’ll end up using the card for other purchases long-term. The bank isn’t doing this out of charity.

For Balance Transfers

This one’s slightly more involved. Let’s say you have $5,000 on a high-interest card. You apply for a 0% balance transfer card, get approved, and request a transfer. The new card pays off your old card, and now that $5,000 sits on your new card — ideally charging you 0% for the next 15 to 21 months.

One critical detail: balance transfers usually have to be completed within a specific window — often 60 to 120 days from account opening — to qualify for the 0% rate. Miss that window? You could end up paying the card’s regular APR on the transferred amount from day one.

What Happens When the Promotional Period Ends

This is where things get uncomfortable for a lot of people. Any remaining balance after the promotional period expires immediately starts accruing interest at the card’s regular APR. And these rates are often high — we’re talking 17% to 28%+.

Here’s the important distinction from deferred interest (which you’ll find on some store credit cards): with a true 0% APR card, there’s no retroactive interest. If you had $500 left at the end of your 18-month promo period, you only start paying interest on that $500 going forward. You’re not suddenly slapped with 18 months of back-interest on your entire original balance. That’s a deferred interest trap, and it’s a different beast entirely — one you want to avoid.

Key Rules You Must Follow (Seriously, Don’t Skip This)

Using a no interest credit card is a little like driving on a highway with very specific speed limits. Stay in the lane, follow the rules, and you’ll be fine. But one slip can cost you the entire benefit.

Rule #1: Always Make the Minimum Payment On Time

This is non-negotiable. If you miss a payment or pay late, many card issuers will immediately revoke your 0% APR offer. Your rate can jump to the card’s regular APR — or worse, a penalty APR, which can be around 29.99%. And once that’s gone, it’s usually gone for good.

Set up autopay for at least the minimum. Every single month. Don’t rely on memory.

Rule #2: Don’t Exceed Your Credit Limit

Going over your credit limit can also void the promotional rate on some cards. Keep your utilization in check.

Rule #3: Know Your Transfer Deadline

For balance transfers, the clock starts ticking the moment your account opens. Balance transfers must typically be completed within 60 days of account opening to qualify for the intro APR — though some cards allow up to 120 days. If you miss that window, you don’t get the 0% rate on the transferred balance.

Rule #4: Understand Payment Allocation

When you pay more than the minimum, the extra money goes toward the balance with the highest interest rate first. This is actually helpful in most cases — but it means if you have a mix of balances (say, a promotional purchase and a cash advance), the payment logic matters.

Balance Transfer Fees, Hidden Costs & Real Examples

Let’s talk money, because this is where the “no interest” label can be a little misleading.

Balance Transfer Fees

Almost every 0% balance transfer card charges a fee when you move debt onto it. A balance transfer fee is generally 3% or 5% of the amount you transfer. So a $5,000 balance transfer with a 5% fee would come out to $250.

Is $250 worth it? In most cases, yes — if you’re moving debt from a card charging 22% APR and you need 18 months to pay it off, you’d have paid far more in interest. But if your existing card only charges 10% and you’d pay it off in 4 months anyway, the math doesn’t work as well.

Always run the numbers before you transfer.

Here’s a quick real-world example:

You have $6,000 on a card at 24% APR. You transfer it to a card with 0% for 18 months and a 3% balance transfer fee ($180). You now owe $6,180 — but you pay it down over 18 months ($343/month) and pay zero additional interest. Compare that to paying $343/month on the original 24% APR card, where you’d still owe about $1,200 at the end of 18 months and have paid roughly $1,100 in interest. The $180 fee just saved you nearly $1,100.

Purchase APR After the Promo Period

Any balance that’s left on your account when the intro period ends will begin to accrue interest at your assigned ongoing APR. For many of the popular 0% cards, that rate lands anywhere from 16% to 28%+. Know this number before you apply.

Annual Fees

Most of the best 0% APR cards don’t charge annual fees. That’s actually one of their more attractive features. But always double-check — some premium cards with 0% intro offers do carry annual fees, and that changes your break-even calculation.

Pros and Cons: The Honest Breakdown

I’ll be real with you here. These cards are genuinely useful tools — but they’re not magic, and they’re not for everyone.

The Pros

Interest savings can be substantial. If you’ve got high-interest debt and can qualify, the savings are real and often significant. We’re talking hundreds to thousands of dollars over a 12–21 month period.

Planned purchases become manageable. Need a new HVAC unit? Unexpected medical bill? A 0% card lets you spread payments over 12–21 months without paying a premium to do so.

Many cards also earn rewards. Several 0% APR cards also offer cash back or points on purchases, so you’re not giving up rewards just to avoid interest.

No annual fee on most options. You’re not paying for the privilege of borrowing interest-free.

The Cons

The promotional period ends. That’s the big one. If you haven’t paid off your balance, you’re suddenly dealing with a regular APR that can be quite high.

Balance transfer fees add up. That 3%–5% fee is real money. Factor it into your savings calculation.

You need good-to-excellent credit to qualify. Many 0% APR credit cards require a good or excellent credit score to qualify, which is at least a 670 FICO score. If your credit is damaged, you likely won’t get approved for the best offers.

It’s a temporary solution, not a cure. If you transfer $8,000 in debt but keep spending on the old card, you’ve made things worse, not better.

Psychological risk. Having a fresh, zero-balance card in your wallet can tempt you to spend more. This is a real pattern I’ve seen (and experienced). Discipline matters.

Who Should Get One — And Who Should Probably Skip It

Not every financial tool is right for every situation. Here’s my honest take.

You’re a Good Candidate If…

- You have existing high-interest credit card debt and a realistic plan to pay it off within 12–21 months

- You’re planning a large, necessary purchase (home repair, medical expense) and need time to pay it off without interest

- You have a credit score of 670 or higher

- You have the discipline to make payments on time — every month — and not run up new debt on the old card

- You’ve done the math and confirmed the balance transfer fee is worth it

You Should Probably Skip It If…

- You tend to carry a balance because of overspending (not a one-time emergency)

- Your credit score is below 670 — you likely won’t qualify for the best offers

- You can’t commit to paying off the balance before the promo period ends

- You have an ongoing problem with overspending — once the intro period ends, you’ll take on interest at the card’s regular ongoing interest rate, which may be 20% APR or even higher

- You’re considering a balance transfer but you’d need 3+ years to pay it off — you’d be better off negotiating directly with your creditor or looking at a personal loan

Best Practices & Smart Strategies to Maximize a 0% APR Card

If you’ve decided this card makes sense for you, here’s how to actually squeeze maximum value out of it.

Calculate your exact monthly payment from day one. Divide your total balance by the number of months in the promo period. That’s your target monthly payment. Set it up in autopay.

Don’t use the old high-interest card again. If you transfer a balance, leave that old card alone. Using it defeats the entire purpose. Cut it up if you have to.

Set a calendar alert 60 days before the promo period ends. This gives you time to either pay off the remaining balance, request a 0% extension (some issuers offer this), or consider another balance transfer if needed.

Treat the promotional period like a countdown, not a comfort zone. I can’t stress this enough. It’s not “free money” — it’s borrowed time.

Avoid cash advances entirely. Cash advances on credit cards are almost never included in 0% promotions. They typically carry a separate, higher rate and fees. Don’t touch them.

Keep your credit utilization in check. Opening a new card and moving a large balance onto it can spike your utilization ratio temporarily. If you need your credit score for something important (like a mortgage application) in the next few months, think carefully about timing.

Best 0% APR Credit Cards in 2026

Here are some of the strongest offers available right now. These aren’t affiliate placements — I’m just sharing what’s actually competitive based on current data.

Wells Fargo Reflect® Card

One of the longest 0% promo windows available right now. The Wells Fargo Reflect Card offers a 0% intro APR for 21 months from account opening on purchases and qualifying balance transfers, with a 17.49%, 23.99%, or 28.24% variable APR afterward. The balance transfer fee is 5% with a $5 minimum. No annual fee. Also comes with cell phone protection when you pay your bill with the card — a surprisingly nice bonus.

Best for: People who need maximum time to pay down debt or a large purchase.

Citi® Diamond Preferred® Card

The Citi® Diamond Preferred® Card comes with 0% intro APR for 21 months on Balance Transfers, plus 0% intro APR for 12 months on Purchases. After that, a 16.49% – 27.24% (Variable) APR applies. The balance transfer fee is 3% for the first 4 months (then 5%) — that lower introductory transfer fee can save you real money if you’re moving a large balance. No annual fee.

Best for: Balance transfer focus with one of the longest 0% BT windows on the market.

BankAmericard® Credit Card

The BankAmericard® credit card offers intro APRs of 0% for 21 billing cycles on purchases and balance transfers. The regular APR is 14.99%–25.99% Variable and the balance transfer fee is 5%. No annual fee, and notably, its ongoing APR floor is on the lower end compared to competitors.

Best for: People with excellent credit who want both a long promo period and a potentially lower long-term rate.

U.S. Bank Shield™ Visa® Card

The U.S. Bank Shield™ Visa® Card features 0% intro APR on purchases and eligible balance transfers for 21 billing cycles, followed by a variable APR of 16.99%–27.99%. Balance transfers must be completed within 60 days of account opening. Also earns 4% cash back on prepaid travel. No annual fee.

Best for: Those who want long 0% coverage plus some ongoing rewards value.

Chase Freedom Unlimited® / Chase Freedom Flex®

These are worth mentioning for people who want a 0% intro period and strong ongoing rewards. The intro APR period is typically shorter (around 15 months), but if you’re in the Chase ecosystem, you’ll find value in the Chase Freedom Flex®, which offers a generous introductory APR period on purchases and balance transfers, plus 5% cash back in rotating bonus categories.

Best for: Existing Chase customers who want dual functionality — debt payoff and long-term rewards earning.

Conclusion: Is a No Interest Credit Card Right for You?

Here’s my bottom line after years of covering this space: a 0% APR credit card is one of the most genuinely useful personal finance tools available to Americans — if you qualify, if you use it strategically, and if you respect the rules.

It’s not a way to get out of debt by doing nothing. It’s a way to buy yourself time — interest-free time — to pay down debt you’re already committed to eliminating. That distinction matters.

Actionable Takeaways

- Do the math first. Calculate your monthly payoff target before you apply. If the numbers don’t work, don’t get the card.

- Set up autopay immediately. Never miss a minimum payment. One slip can cost you the entire benefit.

- Complete your balance transfer quickly. Don’t let the window expire.

- Stop adding to the old high-interest card. Full stop.

- Build a payoff calendar. Mark 60 days before the promo ends on your calendar right now.

One Final Warning

These cards are designed by banks to be profitable. The 0% offer is the hook — what they’re hoping is that you either don’t pay it off in time (so they collect regular APR afterward) or that you stick around as a customer long-term. That’s fine. You can play the game in your favor. But you have to be intentional about it.

Used carelessly, a no interest credit card can make your debt situation worse. Used deliberately? It might just be the breathing room you need to actually get ahead.

Frequently Asked Questions (FAQ)

Q: Does a no interest credit card mean I’ll never pay interest? No. It means you won’t pay interest during the promotional intro period — typically 12 to 21 months. After that, the card’s regular APR applies to any remaining balance. Always know when your promotional period ends.

Q: Will applying for a 0% APR card hurt my credit score? Yes, slightly — applying triggers a hard inquiry, which can temporarily lower your score by a few points. Opening a new account also affects your average account age. These impacts are usually minor and short-lived, especially if you’re responsible with the new card.

Q: Can I transfer a balance from multiple cards to one 0% card? Yes, in most cases — up to the new card’s credit limit. You’ll pay a balance transfer fee on each transfer or on the total amount moved. Make sure the transfers are completed within the qualifying window (usually 60–120 days from account opening).

Q: What’s the difference between 0% APR and deferred interest? This is a critical distinction. True 0% APR means no interest accrues during the promo period. Deferred interest (common on store credit cards) means interest is accruing — it’s just waived if you pay the balance in full by the deadline. If you don’t, you owe all that backdated interest at once. Always confirm which one you’re dealing with.

Q: What credit score do I need to qualify for the best 0% APR cards? Most top 0% APR cards require a good to excellent credit score — generally 670 FICO or higher, with the best offers typically going to those with 720+. Check your score before applying to improve your approval odds.

Q: Is there a fee to take advantage of 0% on purchases (not a balance transfer)? No. You don’t have to pay a fee to take advantage of a 0% purchase APR. The fee only applies when you’re doing a balance transfer. New purchases on a 0% purchase APR card are free to carry — you just need to pay them off before the promo period ends.

Q: What happens if I only make minimum payments? You keep the 0% rate (as long as you pay on time), but you won’t pay off the balance before the promo period ends unless your minimum payment is very high. Always pay more than the minimum — ideally your calculated monthly payoff amount.

Q: Can I use a 0% APR card for a cash advance? Almost never. Cash advances on credit cards are typically excluded from 0% intro APR offers and carry their own separate (usually higher) rates and upfront fees. Avoid cash advances entirely.

Q: How many 0% APR cards can I have at once? Technically, you can apply for multiple. But each application creates a hard inquiry, and having several new accounts can impact your credit score. Most financial advisors suggest opening one at a time, using it strategically, and not stacking multiple balance transfers unless you really know what you’re doing.

Q: What should I do when the 0% period is about to end and I still have a balance? You have a few options: pay off the remaining balance in a lump sum if you can, call the issuer and ask if they’ll extend the promo rate (some will, especially if you’ve been a good customer), or look into doing another balance transfer to a new 0% card. That last option works — but it comes with another balance transfer fee and another hard inquiry on your credit, so weigh it carefully.

This article is for informational purposes only and should not be taken as personalized financial advice. Credit card terms change frequently — always verify current offers and rates directly with the card issuer before applying.