Let me be honest with you — a few years back, I had a $4,200 medical bill sitting on my regular credit card, quietly racking up 24% interest every single month. I kept telling myself I’d pay it off “soon.” Three months later, I’d paid almost $300 in interest and barely touched the principal. That’s when a friend who works in banking said, “Why aren’t you using a 0% intro APR card?” I didn’t even know that was a real thing. Not fully, anyway.

Table of Contents

If you’re in a similar spot — maybe it’s a home renovation you needed done yesterday, a medical expense that blindsided you, or a balance you moved from card to card trying to outrun the interest — this guide is for you. Specifically, I want to talk about the best no interest credit card for 18 months, how they actually work, and more importantly, how to not screw it up.

Because yes, you absolutely can use these cards the right way. But there are also a handful of ways people trip up, and I’ve seen enough of them (including my own mistakes) to know the warnings are worth taking seriously.

What Exactly Is a “No Interest” Credit Card?

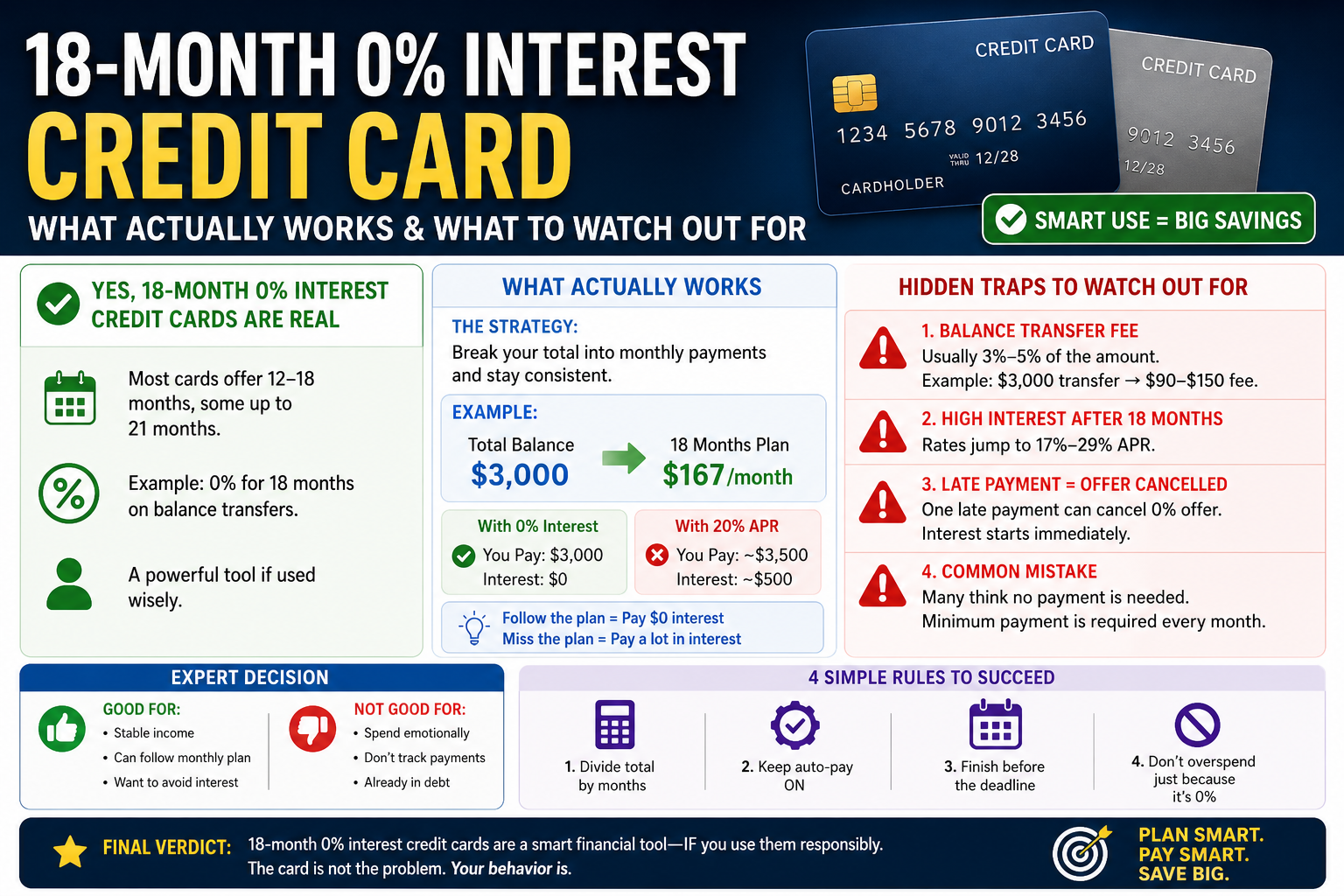

Let’s cut through the jargon first. When people say “no interest credit card,” they’re almost always talking about a card with a 0% introductory APR — either on new purchases, balance transfers, or both.

APR stands for Annual Percentage Rate. It’s the interest rate you pay on any balance you carry from month to month. Most regular credit cards charge somewhere between 18% and 29% APR right now. A 0% intro APR card temporarily pauses that interest — usually for anywhere from 12 to 21 months, depending on the card.

The sweet spot that most smart borrowers look for? 18 months. It’s long enough to meaningfully pay down a large balance or a big purchase without a rushed timeline. And in 2026, there are still some solid cards offering exactly that.

This isn’t some loophole or a trick. Banks offer these deals because they’re betting you won’t pay everything off in time — or that you’ll stay as a customer after the promo period ends. Some people do exactly that. Your job is to be the person who doesn’t.

How Does It Really Work?

Okay, this is where most people gloss over the details — and then get surprised later. Let me break it down properly.

Purchases vs. Balance Transfers

There are two main types of 0% APR offers:

1. 0% on New Purchases: You open the card, make purchases, and as long as you pay at least the minimum each month, no interest accrues on that balance during the promo period.

2. 0% on Balance Transfers: You transfer existing debt from a high-interest card to the new card. Now that debt sits at 0% instead of 22%. This is the move for people with existing credit card debt.

Some cards offer both — which is the most flexible option if you’re juggling new spending AND existing debt.

The Promotional Period

The promo period starts when your account is opened, not when you make your first purchase or transfer. So if you open the card and wait two weeks to use it, that’s two weeks gone. Move quickly once you’re approved.

What Happens After the 0% Period Ends?

This is the part people don’t want to hear. When the promotional period ends, your remaining balance doesn’t disappear — it starts accruing interest at the card’s regular APR, which is typically 19% to 29%. The interest doesn’t get backdated (that’s something called deferred interest, which is different and much worse — more on that in a second). But whatever you still owe will start getting interest charges immediately after the promo period ends.

This is why having an 18-month window matters. If you owe $5,400 and your promo period is 18 months, you need to pay $300/month to be free and clear. That’s a real number you can plan around.

Key Rules You Must Follow

I can’t stress this enough: missing a minimum payment can void your 0% APR offer entirely. Not reduce it. Void it. You could suddenly find yourself hit with the full 29% regular APR on your remaining balance, retroactively or from that point forward.

Here’s what you need to do without exception:

- Pay at least the minimum every single month. Set up autopay the day the card arrives. Don’t rely on yourself to remember.

- Don’t exceed your credit limit. Going over — even by $5 — can trigger penalty rates.

- Don’t miss the promo end date. Mark it in your calendar. Set a reminder 60 days out and again at 30 days.

- Understand whether it’s 0% APR or deferred interest. This distinction matters enormously. True 0% APR means if you pay off the balance in time, no interest ever. Deferred interest (common with store cards like those from furniture stores or electronics retailers) means if you have even $1 left unpaid at the promo end, they charge you interest on the original full balance going all the way back. Always confirm which one you’re getting.

Major bank credit cards — Citi, Chase, Amex, Wells Fargo, BofA — almost always use true 0% APR. Store financing cards? Read the fine print very carefully.

Balance Transfer Fees, Hidden Costs & Real Examples

Here’s the thing no one puts in the headline: most balance transfer cards charge a fee to move your balance over. Typically, it’s 3% to 5% of the amount transferred.

Let’s do real math:

You have $6,000 on a card charging 24% APR. You transfer it to a card offering 0% for 18 months with a 3% transfer fee.

- Transfer fee: $6,000 × 3% = $180 upfront

- Interest you’d pay staying on the old card for 18 months (if paying $333/month): roughly $1,300+

- Net savings: $1,100+

That’s not a bad trade. But if your balance is $800? The math changes. A $24 fee to save maybe $90 in interest — less compelling, but still worth it.

A few other hidden costs to watch:

- Annual fees: Some 0% APR cards charge annual fees. The better ones don’t. Always factor this in.

- Foreign transaction fees: If you travel internationally, watch out.

- Cash advance APR: Cash advances are almost never covered under the 0% offer. Using the card at an ATM starts charging interest immediately at a very high rate.

Pros and Cons (No Sugar-Coating)

The Pros

- You get breathing room. Real, financial breathing room. 18 months to pay down a balance without interest piling on top is genuinely useful.

- It’s cheaper than a personal loan in many cases — especially if the card has no annual fee and you pay it off in time.

- If used for purchases, it’s essentially an interest-free loan from a bank for 18 months.

- Can significantly help with large unexpected expenses: medical bills, car repairs, emergency home fixes.

The Cons

- You need decent credit to qualify. Most 0% APR cards require a 670+ credit score, and the best ones want 720+.

- The balance transfer fee is a real cost upfront.

- It can give you a false sense of financial security. I’ve seen people open a 0% APR card, transfer their balance over, feel relieved — and then run up the original card again. Now they have twice the debt.

- If you miss a payment or don’t pay off in time, the regular APR can be brutal.

- Opening a new card temporarily dips your credit score due to the hard inquiry and lower average account age.

Who Should Get One & Who Should Avoid It

Get One If:

- You have a specific, defined debt (medical bill, home improvement project, one-time expense) that you know you can pay off in 18 months with consistent monthly payments

- You’re being buried by high-interest credit card debt and want to consolidate into one manageable payment

- You’re planning a large but necessary purchase and want to spread payments interest-free

- You’re disciplined enough to not use the card for random extra spending after the transfer

Avoid It If:

- Your spending habits are the root problem. A 0% APR card won’t fix overspending — it just delays it

- You’re not sure you can make consistent monthly payments. The downside of missing payments here is severe

- Your credit score is below 650. You likely won’t qualify for the best offers, or you’ll get approved with a short promo period and a lower limit

- You’re tempted to keep spending on the old card once the balance is transferred. That’s how $6,000 of debt becomes $11,000

Best Practices & Smart Strategies to Maximize It

Here’s what actually works, based on watching a lot of people succeed and fail with these cards:

Calculate your monthly payment before you apply. Divide your total balance (plus transfer fee) by 17, not 18. Give yourself one month of buffer. If that number is more than you can realistically pay each month, this card isn’t the solution right now — it’s just kicking the can.

Automate the payment. Not the minimum — your calculated monthly payoff amount. Or at minimum, automate the minimum to protect your 0% offer, then manually pay extra when you can.

Freeze the old card. Not cancel — canceling hurts your credit score. But put it somewhere inconvenient. Some people literally freeze their credit card in a block of ice. Whatever keeps you from running it back up.

Track the promo end date obsessively. Put it in your phone calendar, your physical calendar, your email reminders. Six weeks before it ends, decide: do you have the remaining balance ready to pay? If not, what’s the plan?

Don’t open multiple cards at once. I’ve seen people think: “If one 0% APR card is good, three is better.” That’s a fast track to a wrecked credit score and unmanageable debt.

Current Popular 0% APR Cards Offering 18 Months in 2026

I want to be upfront: offers change, and you should always verify current terms directly with the issuer before applying. But here are some well-regarded options as of early 2026:

Wells Fargo Reflect® Card — Has consistently offered one of the longest 0% intro periods available, with up to 21 months possible (including the extension period) on purchases and qualifying balance transfers. No annual fee.

Citi Simplicity® Card — Known for no late fees, no penalty rate, and a competitive 0% intro APR period on balance transfers. A solid choice if you’re nervous about one-off late payments triggering consequences.

Chase Freedom Unlimited® — Solid 0% intro APR on purchases and balance transfers, plus cash back rewards. The rewards component makes it genuinely useful long-term, not just during the promo period.

Citi® Double Cash Card — Often offers 18 months on balance transfers, with 2% cash back (1% when you buy, 1% when you pay). One of the better combo cards for people who want to do a balance transfer AND have a useful everyday card afterward.

U.S. Bank Visa® Platinum Card — Known for long 0% intro periods and a simple, no-frills structure. Good for people who just want the tool without complexity.

Again — verify the current offer on each card’s official website before applying. What I’ve seen can shift by the time you’re reading this.

Conclusion + Actionable Takeaways + Warning

Look, a best no interest credit card for 18 months isn’t magic. It’s a tool. A genuinely useful one if you use it with intention, but a financial trap if you treat it like free money or a way to avoid confronting a spending problem.

If you’ve got a real number — a specific debt or planned expense — and you can commit to a realistic monthly payment that clears it in 17-18 months, this is one of the better financial tools available to everyday people. You’re essentially getting a short-term interest-free loan from a bank. That’s real value.

Here’s your quick action list:

- Add up exactly what you need to pay off or finance

- Divide that by 17 months and see if that monthly number is realistic

- Check your credit score before applying (use Credit Karma or your bank’s free tool — it doesn’t hurt your score)

- Compare 2-3 cards, looking at promo length, transfer fee, regular APR, and annual fee

- Apply for your top choice

- The day you’re approved: set up autopay, mark your promo end date, and put the old card away

- Don’t touch the available credit on the new card for new spending

One final warning: The moment you start missing months or adding new spending to the card, the math turns against you fast. These cards reward discipline. If the discipline isn’t there yet — work on that first. There’s no shame in it. Starting there is smarter than opening a card and making things worse.

You’ve got 18 months. Use them.

Frequently Asked Questions

What credit score do I need for the best no interest credit card for 18 months? Most top-tier 0% APR cards for 18 months require a credit score of at least 670 (Fair-Good range), but your best approval odds and highest credit limits come with a 720+ score. If you’re under 650, you may get approved for a shorter promo period or a lower limit than you need.

Does 0% APR mean I don’t have to make any payments? No — and this is a common mistake. You still need to make at least the minimum payment every single month. Skipping a payment doesn’t just cost you a late fee; it can immediately cancel your 0% promotional rate.

Is a balance transfer fee worth paying? In most cases, yes. A 3%-5% fee on a balance you’re currently paying 20%+ interest on is almost always a net win. Run the actual numbers for your situation — divide annual interest on your current card by 12, multiply by 18, and compare it to the transfer fee.

Can I use the card for new purchases AND do a balance transfer? It depends on the card. Some offer 0% on both; some only on one. Always check whether new purchases are included in the promo, or if using the card for spending could complicate your payoff plan.

What happens to my debt if I don’t pay it off before the 18 months end? Any remaining balance starts accruing interest at the card’s regular APR — which is typically between 19% and 29%. The interest isn’t backdated on a true 0% APR card (unlike deferred interest promotions). But it will start accumulating from that point forward on whatever you still owe.

Will applying for a 0% APR card hurt my credit score? Yes, slightly and temporarily. The hard inquiry from the application typically drops your score by 5-10 points. Opening a new account also lowers your average account age. Both effects generally recover within a year, and if you pay the balance down, your credit utilization improvement can offset the dip.

How many balance transfer cards can I apply for at once? Technically you can apply for multiple, but I’d strongly advise against it. Multiple hard inquiries in a short period hurts your score more, and juggling multiple cards with different promo end dates is a recipe for missing something important. Pick one card, commit to it.

Are there 0% APR cards with no balance transfer fee? They exist, but they’re rare and sometimes the tradeoff is a shorter promo period. The BankAmericard® Credit Card has historically offered competitive terms in this area. Worth checking, but don’t sacrifice 18 months of 0% just to avoid a 3% fee — the math rarely works in your favor.