Introduction

A 0% APR credit card sounds like free money. And in a way, it kind of is — if you use it correctly.

The problem is that most people don’t. They get approved, feel relieved, start spending or transferring balances, and then somewhere around month 14, they get hit with an interest charge they didn’t see coming. That’s not a rare edge case. It’s one of the most common ways these cards backfire.

If you’re thinking about opening one — whether to finance a large purchase or escape high-interest credit card debt — this guide breaks down exactly how to make the math work in your favor, what to watch out for, and when walking away is actually the smarter move.

Table of Contents

The Short Answer

A 0% APR card gives you a promotional period (usually 12–21 months) during which you pay no interest on purchases, balance transfers, or both. After that window closes, the standard APR kicks in — often somewhere between 20% and 30%.

The strategy is simple: borrow money interest-free, pay it all off before the promo ends. But executing that strategy takes discipline and a few key habits most people skip.

0% APR Card vs. Regular Credit Card

| Feature | 0% APR Card | Regular Credit Card |

|---|---|---|

| Intro interest rate | 0% | Standard APR applies immediately |

| Promo period | 12–21 months | None |

| Post-promo APR | 20–30%+ | 20–30%+ |

| Transfer fee | 3–5% typical | May apply |

| Best use case | Debt payoff, big purchases | Everyday spending with rewards |

What Is a 0% APR Credit Card?

A 0% APR credit card temporarily charges zero interest on balances — for a set number of months after you open the account.

There are two main types:

Intro APR on purchases: You make new purchases and carry a balance without being charged interest during the promotional window. This is useful if you need to finance something — a medical bill, home repair, appliance — without going into high-interest debt.

Intro APR on balance transfers: You move existing credit card debt onto the new card and pay it down without accruing interest. This is one of the most practical debt reduction tools available, assuming you qualify and use it strategically.

Some cards offer both. Some offer only one.

Here’s what beginners often miss: “0% APR” is not the same as “0% interest forever.” The moment your promotional period ends, your remaining balance starts accruing interest at whatever the card’s ongoing APR is. That rate can be painful — sometimes above 25%.

How to Use a 0% APR Card Wisely

This is where most advice gets too vague. Let’s get specific.

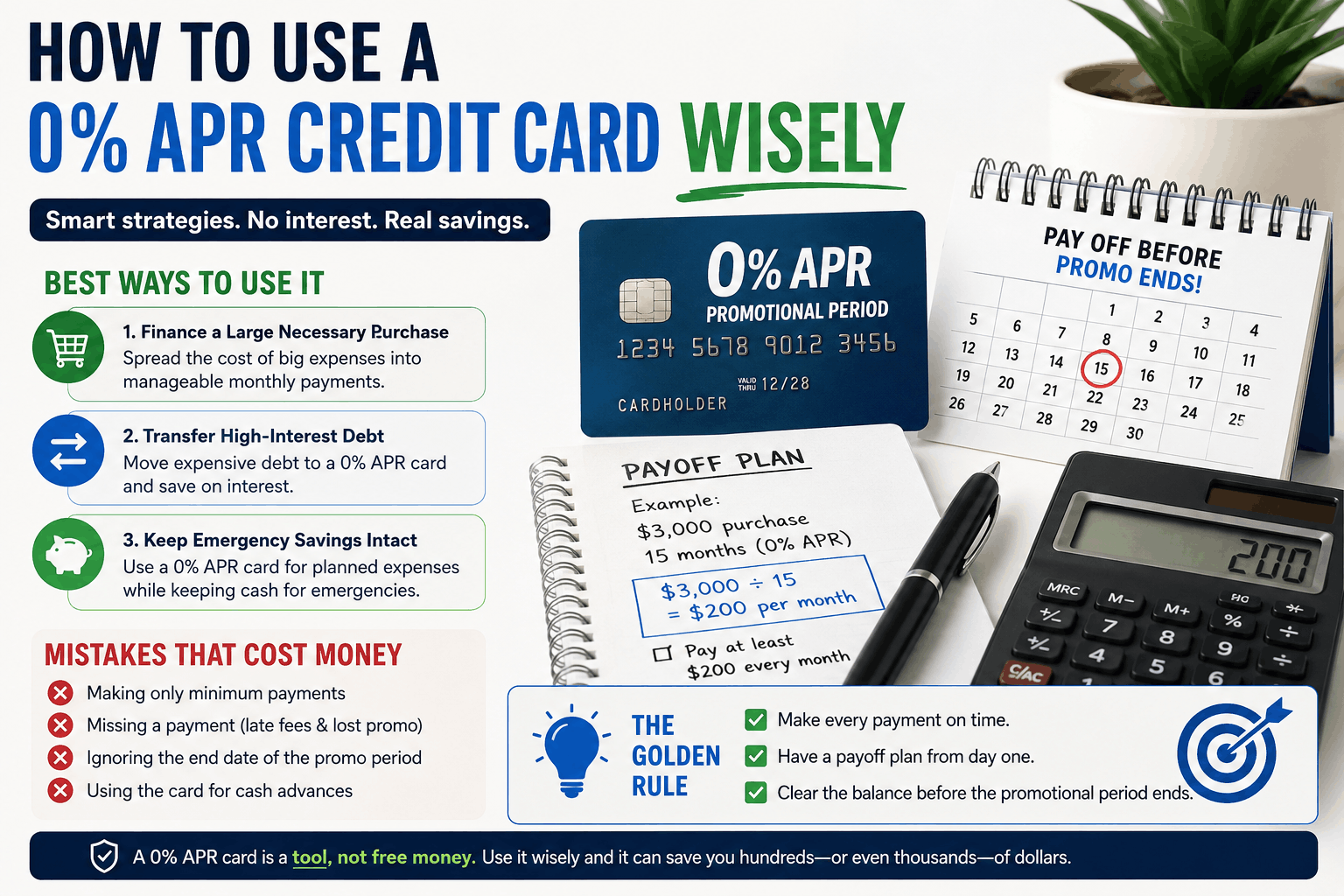

1. Know Your Payoff Number Before You Spend

Before you swipe the card once, do this math:

Take your total planned balance and divide it by the number of months in your promo period. That’s your required monthly payment to avoid any interest at all.

Example: $3,600 balance ÷ 18-month promo = $200/month.

Not $200 minimum payment as listed on your statement. $200 toward your actual balance, every month, without exception.

If that number doesn’t fit your current budget, the card won’t work the way you’re hoping. That’s not a failure — that’s just math telling you to find a longer promo period or reduce the balance you’re carrying.

2. Set Up Autopay — But Not Just for the Minimum

Autopay protects your credit score and keeps you from missing payments. But most people set it for the minimum payment and call it done.

That’s fine for avoiding late fees. It won’t get your balance to zero by the promo end date. You need to automate your calculated monthly payoff amount — the number you found above.

Some issuers let you set a custom autopay dollar amount. Others only offer minimum, full statement balance, or fixed amounts. If yours doesn’t let you set it precisely, create a recurring calendar reminder instead.

3. Don’t Mix Spending With Your Payoff Balance

This is a trap a lot of people fall into after a balance transfer.

You move $4,000 of credit card debt to your new 0% card. Great start. Then you use the same card for groceries, gas, everyday spending. Now you have new purchases mixing with your transfer balance.

Here’s the issue: payments often get applied to the lowest-APR portion first. If any part of your balance isn’t under a promotional rate, your new purchases might sit there accruing interest while you’re focused on the transfer. Read the fine print on how your issuer applies payments.

The cleanest strategy: keep your 0% card strictly for the balance you’re working to eliminate. Use a separate card for daily spending.

4. Track the Promo End Date Like a Bill Due Date

Put it on your phone. Set a calendar alert 60 days before it expires.

The promo end date is the most important date associated with this card. Your statement won’t warn you loudly. The bank isn’t going to send a reminder. That date passes quietly, interest starts immediately — and suddenly you’re back in the same situation you were trying to escape.

Real-World Cost Examples

Example 1: Financing a $2,400 Home Appliance

You buy a $2,400 refrigerator on a card with a 15-month 0% intro APR.

Monthly payment needed to clear it: $160/month.

If you pay it off within 15 months: $0 interest. You borrowed $2,400, you paid back $2,400.

If you still have $600 remaining when the promo ends: That $600 starts accruing interest at 27% APR. After several months of minimum payments, you’ve paid far more than the original balance warranted. The fridge was free. The procrastination wasn’t.

Example 2: Balance Transfer From a High-APR Card

You have $5,000 on a card charging 24% APR.

Without a balance transfer, paying $200/month:

- Time to pay off: ~32 months

- Total interest paid: roughly $1,300+

With a balance transfer to an 18-month 0% card (3% fee):

- Transfer fee: $150

- Monthly payment needed to clear it: ~$278

- Total interest paid: $0 (just the $150 fee)

The math strongly favors the transfer — but only if you commit to the higher monthly payment consistently.

Hidden Fees and Traps

Balance Transfer Fees

Almost every 0% balance transfer card charges a transfer fee — typically 3% to 5% of the amount you move. On a $5,000 transfer, that’s $150 to $250 upfront.

That fee is worth paying if you’re escaping a high-interest card. It’s not worth it if you’re moving a small balance you could pay off in two or three months anyway.

Deferred Interest vs. True 0% APR

This one catches people off guard more than anything else on this list.

A true 0% APR card charges zero interest during the promo period. If you have $300 left when it ends, only that $300 starts accruing interest going forward.

A deferred interest card — common with store credit cards from furniture retailers, electronics chains, and medical financing programs — works very differently. If you don’t pay the full balance by the promo end date, you get charged interest retroactively, on the entire original balance, from day one. All of it. At once.

That’s not a typo. That’s how deferred interest works, and it’s buried in the fine print. Always verify which type you’re dealing with before signing anything.

Penalty APR

Miss a payment — even by a day — and your 0% promotional rate may disappear entirely. Many issuers will apply a penalty APR that can reach 29.99% or higher, applied to your entire balance immediately.

Look for this specifically in your cardholder agreement before you apply. Don’t assume it won’t affect you.

New Purchase APR vs. Transfer APR

Some cards offer 0% only on balance transfers, not on new purchases. Others cover purchases but not transfers. A few cover both. Assuming your card handles everything without checking is a common and expensive mistake.

Common Mistakes People Make

Paying only the minimum. The minimum payment keeps the account in good standing, but it’s designed to keep you in debt longer — not to help you pay it off. Without a calculated monthly target, most balances won’t clear before the promo expires.

Opening the card without a written plan. Getting approved feels like the hard part. Actually committing to a monthly number and following through is where most people slip. Without a specific target, good intentions drift.

Assuming the promo period resets or extends. It doesn’t. Occasionally an issuer might extend it as a goodwill gesture if you call, but that’s not a strategy. Treat your end date as fixed.

Closing the card immediately after payoff. Once you’ve paid everything off, closing the card reduces your available credit and can raise your utilization ratio, which may lower your credit score. Many people keep the card open with a zero balance. If the card has an annual fee, recalculate whether that makes sense.

Applying for multiple cards at once. Each application triggers a hard inquiry on your credit report. If you’re pursuing a balance transfer strategy, pick one well-researched card and apply for that one. Not three, hoping one sticks.

Who Should Avoid 0% APR Cards?

Not everyone should use one. Here’s when it genuinely doesn’t make sense:

If you can’t realistically pay off the balance before the promo ends. If the monthly payment math doesn’t work with your budget, you’ll end up paying high interest anyway — plus a transfer fee you’ve already paid with nothing to show for it.

If available credit tends to become a spending trigger. Having a card with a generous limit and no interest can feel like permission to spend. If that’s been a pattern before, this tool can make things worse.

If your credit score isn’t strong enough for a competitive offer. Many of the best 0% cards require good to excellent credit — typically 670 or above on most models. If you get approved for a shorter promo window, higher post-promo APR, or steep transfer fee, the benefit shrinks considerably. Check your credit before applying.

If the balance you’re carrying is small. For a $400 balance you could clear in three months, the hard inquiry and application process probably aren’t worth it.

How to Choose the Right Card

What to Compare

| Factor | What to Look For |

|---|---|

| Promo period length | 15–21 months preferred |

| Transfer fee | 3% is standard; 0% promos exist |

| Post-promo APR | Lower is better; you may not fully pay off |

| Annual fee | $0 is ideal for this strategy |

| Penalty APR policy | Read before applying |

Questions to Ask Yourself First

- What’s the exact balance I’m planning to transfer or finance?

- Can I realistically pay it off within the promo window at a monthly amount I can sustain?

- Do I need the 0% to apply to purchases, balance transfers, or both?

- Does this card charge an annual fee that reduces my actual savings?

- What happens to my promo rate if I miss a payment?

There’s no single best card. Someone managing $8,000 in debt needs a longer promo period. Someone financing a $1,200 purchase needs minimal fees. Match the card to your specific numbers, not to a general “best of” ranking.

Frequently Asked Questions

Does applying for a 0% APR card hurt my credit score? Yes, temporarily. The hard inquiry typically drops your score a few points. If you use the card responsibly — on-time payments, keeping utilization low — your score can recover within a few months and potentially improve.

What happens to my remaining balance when the promo period ends? It starts accruing interest at the card’s regular APR — often in the 20–30% range. You’re not charged retroactively on what you already paid off, only on what remains.

Can I transfer a personal loan balance to a 0% APR card? Most issuers only accept other credit card balances for transfers. Personal loan transfers aren’t standard, though a small number of cards allow it. Confirm with the issuer before applying with that expectation.

Is a 0% APR card the same as Buy Now Pay Later? Not quite. BNPL services like Affirm or Klarna are tied to specific purchases and operate outside the credit card system. A 0% APR credit card gives broader flexibility, works with your existing spending, and usually has a longer interest-free window. Both can be useful for different purposes.

Can I transfer a balance from another card issued by the same bank? Generally, no. Most issuers don’t allow transfers between their own cards. You typically need to move debt from a card issued by a different financial institution.

Do cash advances qualify for the 0% promotional rate? Almost never. Cash advances usually begin accruing interest immediately — often at a higher rate than regular purchases — regardless of any promotional APR. Avoid using a 0% card for cash advances entirely.

Final Thoughts

A 0% APR credit card is one of the few legitimate tools that lets you borrow money at no cost — if you operate within its terms.

The terms aren’t complicated. Know your monthly payoff number. Automate your payments to hit that number. Track your promo end date. Don’t muddy the balance with unrelated spending. Understand whether you’re dealing with true 0% APR or deferred interest before you sign up.

Where people go wrong isn’t usually a lack of understanding — it’s treating the card as emotional relief rather than a structured plan. The promo period feels long at the start. It moves faster than you expect.

Go in with a specific number, a realistic monthly payment, and an alert set 60 days before expiration. That alone puts you in better shape than most people who hold these cards. It’s not complicated. It just requires follow-through.

Done right, this strategy can save you hundreds or even thousands in interest. Done carelessly, it just relocates your debt without fixing anything.