If you’ve ever stared at a credit card statement and noticed your balance barely moved despite paying on time every month, you already understand the problem. Most of that payment isn’t touching what you actually owe — it’s covering interest. At today’s average rate of roughly 21.5% on cards carrying a balance, a chunk of every dollar you send in just evaporates.

That’s why so many people search for 0% APR options. A 0% intro period, used correctly, can redirect that wasted interest money straight toward your actual debt. Used carelessly, it can also leave you with a bigger balance and a worse credit profile than when you started. This guide walks through how the strategy actually works, where people get tripped up, and how to figure out if it fits your situation.

Table of Contents

Quick Answer

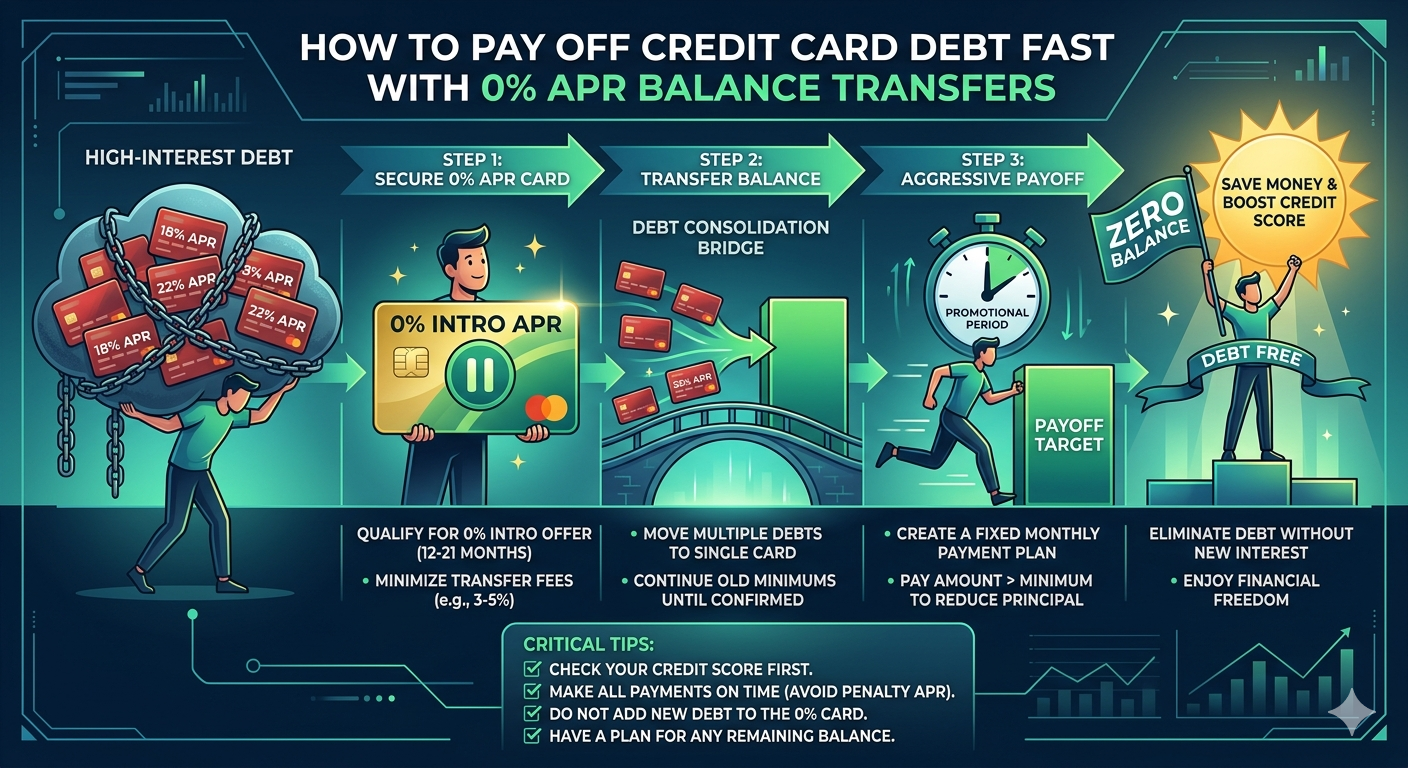

The short version: a 0% APR balance transfer card lets you move existing credit card debt onto a new card that charges no interest for a set introductory window — usually 12 to 21 months. You pay a one-time transfer fee (typically 3% to 5% of the amount moved), then aim every spare dollar at the balance before the promotional rate expires and reverts to the card’s regular APR, often in the high teens to high twenties.

It’s not the only option. Here’s how the main routes compare at a glance:

| Option | Typical 0% Window | Typical Cost |

|---|---|---|

| Balance transfer card | 12–21 months | 3%–5% transfer fee |

| 0% intro APR card (new purchases) | 12–21 months | Usually no transfer fee, but no transfer either |

| Debt consolidation loan | None (fixed rate instead) | Origination fee, 7%–25% APR |

| Nonprofit debt management plan | None (reduced rate instead) | Small monthly fee, often $0–$50 |

There’s no single “best” answer here — it depends on your balance, your credit, and how disciplined you can be once the temptation to keep spending shows up.

What Is a 0% APR Balance Transfer, Really?

APR stands for annual percentage rate — it’s the cost of carrying a balance, expressed as a yearly percentage. A 0% intro APR simply means the card issuer agrees not to charge interest on that balance for a limited stretch of time, usually as a way to win your business.

Here’s the part that confuses a lot of beginners: 0% APR doesn’t erase what you owe. If you move $4,000 in credit card debt onto a 0% APR card, you still owe $4,000 (plus the transfer fee). What changes is that none of your monthly payment goes toward interest during the promo period — all of it chips away at the principal instead.

Compare that to a card sitting at 22% APR. On that same $4,000, you’d be paying roughly $73 a month in interest alone before your payment even starts reducing what you owe. Over a year, that’s close to $900 spent just to keep the debt where it is. A 0% card removes that drag entirely, for as long as the promotion lasts.

The catch is the phrase “for as long as the promotion lasts.” When the intro period ends, the remaining balance starts accruing interest at the card’s standard rate — often 17% to 28%, depending on creditworthiness. That’s the entire game: pay it down (or off) before the clock runs out.

Best Options for Tackling the Debt

1. Balance Transfer Card

Best for: People with existing high-interest credit card debt and decent-to-good credit who can realistically pay it off within the promo window.

Advantages: No interest accrual during the intro period, which can save hundreds or thousands of dollars depending on the balance. Many cards offer 18–21 months on transfers, which is a long runway if you budget for it.

Downsides: The transfer fee is charged upfront, regardless of how quickly you pay off the balance. There’s also a credit limit cap — you usually can’t transfer more than the card’s approved limit, so a very large balance might not fit on one card.

Hidden risks: Most issuers won’t let you transfer a balance from another card issued by the same bank. So if your debt is on a Chase card, a Chase balance transfer card generally won’t work for that specific balance.

Important warning: Miss a payment — even by a few days — and many issuers reserve the right to cancel the 0% rate entirely, sometimes retroactively to a penalty APR around 29%.

Who should avoid it: Anyone who isn’t confident they can avoid using the old card again. Carrying a near-zero balance on the original card while a fresh balance builds on the new one is one of the most common ways this strategy backfires.

2. 0% Intro APR Card for New Purchases

Best for: Someone who needs to make a large near-term purchase (medical bill, car repair, appliance) interest-free, rather than someone moving existing debt.

Advantages: No transfer fee since there’s no transfer involved — you’re simply not charged interest on new spending for the promo window.

Downsides: This doesn’t help pay off debt that already exists elsewhere; it just prevents new debt from accruing interest temporarily.

Hidden risks: A 0% intro APR is not the same thing as a “deferred interest” promotion, which many store and retail cards use instead. With deferred interest, if you don’t pay the entire balance off by the deadline, you’re charged interest retroactively on the original amount — back to day one. Read the terms carefully; the difference between these two structures can cost hundreds of dollars.

Who should avoid it: Anyone tempted to treat the 0% window as extra spending power rather than a repayment tool.

3. Debt Consolidation Loan

Best for: People with larger balances (often $7,000+) spread across multiple cards, or anyone who knows they’ll struggle with the discipline a revolving 0% card requires.

Advantages: A fixed interest rate and fixed monthly payment mean the loan amortizes on a set schedule — there’s no temptation to revert to minimum payments, and no promo period that suddenly expires. Rates currently run anywhere from around 7% for excellent credit up into the low-to-mid 20s for fair credit, according to typical lender ranges reported by major personal finance trackers.

Downsides: Unlike a 0% card, you’re paying interest from day one, just at a lower, fixed rate than your credit cards.

Hidden risks: Origination fees (often 1%–8% of the loan) get deducted from the amount you receive, so you may need to borrow slightly more than your actual debt to cover it.

Who should avoid it: Anyone who doesn’t have the credit profile to qualify for a rate meaningfully lower than what they’re already paying — at that point, the loan isn’t actually saving money.

4. Nonprofit Debt Management Plan (DMP)

Best for: People with significant debt, lower credit scores that won’t qualify for 0% offers, or anyone feeling overwhelmed by multiple accounts and due dates.

Advantages: A certified credit counselor (often through agencies affiliated with the National Foundation for Credit Counseling) negotiates reduced interest rates directly with your creditors — sometimes down to single digits — and consolidates payments into one monthly amount.

Downsides: Most plans require closing the enrolled credit cards, which can temporarily affect your credit utilization and average account age.

Hidden risks: Not every “debt relief” company offering this service is reputable. The Consumer Financial Protection Bureau has issued repeated warnings about debt settlement companies that charge large upfront fees and advise people to stop paying creditors entirely — a very different (and riskier) approach than a nonprofit DMP.

Who should avoid it: People who can already qualify for a 0% balance transfer with a manageable repayment timeline; a DMP makes more sense once that math stops working.

Internal link suggestion: link to a dedicated article comparing debt management plans vs. debt settlement here.

Real-World Cost Examples

Numbers make this easier to picture than percentages alone. Take a $5,000 balance at a 22% APR — close to today’s national average.

Paying it off in 18 months without transferring: you’d need to pay about $329 a month, and roughly $917 of your total payments would go toward interest.

Transferring that same $5,000 to a 0% APR card with a 3% fee: the fee adds $150 to your balance, bringing it to $5,150. Spread over 18 months, that’s about $286 a month — lower than the non-transfer payment — and your total cost is just the $150 fee instead of $917 in interest.

That’s a difference of roughly $767, plus a lower monthly payment, simply by moving the same debt onto a card that doesn’t charge interest during the payoff window.

| Scenario | Monthly Payment | Total Extra Cost |

|---|---|---|

| Stay at 22% APR, pay off in 18 mo. | ~$329 | ~$917 (interest) |

| 0% APR card, 3% fee, pay off in 18 mo. | ~$286 | ~$150 (fee) |

The math only works this cleanly, though, if the balance actually gets paid off inside the promo window. If that same $5,150 is still sitting there when the 0% period ends and the rate jumps to 24%, the remaining balance starts costing real money again — fast.

Hidden Fees and Traps

A lot of people don’t realize how many small details determine whether this strategy actually saves money:

- Balance transfer fee: Almost always 3%–5% of the transferred amount, charged immediately, whether you pay off the balance in two months or twenty.

- Deferred interest vs. true 0% APR: As mentioned above, deferred interest promotions can charge interest retroactively from the original purchase date if the balance isn’t paid in full by the deadline. True intro APR cards only charge interest going forward from the date the promo ends.

- Losing the promo rate: A single late payment can trigger an immediate switch to the penalty APR, sometimes as high as 29.99%, under terms most issuers are legally permitted to apply.

- Transfer limits: You typically can’t transfer more than your approved credit limit on the new card — and limits for new cardholders are often modest, especially for thinner credit files.

- Same-bank restrictions: Issuers generally won’t let you transfer a balance between two cards from their own bank.

- The minimum payment trap: Federal law (the CARD Act of 2009) requires every statement to show how long it would take to pay off your balance using only minimum payments — and the number is often shocking, frequently well over a decade for a moderate balance.

Common Mistakes

This catches borrowers off guard more than almost anything else: transferring the balance, then continuing to use the original card “just a little.” The old balance doesn’t disappear, and now there’s a second one building too.

Other recurring mistakes:

- Not running the math on transfer fee vs. interest saved before applying

- Choosing a card based on rewards rather than the length of the 0% window

- Closing the old card immediately after transferring, which can shorten your average account age and spike your credit utilization ratio

- Treating the 0% period as “no rush” instead of building a fixed monthly payoff plan from day one

- Applying for several balance transfer cards at once, each triggering a hard inquiry that can dip your score with Experian, Equifax, and TransUnion

Who Should Avoid This?

A 0% APR strategy isn’t the right fit for everyone, and there’s no shame in that.

- If your monthly budget genuinely can’t cover paying off the balance before the promo ends, you’re just postponing the same problem with an added fee on top.

- If your credit score sits below the high 600s, you likely won’t qualify for the longest, lowest-fee 0% offers — applying anyway just adds a hard inquiry with little payoff.

- If you’ve struggled in the past to stop using a card once it’s been “cleared,” a fixed-payment debt consolidation loan or a nonprofit DMP may protect you better than another revolving credit line.

How to Choose the Right Option

A simple gut check: take your total debt, divide it by the number of months in the longest 0% offer you can realistically qualify for, and see if that monthly payment fits your actual budget — not your best-case-scenario budget.

If the number works comfortably, a balance transfer card is usually the lowest-cost path. If the number is tight or your credit isn’t strong enough for a long promo period, a debt consolidation loan trades a 0% rate for the security of a fixed schedule with no expiration date. If the debt feels unmanageable on either path, a conversation with a nonprofit credit counselor costs nothing and can clarify which route actually makes sense for your numbers.

Internal link suggestion: link to an article on calculating credit utilization ratio here.

Frequently Asked Questions

Does a balance transfer hurt my credit score? There’s usually a small, temporary dip from the hard inquiry when you apply, and possibly from a new account lowering your average account age. Over time, paying down the balance typically improves your score by reducing your credit utilization ratio.

How long does 0% APR usually last? Most balance transfer offers run 12 to 21 months, with the longest offers generally going to applicants with strong credit.

Can I transfer a balance to a card from the same bank? Usually not. Most issuers only allow balance transfers from other banks’ cards.

What happens if I don’t pay off the balance before the 0% period ends? Any remaining balance starts accruing interest at the card’s standard ongoing APR, which is often significantly higher than the rate on your original card.

Is a balance transfer better than a personal loan? It depends on your discipline and credit. A balance transfer is usually cheaper if you can pay it off within the promo window. A personal loan offers a fixed payment with no expiring rate, which can be safer for larger balances or less predictable budgets.

Do I need good credit to qualify for 0% APR offers? Generally yes — the longest, lowest-fee offers tend to require a credit score in the high 600s or above. Fair-credit borrowers can sometimes qualify for shorter promo periods.

Final Thoughts

A 0% APR balance transfer isn’t a shortcut, and it isn’t free — there’s a fee attached, and a deadline that matters more than people expect going in. What it offers is a temporary pause on interest charges, which can be genuinely useful if you have a realistic plan to pay down the balance during that window.

The math looks better than it feels in real life when the old habits that built the debt are still in the picture. Before applying, it helps to have an honest answer to one question: can this balance actually be paid off before the promo ends, on the budget you actually have? If yes, this is one of the more effective tools available. If not, a fixed-rate loan or a nonprofit debt management plan may serve you better.

This article is general information, not personalized financial advice. For a plan tailored to your specific debts and budget, a fee-only financial advisor or a certified nonprofit credit counselor can take a closer look at your full picture.