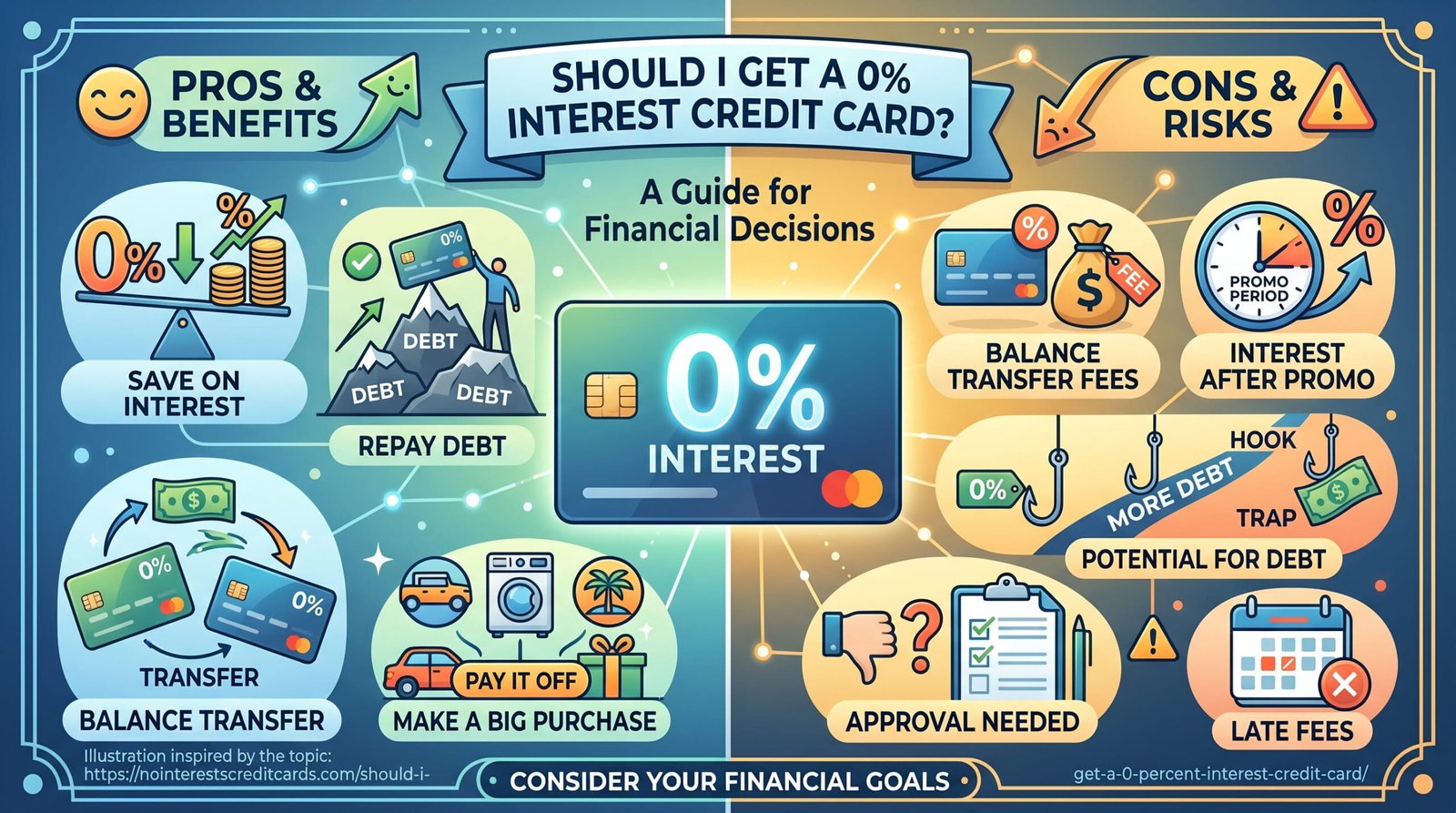

You’re staring at a credit card offer promising “0% APR for 18 months” and trying to figure out if it’s a smart move or a trap with good marketing. That hesitation is fair. A 0% card can save you real money — or it can quietly turn into one more balance you’re stuck juggling once the promotional clock runs out.

People usually land on this question for one of two reasons: they’re carrying credit card debt at a painful interest rate and want relief, or they have a big purchase coming up (a move, a medical bill, a car repair) and don’t want to pay interest while they spread out the cost. Both are valid reasons. The card itself isn’t good or bad — what matters is whether your spending habits and your payoff timeline actually match what the offer requires.

This guide breaks down how 0% interest cards really work, where people get burned, and how to tell if one makes sense for your situation.

Table of Contents

Quick Answer

A 0% interest credit card is worth getting if you can realistically pay off the balance before the promotional period ends and you’re disciplined enough not to treat the interest-free window as extra spending money. It’s usually a bad idea if you’re already stretched thin, tend to carry balances long-term, or you’re not sure you’ll remember the exact end date.

| If this describes you… | A 0% card is probably… |

|---|---|

| You have a clear payoff plan and stable income | A good fit |

| You’re consolidating high-interest debt and can pay it down in the promo window | Often worth it |

| You’re not sure you can pay it off before the promo ends | Risky |

| You tend to spend more when you feel “interest-free” | Probably not a good idea |

| Your credit score is below the high-600s | May not qualify for the best offers |

What Is a 0% Interest Credit Card?

A 0% interest credit card (also called a 0% intro APR card) charges no interest on certain balances for a set promotional period — typically somewhere between 12 and 21 months, depending on the issuer and your credit profile. After that window closes, the rate jumps to the card’s standard APR, which right now averages somewhere in the low-to-mid 20% range for most issuers, according to Federal Reserve data tracked through LendingTree.

There are two main flavors, and the difference trips people up constantly:

- 0% purchase APR — new purchases you make on the card don’t accrue interest during the promo period.

- 0% balance transfer APR — you move an existing balance from a different (higher-interest) card onto this one, and that transferred balance doesn’t accrue interest during the promo period.

Some cards offer both. Some only offer one. They are not interchangeable, and a card advertising “0% on balance transfers” usually still charges normal interest on new purchases, or vice versa. Read the actual terms, not just the headline.

A simple example: Say you put a $2,000 emergency car repair on a 0% purchase APR card with an 18-month promo. If you pay it off in equal installments over those 18 months, you pay zero interest — full stop. The same $2,000 on a card with a 22% APR, paid off over the same period, would cost you roughly $350–$400 in interest. That gap is the entire appeal of these cards.

Best Options: Comparing the Main Types

Rather than chasing a specific “best card” (offers change constantly and the right one depends on your credit profile), it’s more useful to understand the categories you’re choosing between.

1. 0% Purchase APR Cards

Best for: Financing a large planned purchase — furniture, a laptop, medical bills, home repairs.

Advantages:

- No interest on new spending during the promo window

- Often paired with rewards or cash back, depending on the card

- Builds payment history if used responsibly

Downsides:

- The promo rate usually only applies to purchases made early on, not ones added later in the cycle — check the fine print

- Once the intro period ends, any remaining balance starts accruing interest at the full rate immediately

Hidden risks: Some retail and store cards use deferred interest instead of true 0% APR. With deferred interest, if you haven’t paid the entire balance off by the deadline, you get charged interest retroactively on the full original amount — not just the leftover balance. This is one of the most misunderstood terms in consumer credit, and it catches people off guard every year. Always check whether the offer says “0% APR” or “no interest if paid in full by [date].” Those are legally different products.

Who should avoid it: Anyone who isn’t confident they can pay off the purchase before the promo ends, especially on a deferred-interest store card.

2. 0% Balance Transfer Cards

Best for: Consolidating existing high-interest credit card debt onto one lower-cost card.

Advantages:

- Can meaningfully speed up debt payoff by eliminating interest temporarily

- Simplifies multiple balances into a single payment

- Some cards offer 0% for 15–21 months on transfers

Downsides:

- Balance transfer fees typically run 3% to 5% of the transferred amount, charged upfront. On a $6,000 transfer, that’s $180–$300 added to your balance before you’ve paid anything down.

- You usually need good to excellent credit to qualify for the longest 0% windows

- If you keep spending on the old card after transferring the balance, you can end up with two balances instead of one — this is one of the most common ways people make their debt situation worse, not better

Hidden risks: The transfer fee is added to your balance immediately, so your starting number is actually higher than what you transferred. Also, most issuers won’t let you transfer a balance from another card issued by the same bank.

Who should avoid it: Anyone planning to keep charging on the old card without a plan to pay it down, or anyone whose monthly budget can’t realistically clear the new balance before the promo ends.

3. Credit Union or Community Bank Low-Rate Cards

Best for: People who don’t qualify for a 0% promo but still want to lower borrowing costs.

Advantages:

- Often lower ongoing APRs even without a promotional rate, since credit unions are typically not-for-profit

- More flexible underwriting for members with fair credit

- Fewer aggressive fee structures in general

Downsides:

- Requires membership, which sometimes means meeting eligibility criteria

- Rewards programs are usually thinner than big-bank cards

Who should avoid it: Anyone who specifically needs a true 0% rate for a large purchase — credit unions rarely offer intro periods as long as major issuers.

4. Alternatives Worth Comparing: Personal Loans and Nonprofit Debt Management Plans

Best for: People with debt too large to clear within a typical 12–21 month promo window, or people who don’t qualify for 0% offers.

Advantages:

- Fixed monthly payments and a fixed payoff date, which removes the “did I pay it off in time” risk entirely

- Personal loan rates, while not 0%, are often well below standard credit card APRs for borrowers with decent credit

- Nonprofit credit counseling agencies (look for ones accredited by the National Foundation for Credit Counseling) can sometimes negotiate reduced rates through a structured debt management plan

Downsides:

- Personal loans usually carry an origination fee

- Debt management plans may require closing existing credit cards, which can temporarily affect your credit mix

Who should avoid it: Honestly, this path makes sense for more people than they assume — if you’ve tried the credit-card-juggling approach before and it didn’t work, a fixed-payment option removes a lot of the guesswork.

Real-World Cost Examples

These are illustrative, not guarantees — actual costs depend on your card’s specific terms.

Example 1: Balance transfer that works out

- $6,000 balance moved to a card with 0% APR for 18 months and a 3% transfer fee ($180)

- New starting balance: $6,180

- Monthly payment needed to clear it before the promo ends: about $343/month

- Total interest paid: $0 (only the $180 fee)

- Compare that to leaving the $6,000 on a 22% APR card and paying it off over 18 months: roughly $1,150 in interest

Example 2: Promo period missed

- Same $6,000 balance, but the cardholder only pays $200/month and doesn’t clear it before the 18-month mark

- Remaining balance (~$2,400) starts accruing interest at the card’s standard rate, which can land anywhere from 18% to 28%+ depending on the issuer

- The “free” debt consolidation suddenly isn’t free anymore — and now there’s a new account on the credit report with the original high balance to explain

The math looks great on paper. Whether it works in real life comes down to whether the monthly payment is actually built into your budget, not just a hope.

Hidden Fees and Traps

| Trap | What to watch for |

|---|---|

| Balance transfer fee | Usually 3–5%, added to your balance immediately |

| Deferred interest | Retroactive interest on the entire original balance if not paid in full by the deadline — common on store cards |

| Promo-ending penalty | Some cards revoke the 0% rate early if you’re late on a single payment |

| Cash advances | Almost never covered by 0% offers, and they start accruing interest (often at a higher rate) immediately, with no grace period |

| Standard APR after promo | Can be 20–28%+ depending on your credit — know this number before you apply, not after |

| New hard inquiry | Applying for a new card typically triggers a hard inquiry, which can briefly ding your credit score |

The Consumer Financial Protection Bureau has flagged deferred-interest promotions specifically as a category consumers misunderstand often, since the terms can sound identical to true 0% APR offers in the marketing materials even though the financial consequences are very different.

Common Mistakes People Make

- Treating the 0% period like free money. Spending more because “it’s not accruing interest” defeats the purpose entirely.

- Not calculating the real monthly payment needed. Knowing the promo length isn’t enough — divide the balance by the number of months and treat that as a fixed bill.

- Missing a single payment. Many issuers reserve the right to end the promotional rate early if you pay late, even once.

- Keeping the old card balance growing after a transfer. This is the single most common way a debt consolidation plan backfires.

- Confusing 0% APR with deferred interest. These look the same in an ad and behave very differently if you miss the deadline.

- Forgetting the exact end date. Set a calendar reminder. Issuers are not required to send a dramatic warning before the rate jumps.

Who Should Avoid This?

Be honest with yourself about a few things before applying:

- If your monthly budget is already tight and you can’t pencil in a fixed payment large enough to clear the balance in time, a 0% card just delays the interest rather than avoiding it.

- If your credit score is in fair territory (roughly 580–669 on the common FICO scale), you may not qualify for the longest or most generous 0% offers, and applying anyway results in a hard inquiry for an offer you might not get.

- If you have a pattern of carrying balances for years rather than months, a fixed-payment personal loan or a nonprofit debt management plan may serve you better than another credit card, even an interest-free one.

- If you’re planning to apply for a mortgage or auto loan in the next several months, opening a new credit card can temporarily affect your credit utilization and average account age — both factors lenders look at.

None of this means 0% cards are bad. It means they reward a specific kind of discipline, and it’s worth being clear-eyed about whether that’s you right now.

How to Choose the Right Option

A simple way to work through it:

- Add up the total balance or purchase amount you’re trying to finance.

- Divide it by the number of months in the promo period. That’s your real, non-negotiable monthly payment.

- Check whether that payment fits your actual budget — not your optimistic budget.

- Confirm whether the offer is true 0% APR or deferred interest. This single distinction matters more than almost anything else on this list.

- Check the balance transfer fee, if applicable, and add it to your starting balance before doing the math.

- Know what the APR reverts to once the promo ends, in case you don’t finish paying it off.

- Check your credit score through a free service like Experian, Equifax, or TransUnion before applying, so you’re not guessing at your odds.

If the math works at every step, a 0% card is a genuinely useful tool. If it falls apart at step 3, it’s worth looking at alternatives before applying.

Frequently Asked Questions

Does applying for a 0% interest credit card hurt my credit score? Applying typically triggers a hard inquiry, which can lower your score by a small, temporary amount. Opening a new account can also lower your average account age. Most people see these effects fade within a few months, especially if they keep the balance low and pay on time.

What happens if I don’t pay off the balance before the 0% period ends? On a true 0% APR card, you start accruing interest on whatever balance remains, at the card’s standard rate, going forward. On a deferred-interest card, you can be charged interest retroactively on the entire original balance — which is a much bigger hit. This is why knowing which type of offer you have matters so much.

Is a balance transfer card better than a personal loan? It depends on your timeline. A balance transfer card works well if you can realistically clear the debt within the promo window. A personal loan with a fixed rate and term tends to work better for larger balances or longer payoff timelines, since there’s no risk of a rate suddenly jumping if you run out of time.

Can I get a 0% card with average or fair credit? It’s possible but less common. The longest and most generous 0% offers typically go to applicants with good to excellent credit. If your score is in fair territory, a credit union card or a smaller promotional window may be more realistic.

Do balance transfers count as cash advances? No, balance transfers and cash advances are treated differently, but neither one usually qualifies for 0% purchase APR promotions, and cash advances almost always start accruing interest immediately with no grace period. Don’t assume a 0% offer covers cash advances unless the terms specifically say so.

Will moving a balance close my old credit card account? Not automatically. Your old card typically stays open with a zero or reduced balance unless you choose to close it. Many people choose to keep it open (and unused) to preserve their credit history length and overall credit utilization ratio.

Final Thoughts

A 0% interest credit card isn’t a trick, and it isn’t magic — it’s a tool with a deadline attached. Used with a real payoff plan, it can save you hundreds or even thousands of dollars in interest. Used without one, it can quietly turn into the same debt you started with, plus a transfer fee and a new hard inquiry on your credit report.

Before applying for any offer, run the actual numbers: your balance, the promo length, the monthly payment that requires, and what happens if you don’t finish in time. If those numbers fit your real budget, a 0% card is worth considering. If they don’t, it’s worth looking at a personal loan, a credit union card, or talking to a nonprofit credit counselor before taking on a new account.

This article is for general educational purposes and isn’t personalized financial advice. Your best option depends on your individual credit profile, income, and debt situation — when in doubt, a nonprofit credit counselor or a fee-only financial advisor can look at your specific numbers.