That End Date Is Closer Than You Think

Most people apply for a 0% APR card with good intentions. Pay down debt. Buy something big. Float a balance for a few months without paying interest. It sounds straightforward — and honestly, it can work well if you know what’s coming.

The problem is that a lot of cardholders don’t fully understand what happens the moment that promotional period is over. They know something changes. They’re just not sure what, exactly, or how bad it could get.

If your 0% period is ending soon — or you’re considering one of these cards — this article will give you a clear, honest picture of what to expect.

Table of Contents

Quick Answer

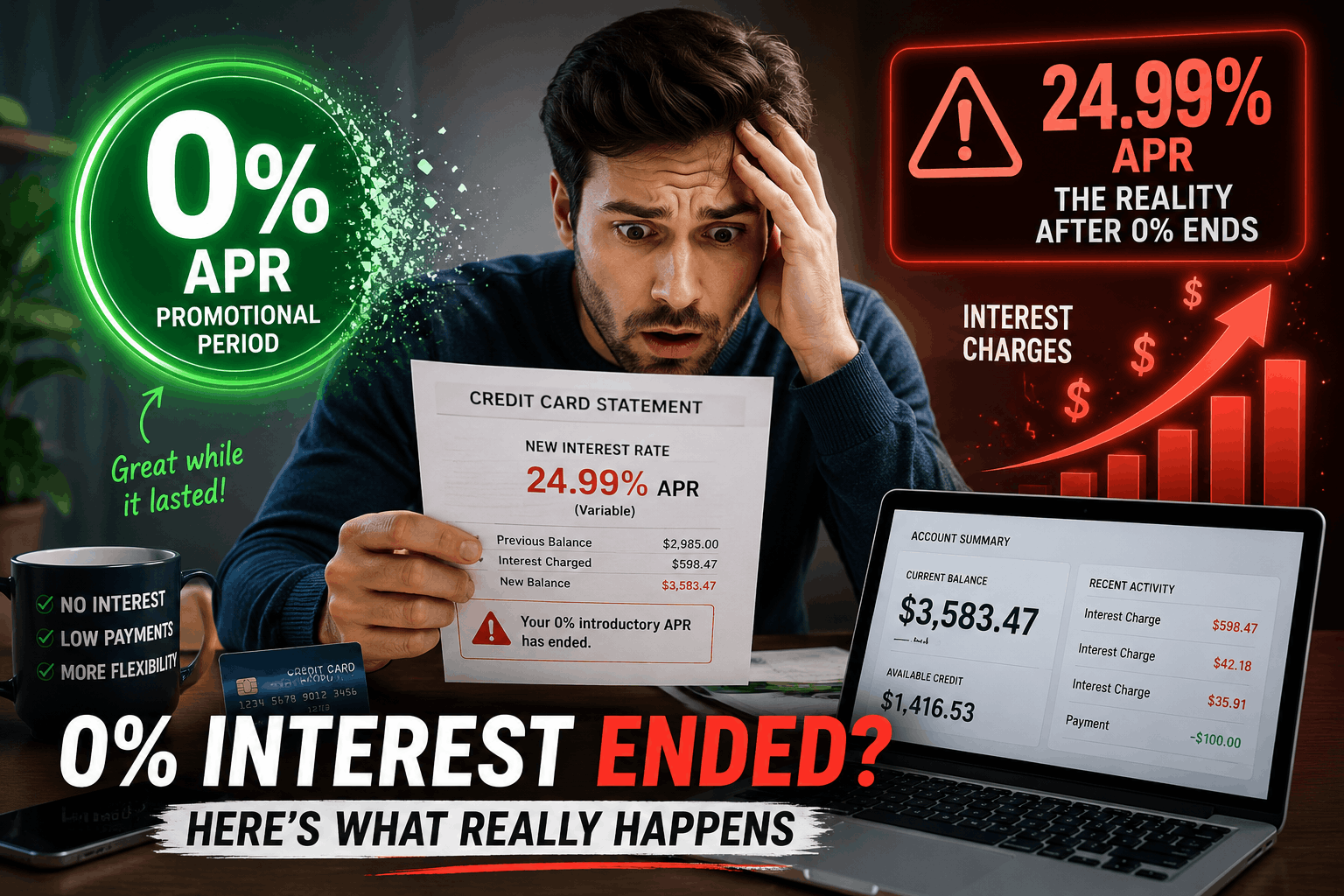

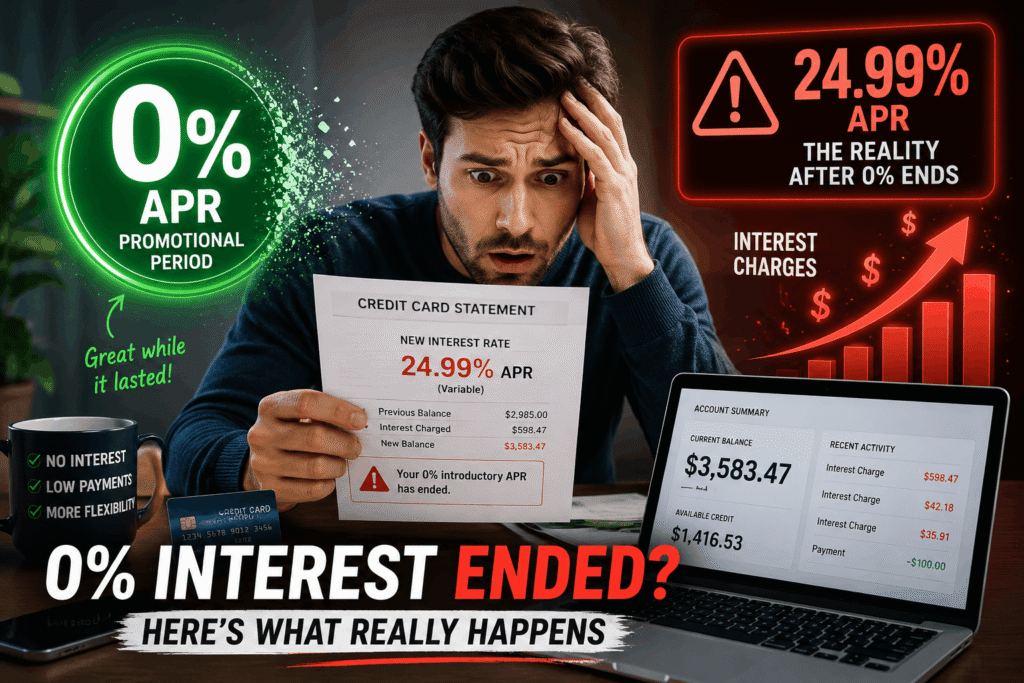

When your 0% APR promotional period ends, the card issuer switches your balance to the card’s regular (ongoing) APR. Any remaining balance immediately starts accruing interest at that rate.

On most credit cards, that regular APR is somewhere between 20% and 30%. On store-branded cards with deferred interest, the situation can be significantly worse (more on that below).

What Changes After the 0% Period Ends

| What Changes | What It Means for You |

|---|---|

| Interest rate | Jumps from 0% to the card’s regular APR |

| Monthly cost | Minimum payments may increase |

| Payoff timeline | Slows down if you carry a balance |

| Deferred interest (store cards) | Can charge interest on the full original balance retroactively |

What the 0% Period Actually Is

A 0% APR offer is a promotional rate — temporary by design. Card issuers use it to attract new customers. The idea is that you get a window, typically 12 to 21 months, where no interest is charged on purchases, balance transfers, or both.

The card itself always has a standard APR. That rate is disclosed in the cardholder agreement, usually shown as a range like “19.99%–29.99% variable APR.” The 0% period simply pauses that rate. It doesn’t eliminate it.

When the promotional period expires, the standard APR kicks in automatically. You don’t need to do anything for it to happen. The bank doesn’t send a warning the day before. Your statement might not even emphasize it clearly.

What Actually Happens on the Day It Ends

The day after your 0% period closes, your remaining balance is subject to the card’s regular purchase or balance transfer APR. Interest starts accruing immediately.

Here’s what that looks like in practical terms:

Say you transferred $4,000 to a 0% balance transfer card. You paid off $1,500 during the promo period. You have $2,500 left. The day the promo ends, that $2,500 begins accumulating interest at the card’s standard rate — often somewhere in the mid-to-high 20s.

At 26% APR, that $2,500 would accrue roughly $54 in interest the first month. Not catastrophic. But it compounds, and if you’re only making minimum payments, you’ll pay far more than $54 before it’s cleared.

The Deferred Interest Trap (This Is Different and Much Worse)

This is the section most people skip, and it costs them money.

There are two fundamentally different types of “0% interest” offers:

True 0% APR cards — These are standard credit cards (Citi, Chase, Discover, etc.) that offer a genuine promotional period. If you carry a balance after the promo ends, interest only applies going forward. Whatever you already paid down is gone. You’re only charged on what’s left.

Deferred interest offers — These are common on store credit cards (think retail financing at furniture stores, electronics chains, medical providers). The language often says “no interest if paid in full within 12 months.” That phrase “if paid in full” is the key difference.

With deferred interest, the interest was never forgiven. It was deferred — sitting in the background, waiting. If you don’t pay the full original balance before the deadline, the issuer charges you all the accumulated interest from day one of the purchase. Every penny.

That catches borrowers off guard constantly. You buy a $2,000 couch, make regular payments, have $200 left at the deadline, and suddenly get hit with $300+ in retroactive interest you thought you were avoiding.

True 0% APR vs. Deferred Interest — Key Differences

| Feature | True 0% APR Card | Deferred Interest (Store Card) |

|---|---|---|

| Interest during promo | None charged | Accrues silently in background |

| If you don’t pay in full | Interest on remaining balance only | Interest on original full balance, retroactive |

| Penalty for $1 remaining at deadline | Small | Can be hundreds of dollars |

| Typical issuers | Major banks | Store cards, retailer financing |

| Phrase to watch for | “0% APR for X months” | “No interest if paid in full” |

If you’re financing something at a retail store and the terms say “no interest if paid in full” — that’s deferred interest. Pay it off completely before the deadline, or don’t use that offer at all.

Real-World Cost Examples

These are simple illustrations to show how the math actually plays out.

Scenario 1: True 0% Card, Balance Not Fully Paid

- Balance transferred: $5,000

- Payments during 15-month promo: $2,400

- Remaining at end of promo: $2,600

- Card’s regular APR: 24.99%

- Monthly interest once promo ends: ~$54

That’s $54/month on top of principal repayment. Over a year of carrying that balance, you’d add roughly $600+ in interest costs.

Scenario 2: Deferred Interest Store Card, Almost Paid Off

- Original purchase: $1,800 furniture

- Payments made over 12 months: $1,650

- Remaining at deadline: $150

- Deferred interest rate: 29.99%

- Retroactive interest charged: approximately $440 (12 months of accrued interest on $1,800)

The cardholder thought they were nearly done. They ended up paying $440 more than expected because they didn’t clear that last $150 in time.

The contrast between these two scenarios is significant. True 0% offers are genuinely useful financial tools. Deferred interest offers require extreme caution.

Hidden Fees and Fine Print to Watch

Beyond the APR jump itself, a few other things are worth knowing.

Balance transfer fees — Most balance transfer cards charge 3%–5% of the transferred amount upfront. This fee isn’t affected by the 0% period ending, but it does affect your total cost. A 3% fee on a $6,000 transfer is $180 — factor that into your math before assuming the offer is free.

The minimum payment trap — During the 0% period, making only the minimum payment feels harmless. But if you’re not meaningfully reducing the balance, you’ll still have a large balance when the promo ends. Minimum payments during a 0% promo are often the reason people find themselves in a worse position than expected.

Variable APR — Most credit card APRs are variable, tied to the prime rate. The APR you see today isn’t guaranteed to stay at that level after your promo ends. If rates rise, your post-promo rate could be higher than what was advertised at the time you applied.

Late payment penalties — Missing a payment during the promo period can void the promotional rate entirely, on some cards. The issuer can apply a penalty APR immediately. Read the cardholder agreement carefully and set up autopay at minimum for the minimum payment.

Common Mistakes People Make

Forgetting the end date — It sounds basic, but it happens constantly. The promo period ends, interest kicks in, and the cardholder is genuinely surprised. Calendar the end date the day you get the card.

Making minimum payments only — The whole point of a 0% period is to pay down a balance without interest eating into your progress. Using it to make minimum payments wastes the benefit.

Applying for a 0% card with no payoff plan — If you don’t have a realistic monthly budget to pay off the balance before the promo ends, the interest charges afterward can partially or fully erase what you saved.

Confusing 0% purchase APR with 0% balance transfer APR — These are separate promotional terms on most cards. A card that offers 0% on purchases may charge the standard APR on balance transfers immediately, and vice versa. Check which purchases or transactions the promo rate actually applies to.

Not reading the deferred interest fine print — As covered above. The phrase “if paid in full” is the red flag. If you see it, treat the offer as a strict deadline, not a flexible grace period.

Who Should Probably Avoid These Cards

Not everyone is well-positioned to use 0% APR cards effectively.

People who tend to carry revolving balances — If you historically pay the minimum each month and carry a balance for years, a 0% offer won’t change that pattern. You’ll likely end up with a new balance on top of the old one once the promo ends.

People with thin credit files or lower credit scores — 0% cards generally require good to excellent credit (roughly 670+ FICO score, with the best offers starting around 720). Applying and getting denied can temporarily ding your credit score.

Anyone financing through a store card without a clear payoff plan — Deferred interest offers are particularly risky for people who don’t track their exact balance and payment timing.

People close to a major loan application — Applying for a new credit card shortly before applying for a mortgage or auto loan can affect your credit score through both the hard inquiry and the reduction in average account age.

What to Do Before the Promo Period Ends

If your 0% period is ending soon and you still have a balance, here’s how to think about it:

Calculate exactly what’s left — Log into your account and get the current balance. Don’t rely on memory.

Estimate the post-promo interest cost — Multiply your remaining balance by the APR, then divide by 12. That’s your approximate monthly interest charge once the promo ends. Decide if that’s tolerable or if it requires more aggressive payoff action now.

Consider a balance transfer to a new 0% card — If you have good credit and the remaining balance is large, you may qualify for another 0% balance transfer card. Just account for the balance transfer fee (usually 3%–5%) in your comparison. This only makes sense if the interest savings outweigh the fee.

Increase payments during the final months — Even if you can’t pay it all off, reducing the balance before the promo ends minimizes how much interest you’ll pay afterward.

Set up autopay if you haven’t — At minimum, ensure you’re not missing payments, which can trigger penalty rates.

How to Choose the Right Approach

Quick Decision Guide

| Your Situation | Best Move |

|---|---|

| Balance nearly paid, a few months left | Push hard to clear it fully |

| Large balance, good credit | Consider balance transfer to new 0% card |

| Store card, “if paid in full” terms | Prioritize full payoff above all else |

| Can afford to absorb new APR | Carry the balance but increase monthly payments |

| Balance is unmanageable | Consider a personal loan at lower fixed APR |

There’s no single right answer — it depends on your balance size, your available monthly cash flow, and your credit profile. The key is making a deliberate decision rather than letting the end date arrive without a plan.

Frequently Asked Questions

Does my interest rate go up automatically when the 0% period ends? Yes. The card issuer applies the standard APR to any remaining balance as soon as the promotional period expires. You don’t need to do anything — it happens automatically.

Will my minimum payment increase after the 0% period ends? It can. Minimum payments are typically calculated as a percentage of your balance, which now includes interest charges. Your actual payment amount may increase slightly.

Can I call the bank and ask for an extension on the 0% rate? You can ask, but issuers are rarely willing to extend promotional rates. It’s possible in some cases for customers with strong payment history, but don’t count on it as a strategy.

What’s the difference between 0% APR and deferred interest? With a true 0% APR card, you’re only charged interest on whatever balance remains after the promo ends. With deferred interest, if you don’t pay the full original balance by the deadline, you’re charged all the interest that was silently accruing from day one. Deferred interest can be significantly more expensive.

Does carrying a balance after the promo end hurt my credit score? It doesn’t hurt your score directly, but a high utilization ratio — your balance relative to your credit limit — can lower your score. Keeping your balance below 30% of the card’s limit is generally recommended.

If I transfer a balance to a new 0% card before my current promo ends, does the clock restart? Yes, you’d start a new promotional period on the new card. Just factor in the balance transfer fee, and confirm the new card’s terms before applying.

Can I still use the card normally after the 0% period ends? Yes. The card doesn’t expire or change functionally. New purchases will just be subject to the regular APR from that point forward, unless there’s a separate purchase APR promotion.

Final Thoughts

A 0% APR promotional period is a useful financial tool — but only if you treat it as exactly that: a tool with a deadline.

The interest rate change at the end of the promo isn’t a punishment. It’s simply the card’s normal operating terms resuming. The issuers disclosed it. They just don’t go out of their way to remind you it’s coming.

Understanding the difference between a true 0% APR card and a deferred interest offer matters a lot. Knowing your end date, having a payoff plan, and avoiding the minimum-payment-only trap are what separate people who genuinely benefit from these offers from those who end up paying more than they expected.

If you’re currently in a 0% period, use it aggressively. If you’re considering one, go in with math, not optimism.

This article is for informational purposes only and does not constitute financial advice. Interest rates and card terms vary by issuer. Review your cardholder agreement for the specific terms of your account.