Most people don’t understand their credit card interest until they open a statement and see their balance has somehow grown — even though they barely touched the card that month. That moment of confusion is frustrating, and it happens to a lot of people.

Credit card interest is technically disclosed in your cardholder agreement. But it’s written in a way that takes three reads and a lot of patience to decode. If you’ve ever wondered why your balance barely moves even when you’re making payments, or why a small purchase seems to cost more than it should, this guide is for you.

No jargon. No filler. Just a straight explanation of how credit card interest actually works — and what it means for your wallet.

Table of Contents

Quick Answer: How Credit Card Interest Works

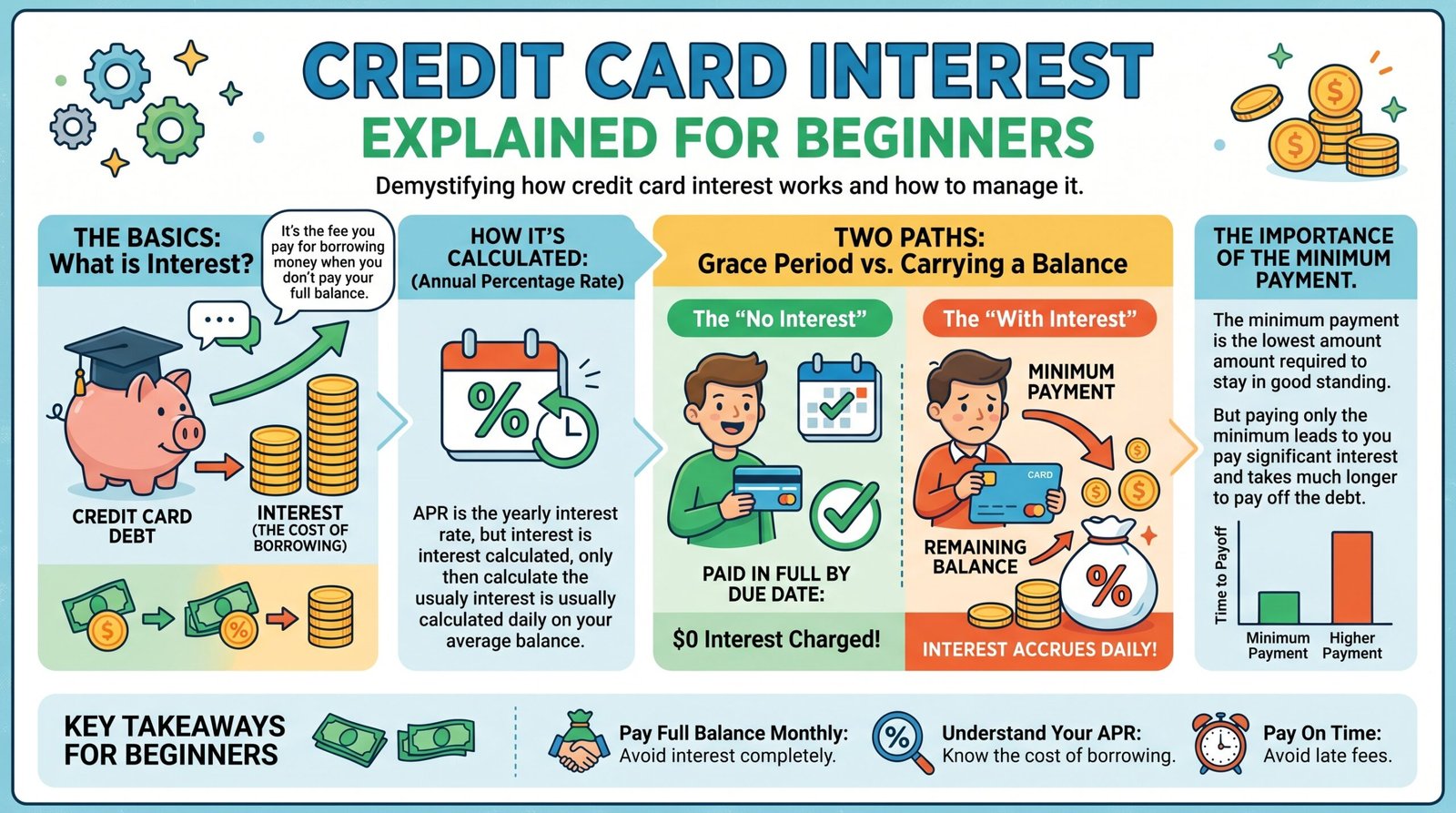

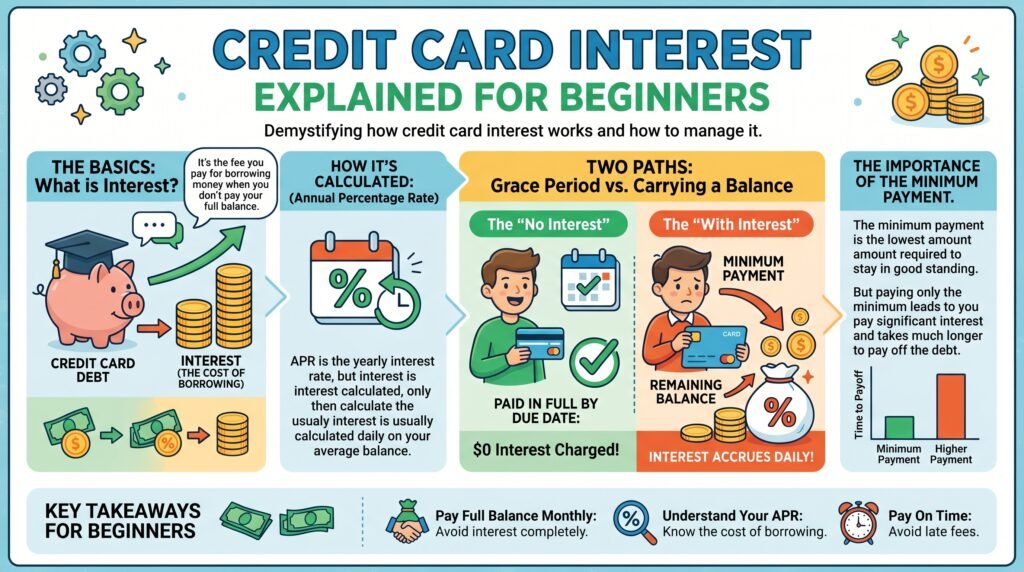

Your credit card charges interest when you carry a balance from one month to the next. The rate is called the APR (Annual Percentage Rate), but it’s applied daily — not once a year. That’s where most people get confused.

The basics:

- If your APR is 24%, your daily rate is roughly 0.066%

- That rate applies to your unpaid balance every single day

- Interest compounds, meaning you pay interest on interest over time

| Term | Plain-Language Meaning |

|---|---|

| APR | Your annual interest rate (e.g., 24%) |

| Daily Periodic Rate | APR divided by 365 — applied each day |

| Grace Period | Days after statement closes where no interest is charged, if you pay in full |

| Minimum Payment | The smallest amount to avoid a late fee — not a debt payoff plan |

| Balance Transfer APR | Rate used when you move debt from another card |

What Is Credit Card Interest, Really?

Think of it as a fee for borrowing money. When you swipe your card, the credit card company covers that purchase. If you repay the full amount before the due date, you borrowed for free. If you don’t, they charge a percentage of what you owe — and that percentage compounds daily.

Here’s how the math works:

- APR: 24%

- Daily rate: 24% ÷ 365 = 0.0658% per day

- Balance carried: $1,000

- Daily interest charge: approximately $0.66

That $0.66 gets added to your balance. The next day, interest is calculated on $1,000.66. Then $1,001.32. Compounding means each day’s interest is slightly larger than the day before. Over months, this adds up faster than most people expect — especially when the minimum payment barely keeps pace.

The Grace Period — And Why It Disappears

If you pay your full statement balance by the due date every month, you won’t pay a single dollar in interest. That’s the grace period in action — typically 21 to 25 days between when your statement closes and when the payment is due.

Here’s what catches people off guard: the grace period disappears the moment you carry a balance.

Say you owed $500 last month and paid $400. The remaining $100 rolls over. Now, interest starts accruing on your new purchases immediately — even on things you bought the day your statement closed. You don’t get those interest-free days back until you’ve paid the full balance.

This is one of the most misunderstood mechanics in all of personal finance. Carrying even a small balance can quietly make every new purchase more expensive.

The Different Types of Credit Card APR

Most people only know about the purchase APR. But your card actually has several interest rates depending on how you use it.

Purchase APR

The standard rate on everyday spending when you carry a balance. This is the number you see most prominently advertised — typically somewhere between 20% and 30% for most cardholders today, based on Federal Reserve data tracking.

Cash Advance APR

Almost always higher than your purchase rate — often 25% to 30% or more. And there’s no grace period. Interest starts accumulating the second the cash hits your hand. For most situations, cash advances are worth avoiding.

Balance Transfer APR

Some cards offer 0% promotional rates for 12 to 21 months when you transfer debt from another card. When that window closes, the rate jumps — sometimes significantly. If you haven’t paid off the transferred balance by then, you’ll face a steep interest spike on whatever’s left.

Penalty APR

Miss a payment or pay late, and many card issuers can bump your rate to a penalty APR — as high as 29.99%. Depending on the card’s terms, this can apply to your entire existing balance, not just new charges.

| APR Type | Typical Range | Grace Period? |

|---|---|---|

| Purchase APR | 20%–30% | Yes, if paid in full |

| Cash Advance APR | 25%–30%+ | No |

| Balance Transfer APR | 0% promo, then 20%–28% | Varies |

| Penalty APR | Up to 29.99% | No |

Real-World Cost Examples

Scenario 1: Paying the Minimum Only

- Balance: $2,000

- APR: 24%

- Minimum payment: ~$40/month

At this pace, paying off that $2,000 takes over 8 years — and you’d pay nearly $2,000 in interest on top of the original balance. You’d essentially pay for the same purchase twice.

Scenario 2: Paying a Fixed Higher Amount

- Same $2,000 balance, same 24% APR

- Monthly payment: $150

Payoff time: about 15 months Total interest paid: roughly $300

That one decision — paying $150 instead of $40 — saves over $1,700. Same debt. Very different outcomes.

Scenario 3: Forgetting a Small Balance

- Balance: $300

- APR: 24%

- Unpaid for two billing cycles

Interest accrued: roughly $12–$14. Sounds small. But this habit across two or three cards, compounded over a year, becomes a real cost with nothing to show for it.

Hidden Fees and Interest Traps

Deferred Interest Promotions

This is not the same as 0% APR — and the difference matters a lot. Deferred interest means that if you don’t pay off the entire balance before the promotional period ends, you get charged all the back interest from day one. Retail store cards and some furniture financing deals use this structure. The promotional rate feels like a free loan. It isn’t.

Balance Transfer Fees

Even a 0% APR offer usually comes with a 3%–5% upfront fee on the amount transferred. On $5,000, that’s $150–$250 immediately. For most people, this still beats a 24% APR — but you need to factor it into your calculation before assuming the transfer saves money.

Minimum Payment Trap

The minimum payment exists to prevent a late fee. It’s not designed to help you get out of debt quickly. It’s the floor — and staying close to it keeps interest charges running as long as possible.

Cash Advance Fees

Beyond the higher APR, most cards charge a cash advance fee of 3%–5% upfront. Withdraw $500 and you immediately owe $515–$525, with interest accruing from that moment. This is one of the most expensive ways to access money.

Variable APRs

Most credit card rates are variable, tied to the prime rate, which moves when the Federal Reserve adjusts its benchmark. When the Fed raises rates — as it did repeatedly in 2022 and 2023 — your card’s APR increases automatically. Most cardholders don’t notice until they see the statement.

Common Mistakes Beginners Make

Treating the minimum payment as a real repayment plan. It keeps your account in good standing, but it barely touches principal on a high-interest balance. It’s the most expensive way to carry debt.

Assuming 0% means zero interest forever. A promotional 0% APR expires. After 12 or 21 months, the full regular APR kicks in. Any remaining balance starts accruing interest at the standard rate immediately.

Not understanding that cash advances are expensive loans. Many cardholders treat them like regular withdrawals. They’re not. Higher rate, no grace period, immediate fee — the cost adds up quickly.

Carrying a balance and expecting the grace period to still apply. Once you carry any amount from month to month, new purchases start accruing interest right away. A lot of people don’t realize this until they see the charge on their next statement.

Focusing on the monthly payment without calculating the total. A $500 balance paid back at $25/month on a 24% APR card doesn’t cost $500. It costs significantly more by the time it’s cleared. The monthly number looks manageable. The total isn’t always.

Who Should Be Extra Careful With Credit Card Interest?

Credit cards aren’t inherently dangerous — but they carry more financial risk for certain people.

Those with variable or unpredictable income may carry balances more often than planned. One slow month can turn a manageable balance into a growing one that’s harder to clear.

Anyone already carrying debt across multiple accounts should be cautious about adding more revolving credit without a clear payoff strategy. Interest compounds across balances simultaneously.

People who tend to spend impulsively may find that swiping a card doesn’t feel like spending real money — which makes it easier to overspend and harder to stay within budget.

Anyone considering store-branded retail cards should read the terms carefully. These cards often feature deferred interest, not true 0% APR, and the distinction is buried in the fine print.

How to Choose the Right Card If You Sometimes Carry a Balance

If carrying a balance is a realistic part of your financial life, the card’s interest rate matters far more than its rewards program. Earning 2% cash back while paying 27% APR is not a net gain.

Look for:

- A lower regular APR (credit unions often offer better rates than major banks)

- No penalty APR clause, or a limited one

- A 0% balance transfer intro offer if you have existing debt to consolidate

Be cautious of:

- Retail store cards with deferred interest structures

- High-rewards cards with high APRs — these only make sense if you pay in full monthly

- Cards that advertise sign-up bonuses prominently while listing the APR in footnotes

| Card Type | Good Fit If You… | Watch Out For |

|---|---|---|

| Low APR Card | Sometimes carry a balance | Fewer rewards perks |

| 0% Balance Transfer Card | Have high-interest debt to move | Transfer fee, rate after promo ends |

| Rewards Card | Pay in full every month | High APR makes carrying costly |

| Store/Retail Card | Shop heavily at one retailer | Deferred interest, limited usability |

Frequently Asked Questions

What is a good APR for a credit card?

There’s no universal standard, but Federal Reserve data shows average credit card APRs have been sitting well above 20% for most accounts in recent years. Anything below 20% is generally considered better than average. Credit unions tend to offer lower rates than major national banks.

Does credit card interest affect your credit score?

Interest charges don’t appear as a separate line item on your credit report. But carrying a high balance relative to your credit limit — called credit utilization — does affect your score. Keeping utilization below 30% is generally recommended by Experian, Equifax, and TransUnion.

What happens if I only pay the minimum?

Your account stays in good standing and you avoid late fees. But the interest compounds, and you’ll pay significantly more over time. On a $2,000 balance at 24% APR, minimum payments could take nearly a decade to clear.

Can my credit card company raise my interest rate?

Yes. For variable rate cards, your APR adjusts automatically when the prime rate changes. Issuers can also raise your rate after 45 days’ written notice for creditworthiness-related reasons. The CARD Act of 2009 provides some protection for existing balances, but new purchases can be subject to the new rate.

Is it better to pay off credit card debt or invest?

For most people, paying down high-interest credit card debt first makes financial sense. A guaranteed 24% APR savings is difficult to beat with an investment return. The one common exception: always contribute enough to get the full employer match on a 401(k) — that’s effectively a 50%–100% immediate return.

What does “no preset spending limit” mean?

It refers to charge cards or certain premium credit products where the limit flexes based on your payment history and spending patterns. It doesn’t mean unlimited spending. Interest rules still apply if a balance is carried.

Final Thoughts

Credit card interest is genuinely simple once you understand the mechanics. The daily compounding, the grace period rules, the different APR types — all of it flows from one basic fact: you can borrow for free if you pay in full, or borrow expensively if you don’t.

If you’re currently carrying a balance, the most useful first step is to know exactly what rate you’re paying and calculate how long it will take to clear at your current payment level. Then decide whether increasing your monthly payment, consolidating with a balance transfer, or both makes the most sense.

There’s no single right answer for everyone. But having the numbers in front of you — rather than ignoring the statement — removes the guesswork and keeps a manageable debt from quietly becoming an unmanageable one.

Credit cards work well as a tool. They’re expensive as a crutch.

Related Reading: How to Pay Off Credit Card Debt Faster | What Is a Balance Transfer and Is It Worth It | How Credit Utilization Affects Your Credit Score | How to Read Your Credit Card Statement