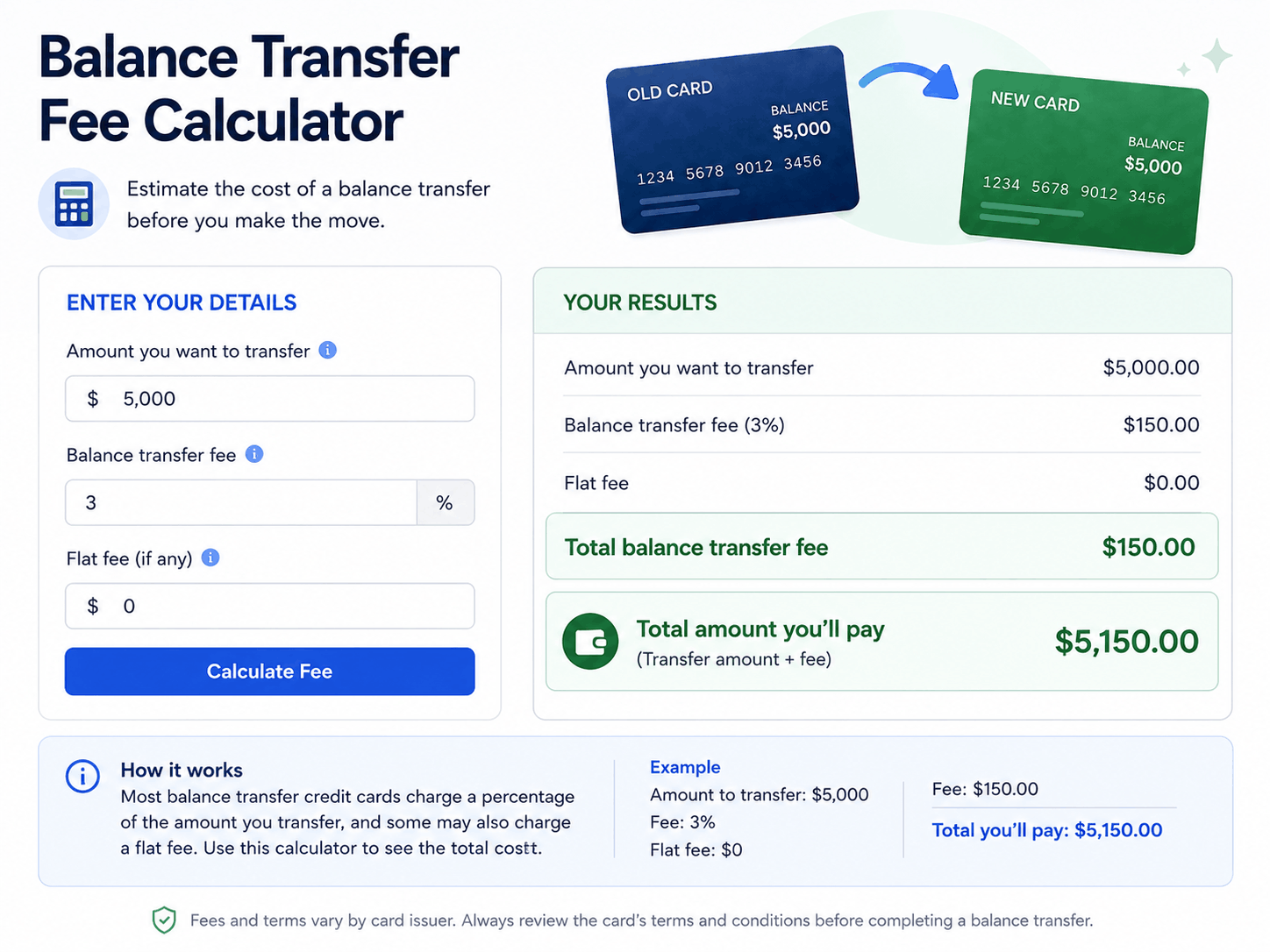

Balance Transfer Fee Calculator

Find out if a balance transfer saves you money — or costs you more than it’s worth.

You’ve found a 0% APR balance transfer offer and it sounds like a lifeline. No interest for 18 months — finally some breathing room. But before you pull the trigger, there’s a number most people skip right past: the transfer fee. That 3% to 5% charge added to your balance on day one can quietly eat a chunk of your savings before you even make a single payment.

Use the calculator above to run your own numbers. The article below explains exactly what you’re calculating, what the results mean, and what the fine print doesn’t tell you.

Quick Answer: What Is a Balance Transfer Fee?

A balance transfer fee is a one-time charge — typically 3% to 5% of the amount you move — applied when you transfer debt from one credit card to another. On a $6,000 balance, that’s $180 to $300 added to your new card immediately.

The trade-off: you pay that fee upfront in exchange for a 0% promotional APR period, usually lasting 12 to 21 months. The question the calculator answers is simple — is the interest you’d save worth more than the fee you’re paying?

| Factor | Typical Range |

|---|---|

| Transfer fee | 3%–5% of balance |

| Promo APR period | 12–21 months |

| Regular APR after promo | 19%–29%+ |

| Minimum credit score needed | 670+ (good credit) |

| Time to process transfer | 7–14 business days |

| Same-bank transfers allowed? | No |

How the Balance Transfer Fee Calculator Works

The calculator above does four things:

1. Calculates your transfer fee — Takes your balance and multiplies it by the fee percentage. This is the upfront cost you pay on day one.

2. Estimates interest you’d save — Simulates what you’d pay in interest on your current card over the promo period, assuming the same monthly payment. This is the money you’re trying to avoid.

3. Shows your net savings — Subtracts the fee from the interest saved. If it’s positive, the transfer makes financial sense. If it’s negative, you’d actually come out worse.

4. Projects your remaining balance — Based on your monthly payment, it shows what you’d still owe when the promo period ends. This matters a lot, because whatever’s left gets hit with the regular APR.

Why the Monthly Payment Field Matters

A lot of people focus only on the fee and ignore whether they can actually pay off the balance in time. The calculator factors in your payment so you can see what happens to your balance by month 12, 15, or 18 — not just what the fee costs today.

If you’re putting $150/month toward a $7,000 balance on a 15-month promo card, you’ll still have about $4,750 remaining when the 0% window closes. At 24% APR, that’s a painful restart. The calculator surfaces that reality before you commit.

What Is a Balance Transfer? (Plain Language Explanation)

A balance transfer moves your existing credit card debt to a new card — usually one offering 0% interest for an introductory period. Instead of your current issuer charging 20%+ APR every month, the new card charges nothing during the promo window.

The mechanics are simple. You apply for the new card, request the transfer, and the new issuer pays off your old card (or a portion of it, up to your approved credit limit). You now owe the new card instead.

Here’s what trips people up: the transfer doesn’t erase the debt. It relocates it. You still owe the same amount — plus the transfer fee — just to a different institution and at a different rate. If your spending habits don’t change, or your monthly payments stay too low, the debt doesn’t shrink meaningfully.

When Does a Balance Transfer Make Financial Sense?

Run the numbers with the calculator, but here’s the general logic:

The transfer is worth it when:

- The interest you’d save over the promo period is noticeably larger than the transfer fee

- You can commit to monthly payments that realistically pay off (or significantly reduce) the balance before the promo ends

- Your current APR is 18% or higher

The transfer may not be worth it when:

- Your balance is small (under $1,000–$1,500) and the fee eats most of the savings

- The promo period is short (12 months or less) and your required monthly payment is unrealistic

- You’re carrying debt at a lower rate (under 12%) where the math barely favors a transfer

Real-World Cost Comparison

Let’s use a concrete example. You have $5,000 at 22% APR and you’re paying $300/month.

Without a balance transfer: Over 18 months, you’d pay roughly $900–$1,000 in interest before the debt is cleared.

With a balance transfer (3% fee, 0% for 18 months): Transfer fee: $150. Interest during promo: $0. Net saving: roughly $750–$850.

At a 5% fee, the cost rises to $250. Net saving drops to around $650–$750. Still worth it — but the advantage narrows.

Now change the scenario: $1,200 balance, 18% APR, $200/month. Over 6–7 months you’d pay maybe $70 in interest naturally. A 3% fee costs $36. Savings are minimal and the credit inquiry plus new account on your report may not be worth it.

Hidden Costs the Calculator Can’t Capture

The math in the calculator covers the core trade-off. But a few costs fall outside the numbers:

Hard credit inquiry: Applying for a balance transfer card triggers a hard pull on your credit report. This typically drops your score 5–10 points temporarily. That’s usually fine — but if you’re planning a mortgage or auto loan soon, timing matters.

Average account age: Opening a new card lowers the average age of your accounts, which affects your credit score. For most people, this is temporary and minor. But it’s worth knowing.

New purchase APR: Many 0% balance transfer cards apply the promo rate only to transferred balances, not new purchases. If you use the card for everyday spending, those charges often accrue interest at the regular rate from day one. Worse, payments frequently get applied to the lower-rate balance first, letting the high-rate purchases compound.

Penalty rate elimination: If you miss a payment — even once — some issuers will cancel your promotional APR entirely. Read the cardholder agreement. The penalty APR can jump to 29.99% immediately, applied to your full remaining balance.

Balance transfer windows: Many cards require you to complete the transfer within 60 days of account opening to receive the promotional rate. Transfer after that window and you may lose the 0% offer entirely.

Three Balance Transfer Fee Scenarios

Scenario 1: The Clear Win

Balance: $8,000 | APR: 24% | Fee: 3% | Promo: 21 months | Monthly payment: $420

Transfer fee: $240. Without a transfer, $8,000 at 24% APR with $420/month over 21 months generates roughly $1,700+ in interest. Net saving: well over $1,400. The math is straightforward. This is exactly what balance transfers are designed for.

Scenario 2: The Break-Even Zone

Balance: $2,500 | APR: 18% | Fee: 5% | Promo: 12 months | Monthly payment: $210

Transfer fee: $125. Interest saved over 12 months: roughly $200–$240. Net saving: $75–$115. Technically positive, but the credit inquiry and administrative effort may not be worth a $75–$100 gain for everyone. Reasonable people could go either way.

Scenario 3: The Trap

Balance: $6,000 | APR: 21% | Fee: 3% | Promo: 15 months | Monthly payment: $150

Transfer fee: $180. Over 15 months, $150/month only pays down about $2,250 of principal. You’d still owe roughly $3,750 when the promo ends. At 26% regular APR, that leftover balance becomes a new expensive problem. The transfer saved interest during the promo window but left the person in a worse position because the payment was too low.

Common Mistakes When Calculating Balance Transfer Costs

Forgetting that the fee adds to the balance. The 3% fee doesn’t come out of your pocket separately — it gets added to the balance you now owe on the new card. If you transfer $5,000 at 3%, your new balance starts at $5,150.

Only looking at the fee, not the remaining balance. The fee is day-one math. The bigger risk is what happens at month 13 or month 19 when the promo ends and you still have $3,000 sitting there.

Assuming the minimum payment is a plan. Minimum payments are designed to keep you in debt longer. If your minimum is $75/month on a $6,000 balance, you will not pay it off in any promo period. Run the actual numbers.

Not confirming what the fee percentage applies to. Some cards charge a minimum fee (e.g., 3% or $10, whichever is greater). On very small transfers, the minimum flat fee may be proportionally higher than 3%.

Transferring and then continuing to use the original card. One of the most common patterns: you transfer $4,000, feel relief, then start spending on the now-empty card again. Six months later you have $4,000 on the new card plus a growing balance on the old one.

Who Should Avoid Balance Transfers?

Balance transfers aren’t the right tool for every situation. Be clear-eyed here.

If your credit score is below 650–660, you likely won’t qualify for a card with a competitive 0% offer. You might get approved for something, but the promo period will be shorter, the credit limit lower, and the post-promo APR potentially very high.

If you can realistically pay off the debt within 3–4 months at your current rate, the transfer fee may cost more than just paying it down directly. Use the calculator — the savings may be smaller than you expect for short-payoff timelines.

If you’re currently applying for a mortgage or major loan, a new card application affects your credit profile. The timing may not be worth it.

If your financial situation is unstable, the risk of missing a payment and losing the promotional APR is real. A penalty rate at 29.99% on a large balance is worse than whatever you were dealing with before.

How to Choose the Right Balance Transfer Card

Once you’ve confirmed the transfer makes financial sense with the calculator, here’s what to evaluate:

Length of promo period first. Match the promo window to your realistic payoff timeline, not the maximum available. A 21-month card is only better than a 15-month card if you genuinely need those extra 6 months.

Compare fee percentages. Some cards offer 3%, some 5%, a few rare ones charge nothing (usually on shorter promo windows). Run the numbers on each using the calculator.

Check the regular APR. This is what you’ll pay if you have a balance left when the promo ends. A 26% regular APR is meaningfully worse than 20%. Read the terms.

Confirm the transfer window. You typically need to complete the transfer within 45–60 days of account opening to get the promo rate. Don’t wait.

Read the minimum payment requirements. Some cards require you to make minimum payments during the promo period to keep the 0% rate active. Missing one can void the entire promotion.

Frequently Asked Questions

What is a good balance transfer fee percentage? 3% is standard. Anything below 3% is favorable. A 5% fee is common on cards with longer promo periods. The fee is only “good” if the interest savings outweigh it — run the calculator before deciding.

Is a balance transfer fee worth it? It depends on four variables: your balance, your current APR, the fee rate, and your monthly payment. For most people carrying $3,000+ at 18%+ APR who can make above-minimum payments, the math works in their favor. The calculator above shows your specific numbers.

Does the balance transfer fee get charged upfront? Not exactly upfront — it’s added to the transferred balance on the new card. If you transfer $5,000 at a 3% fee, your opening balance on the new card is $5,150.

Can I avoid the balance transfer fee? A few cards offer 0% fee promotions, usually within the first 60 days. They’re less common and often paired with shorter promo periods. Search for “no balance transfer fee credit cards” and compare whether the shorter promo is still worth it given your payoff timeline.

What happens if I can’t pay off the balance before the promo ends? The remaining balance starts accruing interest at the regular APR — typically 19%–29%. It doesn’t retroactively charge interest on what you transferred. But from that point forward, the clock restarts at full rate. This is why the remaining balance figure in the calculator matters so much.

Does applying for a balance transfer card hurt my credit score? Temporarily, yes. A hard inquiry typically reduces your score by a few points for 6–12 months. Opening a new account also affects average account age. For most people, these are minor and short-lived effects — especially compared to the long-term benefit of reducing high-interest debt.

Final Thoughts

A balance transfer is a useful financial tool when used deliberately. The fee is real, the math is straightforward, and the only way to know if it works in your favor is to run the actual numbers — which is exactly what the calculator at the top of this page does.

The people who benefit most treat it as a temporary rate reduction, not a debt solution. They set up a monthly payment that will realistically clear the balance before the promo ends, they leave the old card alone, and they read the terms carefully before transferring.

The people who run into trouble either don’t calculate whether the savings exceed the fee, set monthly payments too low, or start spending on the old card again while the transfer is active.

The tool is simple. The discipline around it is the harder part.