If you’re carrying credit card debt and someone told you a balance transfer could save you hundreds in interest, your first instinct is probably: sounds too good, what’s the catch?

One of the most common worries people have before doing a balance transfer is what it’ll do to their credit score. And honestly, that concern makes sense. You’ve worked hard to build your score, and the last thing you want is a money-saving move that quietly damages it in the background.

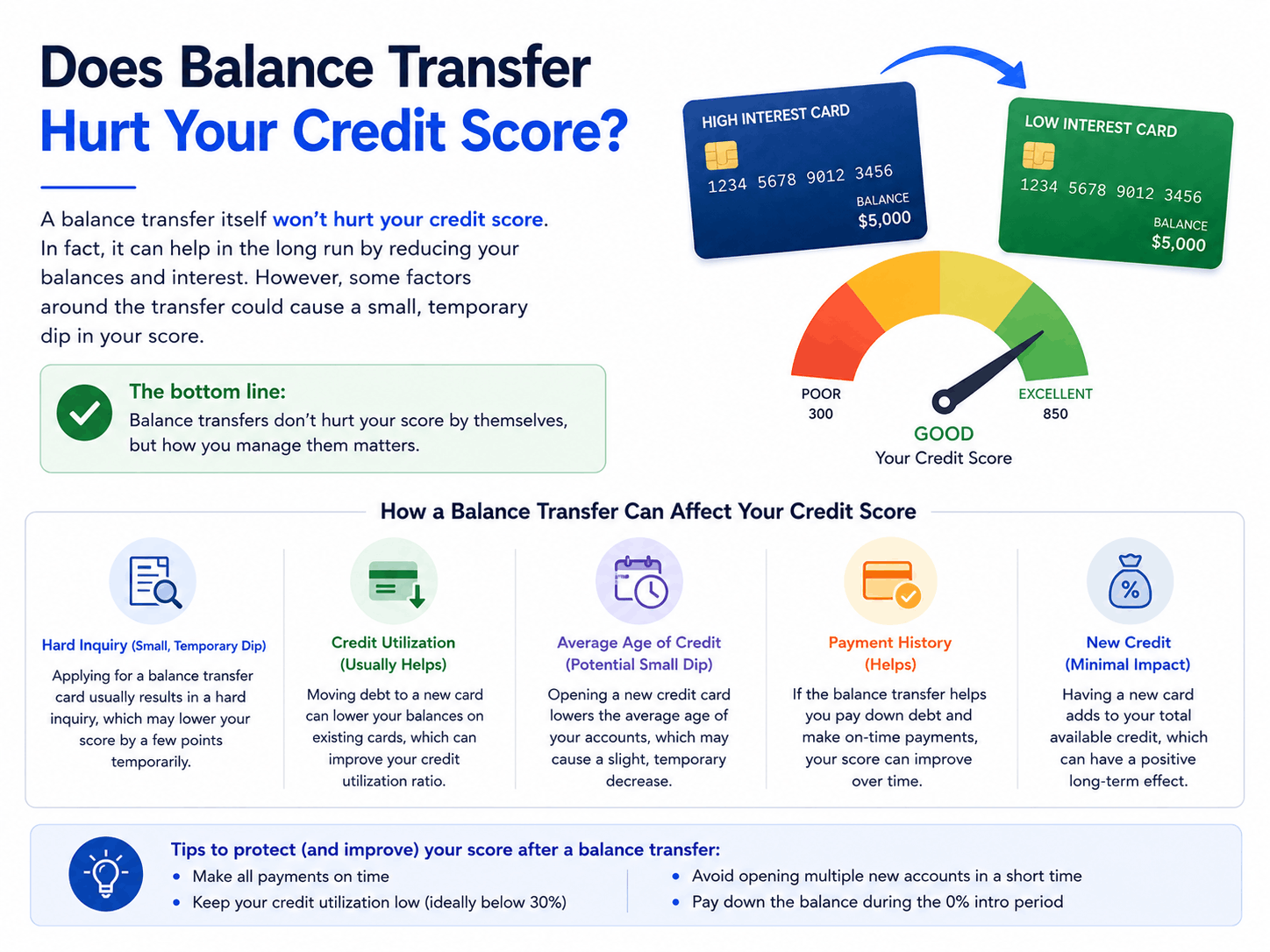

The short answer is: yes, a balance transfer can temporarily lower your credit score — but for most people, the long-term effect is actually positive. The key word is temporarily. Here’s what actually happens, why it happens, and when you should think twice.

Table of Contents

Quick Summary: Balance Transfer and Credit Score

| Factor | Short-Term Effect | Long-Term Effect |

|---|---|---|

| Hard inquiry (application) | Small dip (−2 to −5 pts) | Fades in 12 months |

| New credit account opened | Small dip | Recovers as account ages |

| Credit utilization on old card | Improves | Stays positive if card kept open |

| Utilization on new card | May rise | Improves as you pay down debt |

| Payment history | No impact if paid on time | Strengthens over time |

The bottom line: a balance transfer is a short-term credit score trade-off for a long-term financial benefit — if you use it correctly.

What Is a Balance Transfer, Exactly?

A balance transfer means moving debt from one credit card to another — usually to a card offering 0% APR for an introductory period, often 12 to 21 months. You pay a transfer fee (typically 3%–5% of the amount moved), and in exchange, you get a window to pay down principal without interest piling up.

For example: you owe $4,000 on a card charging 24% APR. If you transfer that to a 0% intro APR card with a 3% fee, you pay $120 upfront but save potentially $800–$900 in interest over the next 15 months — assuming you pay it off in time.

That math is genuinely attractive. But the credit score side of it trips people up because there are multiple moving parts happening at once.

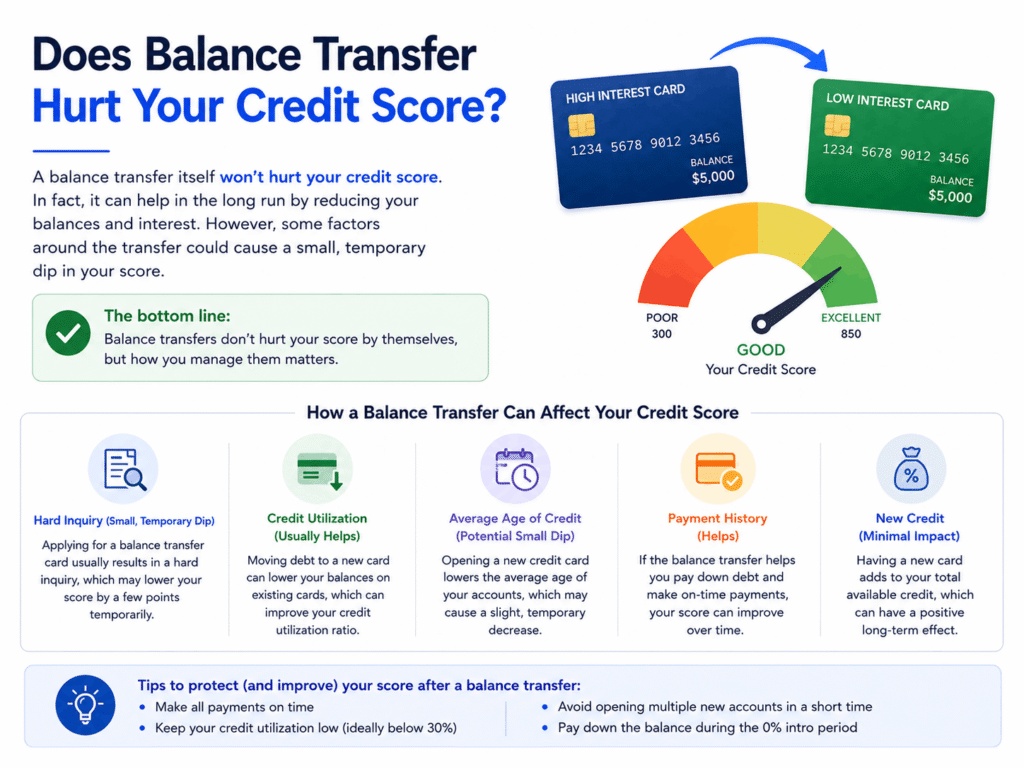

How a Balance Transfer Affects Your Credit Score

1. The Hard Inquiry

When you apply for a new balance transfer card, the issuer pulls your credit report. This is called a hard inquiry, and it typically drops your score by a small amount — usually somewhere between 2 and 5 points, sometimes a bit more.

It’s not nothing, but it’s not catastrophic either. Hard inquiries stay on your credit report for two years, but their impact on your score typically fades significantly after about 12 months.

The problem is when people apply for several cards at once because they got declined once, or they’re shopping around and submitting multiple applications. Multiple hard inquiries in a short window can stack up and look risky to lenders.

2. A New Account Lowers Your Average Age of Credit

Your credit score factors in the average age of all your credit accounts. Open a new card, and that average drops — even if your oldest accounts are years old.

This matters more for people with shorter credit histories. If you’ve only had credit for two or three years, adding a new account has a more noticeable effect than if you’ve had accounts open for a decade.

FICO considers length of credit history to account for about 15% of your overall score. It’s not the biggest factor, but it’s real.

3. Credit Utilization — This Is Where It Gets Interesting

Credit utilization is how much of your available credit you’re using, and it makes up roughly 30% of your FICO score. Lower is better. Under 30% is the general guidance; under 10% is even better.

Here’s how a balance transfer affects this in two ways:

On your old card: If you don’t close it after the transfer, your old card now has a $0 (or near-zero) balance with its full credit limit available. This lowers utilization on that card — which is good.

On your new card: The transferred balance now sits on your new card. Depending on the credit limit you were approved for, your utilization on that card could be quite high — or even maxed out — right from day one.

This is something a lot of people don’t think about. If you transfer $4,000 to a card with a $5,000 limit, you’re at 80% utilization on that new card immediately. That can drag down your score more than the hard inquiry does.

Over time, as you pay down that balance, utilization improves and your score recovers. But in the short term, it can sting.

What Happens to Your Score Over Time

Let’s say you do everything right. You transfer a balance, keep your old card open (and don’t add new charges to it), and consistently pay down the new card before the 0% period ends.

Here’s roughly what the timeline looks like:

Month 1–2: Score dips slightly from the hard inquiry and potentially elevated utilization on the new card.

Month 3–6: Score stabilizes. Payments are building positive payment history.

Month 6–15: As the balance decreases, utilization drops. Score typically starts improving.

Month 12–18: Hard inquiry impact has largely faded. Score may be higher than before the transfer, especially if you’ve significantly reduced total debt.

This is the best-case scenario, and it’s realistic if you stick to the payoff plan.

Real-World Cost Example

Say you have $6,000 in credit card debt at 22% APR.

Without a balance transfer: At minimum payments, you could spend 3+ years paying it off and pay well over $2,000 in interest.

With a balance transfer to a 0% card for 18 months: You pay a 3% transfer fee ($180). To pay off the $6,180 in 18 months, you’d need to pay about $343/month. Total interest paid: $0. Total cost: just the $180 fee.

That’s a real, meaningful difference. The temporary credit score dip — maybe 10–15 points at most — is a reasonable tradeoff for potentially saving over $1,800 in interest.

Hidden Fees and Traps to Know Before You Transfer

Transfer Fees

Most balance transfer cards charge 3%–5% of the transferred amount. Some cards advertise 0% transfer fees, but those usually come with shorter promotional periods or stricter approval requirements.

Do the math before you transfer. If you’re moving $2,000 to save $300 in interest but the fee costs $100, you’re saving $200 net — still worth it, but less impressive than the headline suggests.

The Deferred Interest Trap

This is critical and often misunderstood. Some cards — especially retail and store-branded cards — offer “deferred interest” rather than true 0% APR. With deferred interest, if you carry any remaining balance at the end of the promo period, all the interest that would have accrued gets charged retroactively.

Look for “0% APR” specifically, not “no interest if paid in full.” Those are not the same thing.

What Happens After the Promo Period

If you haven’t paid off the balance before the 0% window closes, the remaining amount gets hit with the card’s regular APR — which can be 25%–29% or higher. This catches a lot of borrowers off guard.

Build a realistic payoff timeline before you transfer. Divide the total balance (including the fee) by the number of months in the promo period. That’s your monthly target. If that number isn’t feasible for your budget, a balance transfer might not solve your problem — it might just delay it.

New Purchases Don’t Always Get the Same Rate

Many balance transfer cards apply the 0% promo rate only to transferred balances, not to new purchases. New purchases might start accruing interest immediately at the regular APR.

Even worse: when you make a payment, issuers may apply it to the lowest-interest balance first, meaning your new purchases sit there accruing interest while you’re paying down the transferred amount.

Common Mistakes That Make Things Worse

Closing the old card after the transfer. This removes available credit from your total, which raises your utilization ratio. Unless there’s a compelling reason (like an annual fee you don’t want to pay), keeping the old card open and unused is usually the smarter move.

Continuing to use the old card. If you rack up new debt on the card you just cleared, you haven’t solved anything. You’ve doubled your problem.

Not getting approved for enough credit. Sometimes people transfer only part of their balance because the new card’s limit isn’t high enough. That’s not always a dealbreaker, but it means you’re juggling two balances, and the high utilization on the new card is still a factor.

Missing a payment. Most 0% APR offers include a clause that terminates the promotional rate immediately if you miss a payment. One late payment can trigger the full APR retroactively in some cases. Set up autopay for at least the minimum as a safety net.

Who Should Think Twice Before Doing This

A balance transfer isn’t the right move for everyone.

If your credit score is below 670, you probably won’t qualify for the best 0% APR offers. You might get approved for something with a shorter promotional period or a higher post-promo APR, which changes the math significantly.

If you can’t realistically pay off the balance within the promo period, you could end up in a similar situation at the end — or worse, if the new card’s APR is higher than your original card’s.

If you have a pattern of carrying balances, a balance transfer addresses the symptom but not the behavior. Without changing spending habits, many people find themselves right back in the same spot 18 months later — sometimes with a new card and the old one partially charged up again.

If you’re planning a major loan application soon — a mortgage, auto loan, or small business loan — a hard inquiry and new account on your file isn’t ideal timing. Even a small dip matters when lenders are reviewing your credit closely.

How to Decide if a Balance Transfer Makes Sense for You

Ask yourself four things:

- Can I get approved for a good offer? Check your credit score beforehand. Most competitive 0% cards require a score of 670 or above. Some require 700+. Prequalification tools exist that use a soft inquiry (no score impact) to give you a general idea.

- Can I pay off the balance in time? Be honest about your monthly budget. If the payoff amount feels aggressive, the transfer might just be kicking debt down the road.

- Will the fee savings actually work out? Run the numbers. Transfer fee versus interest saved. Make sure you’re actually ahead.

- What’s my plan to avoid new debt on the cleared card? This is the one most people skip, and it’s what causes the cycle to repeat.

If you answered those honestly and the math works, a balance transfer is one of the more practical tools available to people managing high-interest credit card debt.

Frequently Asked Questions

Does applying for a balance transfer card always hurt my credit score?

Yes, a small temporary dip is almost certain due to the hard inquiry. The amount is usually modest — under 10 points for most people with established credit.

How long does a balance transfer affect your credit score?

The hard inquiry impact fades significantly within 6–12 months. Any effect from high utilization on the new card improves as you pay down the balance.

Should I close my old card after a balance transfer?

In most cases, no. Keeping it open preserves your available credit and helps your utilization ratio. Close it only if there’s an annual fee you’re not willing to pay, or if you have a spending discipline concern.

Can I do a balance transfer with bad credit?

It’s difficult. Most 0% APR balance transfer offers require good to excellent credit. If your score is lower, you might find limited options with shorter promo periods, higher fees, or higher post-promo APRs.

Is a balance transfer better than a personal loan for debt payoff?

It depends. Balance transfers can have lower total cost if you can pay off the balance during the 0% window. Personal loans give you a fixed payment and fixed rate — more predictable but not interest-free. Compare both for your specific balance and payoff timeline.

What credit score do I need for a balance transfer card?

Generally 670 or above for competitive offers, though some issuers look for 700+. Check the card’s terms and use prequalification tools to avoid unnecessary hard inquiries.

Final Thoughts

A balance transfer will likely cause a small, temporary drop in your credit score. That’s just how credit works — new accounts and hard inquiries always have some short-term impact.

But for most people with solid repayment discipline and a realistic payoff timeline, the credit score effect is minor compared to the interest savings potential. The risk isn’t really the score dip. The real risk is getting the card, feeling relief, not paying it down aggressively enough, and ending up back where you started.

Go in with a plan. Know your monthly payoff target. Keep the old card open. Don’t touch the balance transfer card for new purchases. And understand exactly what happens when that promotional period ends.

Done right, a balance transfer is a legitimate, genuinely useful tool for reducing debt cost. Done carelessly, it just buys you time — at a price.